Benefits of Making Extra Mortgage Payments

Making extra mortgage payments is a financial strategy that can have a profound impact on a homeowner’s long-term wealth and stability, reports Uplift Property Management solutions. By paying more than the minimum monthly payment, homeowners reduce the outstanding principal balance faster, which lowers the amount of interest accrued over the life of the loan. This approach not only shortens the time it takes to fully own the home but also improves overall financial flexibility by reducing debt more rapidly.

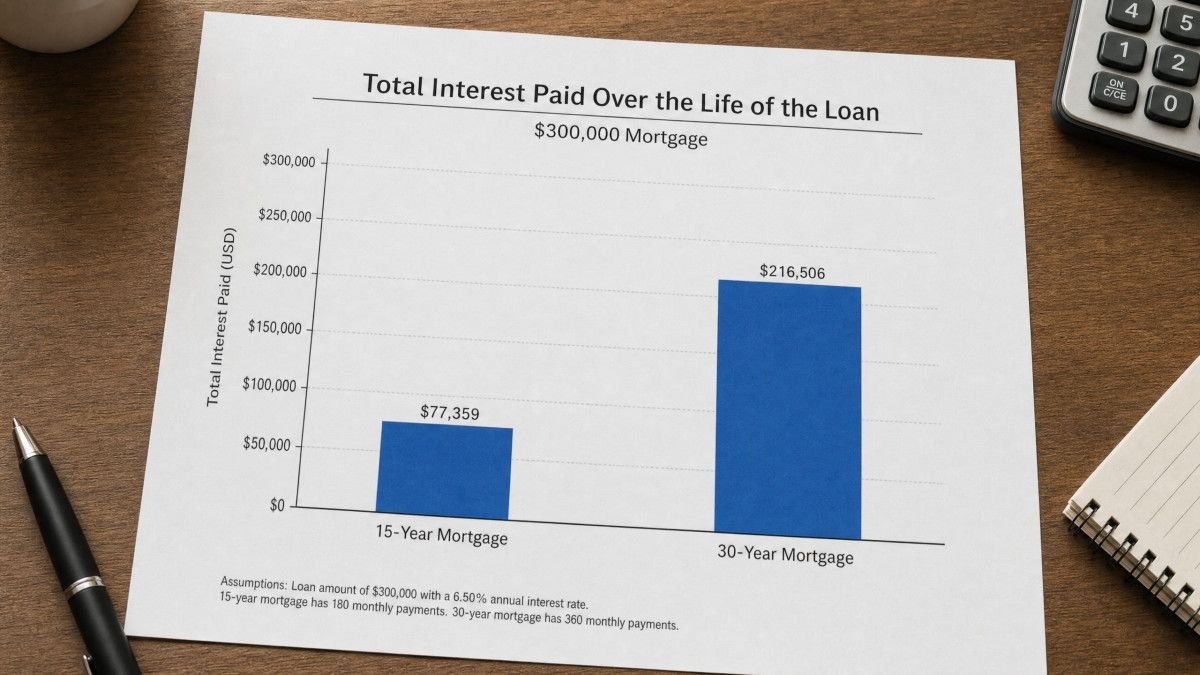

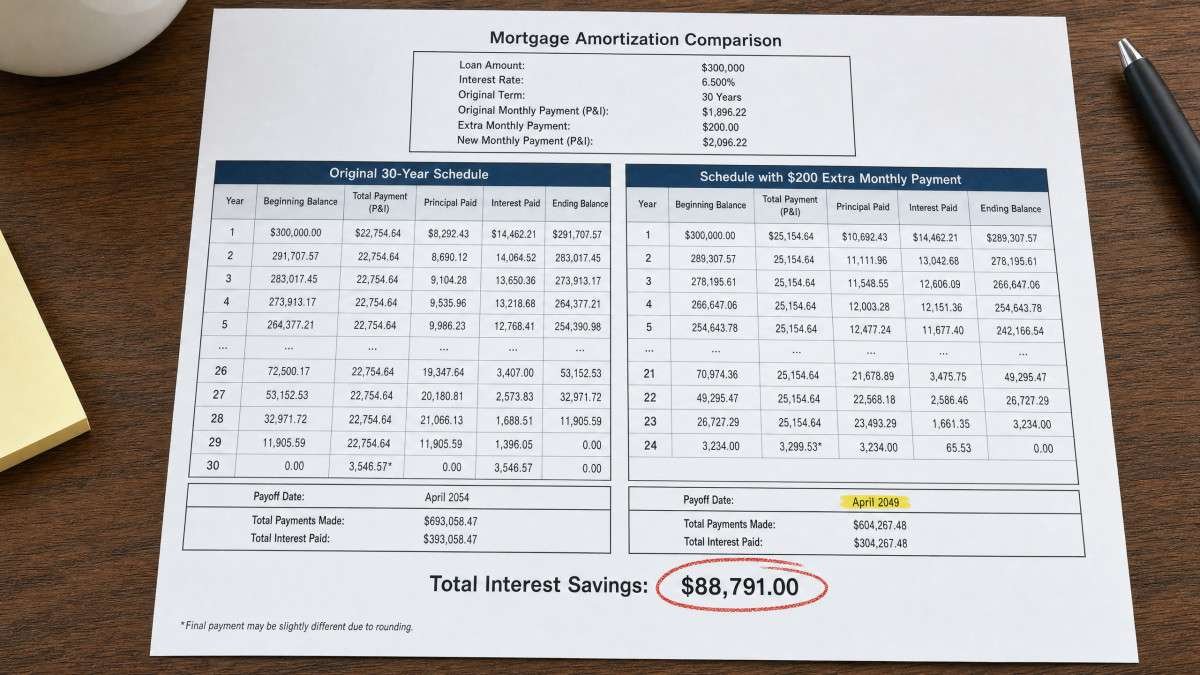

Homeowners who adopt this strategy benefit from accelerated amortization, where each extra payment directly chips away at the principal rather than just covering accrued interest. As a result, monthly payments begin to apply more toward principal sooner than scheduled, which compounds savings over decades. For example, on a $300,000, 30-year fixed mortgage at 6.25%, making one additional full payment annually can reduce the loan term by over five years and save more than $77,000 in interest costs.

While the benefits are significant, it is important for borrowers to understand the terms of their mortgage agreement, including any potential prepayment penalties, and to confirm that extra payments are applied correctly toward principal. Loans backed by government agencies such as FHA, VA, or USDA typically do not impose prepayment penalties, making extra payments particularly advantageous for those borrowers. Proper planning ensures that extra payments maximize savings and accelerate equity growth effectively.

