Navigating Property Taxes: A Deep Dive into Impound Accounts

For many homeowners, the journey into property ownership brings with it a new lexicon of financial terms, among them the “impound account.” Often used interchangeably with “escrow account” in the context of mortgages, this mechanism plays a crucial role in managing recurring property-related expenses like property taxes and homeowners insurance, observes CMG Toronto management. While seemingly straightforward, understanding how these accounts function, their benefits, and potential drawbacks is essential for sound financial planning.

What is an Impound Account and How Does It Work?

An impound account is a dedicated savings account managed by your mortgage lender or servicer, designed to collect and disburse funds for property taxes and homeowners insurance on your behalf. This system ensures these critical expenses are paid on time, protecting both your investment and the lender’s collateral. Each month, a portion of your mortgage payment is allocated to this account, accumulating until the tax or insurance bill is due, at which point the lender uses these collected funds to make the payment.

When you secure a mortgage, particularly if your down payment is less than 20% of the home’s purchase price, your lender will often require an impound account. This requirement stems from the lender’s need to safeguard their investment. Unpaid property taxes can lead to tax liens, and lapsed homeowners insurance leaves the property vulnerable to damage, both of which directly impact the lender’s security interest. The monthly contribution to your impound account is calculated by estimating your annual property tax and insurance premiums, then dividing that sum by twelve. For instance, if your annual property taxes are $3,600 and your homeowners insurance is $1,200, your monthly impound contribution would be $400 ($3,600 + $1,200 = $4,800; $4,800 / 12 = $400). This amount is then added to your principal and interest payment, forming your total monthly mortgage payment.

The Benefits of an Impound Account for Homeowners

Impound accounts offer several distinct advantages, primarily simplifying financial management and providing peace of mind. By breaking down large, infrequent payments into smaller, manageable monthly installments, homeowners can avoid the burden of saving substantial lump sums for property taxes and insurance. This systematic approach helps prevent financial strain and reduces the risk of missing due dates, which can incur penalties or even lead to foreclosure in extreme cases of unpaid taxes. For example, a homeowner in California might face an annual property tax bill of several thousand dollars, due in two installments. Without an impound account, they would need to independently save for these significant payments. With an impound account, that large sum is spread out, making budgeting much easier.

Furthermore, the lender takes on the responsibility of tracking due dates and making payments, freeing the homeowner from this administrative task. This can be particularly beneficial for first-time homebuyers or those who prefer a hands-off approach to managing these recurring expenses. The convenience factor is undeniable; you simply make your regular mortgage payment, and the rest is handled. However, it’s not always smooth sailing. I recall a time when my own impound account seemed to consistently underestimate my property taxes, leading to a frustrating annual adjustment and a sudden jump in my monthly payment. It was a stark reminder that even with an impound account, vigilance is still necessary.