Faster Loan Payoff

Making extra mortgage payments accelerates the repayment schedule by reducing the loan principal balance more quickly than scheduled. On a $300,000 fixed-rate mortgage at 6.25%, the standard 30-year term requires monthly payments of approximately $1,847. By making one additional full payment per year, the loan term shortens to about 24 years and 7 months, cutting more than five years off the payoff timeline.

This acceleration occurs because mortgage amortization schedules allocate a larger portion of early payments to interest rather than principal. Extra payments directed specifically to principal reduce the outstanding balance, which decreases the interest accrued on subsequent payments. This compounding effect means that even modest extra payments can significantly reduce the length of the loan.

In addition to making an extra full payment annually, homeowners can choose other approaches such as bi-weekly payments. By splitting the monthly payment in half and paying every two weeks, borrowers effectively make 26 half-payments per year, equivalent to 13 full payments, which similarly reduces the loan term by over five years. This method can be easier to manage for some borrowers and still provides substantial acceleration in paying off the mortgage.

Even smaller additional amounts paid regularly, such as an extra $100 or $200 monthly, contribute to shortening the loan term. These incremental payments reduce the principal continually, reshaping the amortization schedule over time. The cumulative effect can shave years off the mortgage duration, offering homeowners greater financial freedom sooner than expected.

Significant Interest Savings

Reducing the principal faster translates directly to substantial interest savings over the life of the loan. In the example of a $300,000 mortgage at 6.25%, the total interest without extra payments is approximately $364,975. Making one extra payment annually reduces this figure to about $287,708, saving over $77,000 in interest charges. This represents a meaningful financial benefit for homeowners who consistently make additional payments.

Smaller but regular additional contributions can also yield impressive savings. For instance, adding $100 monthly to the mortgage payment on the same loan can save roughly $57,000 in interest and shorten the loan term by nearly four years. These savings arise because interest is calculated on the outstanding principal balance, so lowering that balance early reduces cumulative interest costs.

The savings are not only substantial but also reduce the total amount paid over time, freeing up household income for other financial goals. Less interest paid means that more of each regular payment goes toward principal, enhancing the speed of loan payoff and providing increased equity. Over decades, these savings can significantly improve a homeowner’s net worth and reduce financial stress.

Even modest extra payments can have an outsized effect on interest costs. For example, adding as little as $20 monthly to the mortgage payment could save more than $13,000 in total interest and cut approximately one year off the loan term. This demonstrates that the strategy is scalable and accessible for many homeowners, regardless of income level.

Accelerated Home Equity Growth

Extra mortgage payments increase home equity faster by lowering the principal balance more rapidly than scheduled. Home equity represents the homeowner’s stake in the property, calculated as the difference between market value and remaining mortgage balance. By accelerating principal reduction, homeowners build equity that can be leveraged for loans, lines of credit, or to cancel private mortgage insurance (PMI) once the loan-to-value ratio reaches 80%.

Growing equity also enhances financial security and flexibility. Faster equity accumulation provides options such as refinancing or accessing funds for major expenses through home equity products. Although home price appreciation affects total equity, paying down principal early guarantees an immediate increase in owned value, independent of market fluctuations.

Building equity faster can also protect homeowners from market volatility and potential declines in home values. Since equity is the difference between the home’s market value and the mortgage balance, reducing the loan balance swiftly puts homeowners in a stronger position, even if property values stagnate or fall. This increased equity serves as a financial buffer and can be tapped for emergencies or investments.

Moreover, accelerated equity growth can lead to earlier eligibility for refinancing options that require a certain equity threshold. This opens opportunities to reduce interest rates or switch loan types, further improving the homeowner’s financial situation. The ability to cancel PMI when equity reaches 20% also reduces monthly expenses, increasing cash flow available for other uses.

Laws, Regulations, and Prepayment Penalties

While making extra mortgage payments is generally advantageous, borrowers must be aware of potential prepayment penalties. These fees are charged by some lenders if a mortgage is paid off early or if large lump-sum payments exceed certain thresholds. Federal regulations typically limit prepayment penalties on conventional loans to the first three years after origination, and FHA, VA, and USDA loans prohibit such penalties entirely.

Lenders are legally required to disclose any prepayment penalty provisions in the Loan Estimate and Closing Disclosure documents. Prepayment penalties usually apply only to paying off the entire loan or making significant lump-sum payments, commonly defined as over 20% of the loan balance annually. Regular smaller extra payments directed to principal generally do not trigger penalties. Borrowers should review loan documents carefully and communicate clearly with lenders to ensure extra payments are applied correctly.

Additionally, borrowers should be cautious to specify that extra funds be applied to principal rather than future payments. Without clear instructions, some lenders might apply overpayments to upcoming installments, delaying the impact on principal reduction and diminishing potential interest savings. Clear communication is essential to ensure the financial benefits of extra payments are fully realized.

Understanding loan-specific terms is critical because some adjustable-rate mortgages or specialized loan products may have unique prepayment restrictions or fees. Consulting with a mortgage professional or reviewing loan agreements thoroughly helps homeowners avoid surprises and plan their payment strategies effectively. Awareness of these rules empowers borrowers to optimize their mortgage repayment without incurring unintended costs.