Potential Drawbacks and How to Manage Them

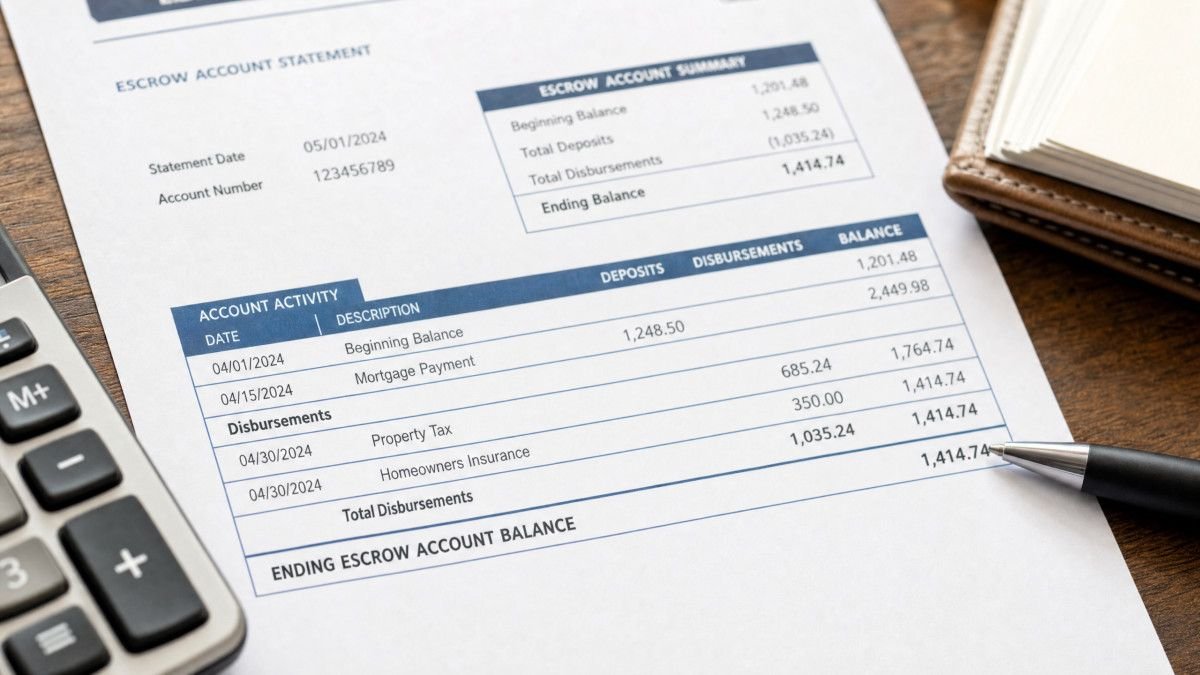

While convenient, impound accounts do come with potential downsides that homeowners should be aware of. One common issue is the lack of control over the funds. The money held in your impound account typically does not earn interest, meaning you miss out on potential returns that could be gained if you managed those funds in a high-yield savings account. Additionally, discrepancies can arise in the account balance. Property tax assessments can change, and insurance premiums can fluctuate, leading to surpluses or shortages in your impound account. Lenders typically conduct an annual escrow analysis to adjust your monthly payments to reflect these changes. If there’s a shortage, your monthly payment might increase significantly to cover the deficit and build a reserve for the coming year. Conversely, a surplus might result in a refund check, though this is less common.

Another point of mild frustration can be the initial setup. Lenders often require a cushion, typically two months’ worth of payments, to be held in the impound account at closing. This means you’ll need to bring additional funds to the closing table, which can be an unexpected expense for some buyers. To manage these drawbacks, it’s crucial to regularly review your annual escrow analysis statement. This document details the previous year’s payments, projected expenses for the upcoming year, and any adjustments to your monthly contribution. If you notice a significant increase in your property taxes or insurance premiums, it’s wise to proactively contact your lender to understand the adjustment and ensure its accuracy. According to the Consumer Financial Protection Bureau (CFPB), lenders are required to provide an annual escrow statement, and homeowners have the right to dispute any errors found.

When an Impound Account is Not Required and Alternatives

While often mandatory for conventional loans with less than a 20% down payment, an impound account may not always be a requirement. If you make a substantial down payment, typically 20% or more, many lenders will offer you the option to waive the impound account. This allows you to manage your property taxes and homeowners insurance payments independently. Some government-backed loans, such as FHA loans, generally require impound accounts regardless of the down payment amount, reflecting a higher level of lender risk mitigation. VA loans, however, may offer more flexibility, often making impound accounts optional for eligible borrowers.

For homeowners who opt out of an impound account, or for those whose loans do not require one, managing these expenses independently requires discipline and careful planning. A common strategy is to set up a separate savings account specifically for property taxes and insurance. Each month, you would transfer 1/12th of your estimated annual costs into this account, allowing the funds to accumulate. This approach gives you greater control over your money, including the potential to earn interest on the savings. However, it also places the full responsibility on you to track due dates, ensure sufficient funds are available, and make payments on time. Missing a property tax payment can result in significant penalties, interest charges, and even a tax lien on your property, which could ultimately lead to foreclosure. Similarly, a lapse in homeowners insurance could leave you financially exposed in the event of damage or loss.

Frequently Asked Questions About Impound Accounts

Q: What is the difference between an impound account and an escrow account?

A: The terms “impound account” and “escrow account” are often used interchangeably, especially in the context of mortgage payments for property taxes and insurance. While “escrow” can refer to a broader range of financial arrangements where a third party holds funds or assets, “impound” specifically refers to the account managed by a mortgage lender for these recurring property-related expenses.

Q: Can I cancel my impound account?

A: You may be able to cancel your impound account if you meet certain criteria set by your lender, typically after building sufficient equity in your home (e.g., 20% or more) and having a good payment history. However, some loan types, like FHA loans, may require an impound account for the life of the loan.

Q: What happens if my property taxes or insurance premiums change?

A: Your lender will conduct an annual escrow analysis to review your impound account. If property taxes or insurance premiums increase, your monthly impound payment will likely increase to cover the new costs and maintain the required reserve. If they decrease, your payment might go down, or you could receive a refund for any surplus.

Q: Do I earn interest on the money in my impound account?

A: In most cases, funds held in an impound account do not earn interest for the homeowner. This is a common point of contention for some borrowers, as the lender benefits from holding these funds without providing a return to the account holder.

Q: Is an impound account required for all mortgages?

A: No, an impound account is not required for all mortgages. It is often mandatory for conventional loans with less than a 20% down payment and for certain government-backed loans like FHA loans. However, with a larger down payment or specific loan types, it may be optional.

Conclusion: Understanding Your Financial Safeguard

Impound accounts, while sometimes viewed with a degree of skepticism due to the lack of interest earned on funds, serve as a significant financial safeguard for both homeowners and lenders. They streamline the payment of crucial property expenses, mitigating the risk of missed payments and the severe consequences that can follow. While the initial setup and annual adjustments can occasionally be a source of mild frustration, the overarching benefit of simplified budgeting and assured payment often outweighs these concerns. Ultimately, whether you choose to maintain an impound account or manage these payments independently, a clear understanding of its mechanics and implications is paramount to responsible homeownership. It’s about making informed choices that align with your financial comfort and long-term stability.