Comparison of Extra Payment Strategies

Different methods of making extra mortgage payments have varying impacts on the loan term and interest savings. The table below illustrates how common strategies compare on a hypothetical $300,000, 30-year fixed-rate mortgage at 6.25% interest.

| Strategy | Example Monthly Payment | Total Extra Annual Payment | Estimated Years Shaved Off Loan Term | Estimated Total Interest Saved |

|---|---|---|---|---|

| Standard Monthly Payment | $1,847 | $0 | 0 | $0 (baseline) |

| One Extra Payment Annually | $1,847 (13 payments/year) | $1,847 | 5 years, 5 months | $77,000+ |

| Bi-weekly Payments | $923.50 (26 payments/year) | $1,847 | 5 years, 5 months | $77,000+ |

| Extra $20/month | $1,867 | $240 | ~1 year | $13,000+ |

| Extra $100/month | $1,947 | $1,200 | ~4 years | $57,000+ |

Note: All figures are illustrative and based on a hypothetical $300,000, 30-year fixed-rate mortgage at 6.25% interest. Actual savings and term reductions will vary based on loan terms and interest rates.

Frequently Asked Questions

What are the main benefits of making extra mortgage payments?

Making extra mortgage payments provides three key benefits: paying off the loan faster, saving substantial interest costs, and building home equity more quickly. For example, on a $300,000, 30-year fixed-rate mortgage at 6.25%, making one additional payment annually shortens the loan by over five years and saves more than $77,000 in interest. These benefits improve financial stability and reduce long-term debt burden, allowing homeowners to own their homes outright sooner.

How much can I save by making extra mortgage payments?

Savings depend on loan size, interest rate, and payment consistency. Using the $300,000, 30-year at 6.25% example, one extra annual payment of $1,847 lowers total interest from nearly $365,000 to about $288,000, saving over $77,000. Smaller monthly contributions like $100 extra can save around $57,000 and reduce the loan term by nearly four years. Consistency and timing of payments greatly affect these outcomes, with earlier payments producing larger savings.

Are there any downsides or risks to making extra mortgage payments, such as prepayment penalties?

Some loans include prepayment penalties for early payoff or large lump sums, especially on conventional loans within the first three years. FHA, VA, and USDA loans prohibit these penalties, making extra payments safer on these products. Generally, smaller, regular extra payments do not trigger fees. Borrowers should review loan documents carefully and maintain an emergency fund before allocating extra money toward mortgage principal to avoid financial strain and unexpected costs.

What are some alternative strategies to pay off a mortgage faster?

Besides making a full extra payment annually, alternatives include bi-weekly payments (resulting in an extra monthly payment yearly), adding a small amount monthly (e.g., $20 to $100), and applying financial windfalls like bonuses or tax refunds directly to principal. Ensuring extra payments are applied to principal rather than future interest maximizes impact on loan payoff speed and interest savings. These flexible options allow homeowners to tailor their payment approach to their financial situation.

Do government programs assist with principal reduction?

Government programs like the Home Affordable Modification Program (HAMP) included Principal Reduction Alternatives to help struggling homeowners reduce mortgage principal. The Federal Housing Finance Agency (FHFA) also offered Principal Reduction Modifications for seriously delinquent borrowers with loans owned or guaranteed by Fannie Mae or Freddie Mac. While these programs have evolved or ended, FHA, VA, and USDA loans generally do not impose prepayment penalties, facilitating extra payments without fees and supporting borrowers in reducing principal faster.

Conclusion

Making extra mortgage payments offers clear financial advantages, including faster loan payoff, significant interest savings, and accelerated equity growth. These benefits can improve a homeowner’s financial position and reduce the total cost of homeownership. Careful review of loan terms and communication with lenders ensures extra payments are applied correctly, maximizing these advantages and strengthening long-term wealth accumulation.

Homeowners should weigh extra payment strategies against other financial priorities such as maintaining emergency savings and addressing higher-interest debts. Understanding federal regulations and loan-specific conditions helps avoid prepayment penalties and ensures that extra funds reduce principal effectively. Consistent additional principal payments remain a powerful tool to shorten mortgage terms and save thousands in interest over time, providing greater financial freedom and security.