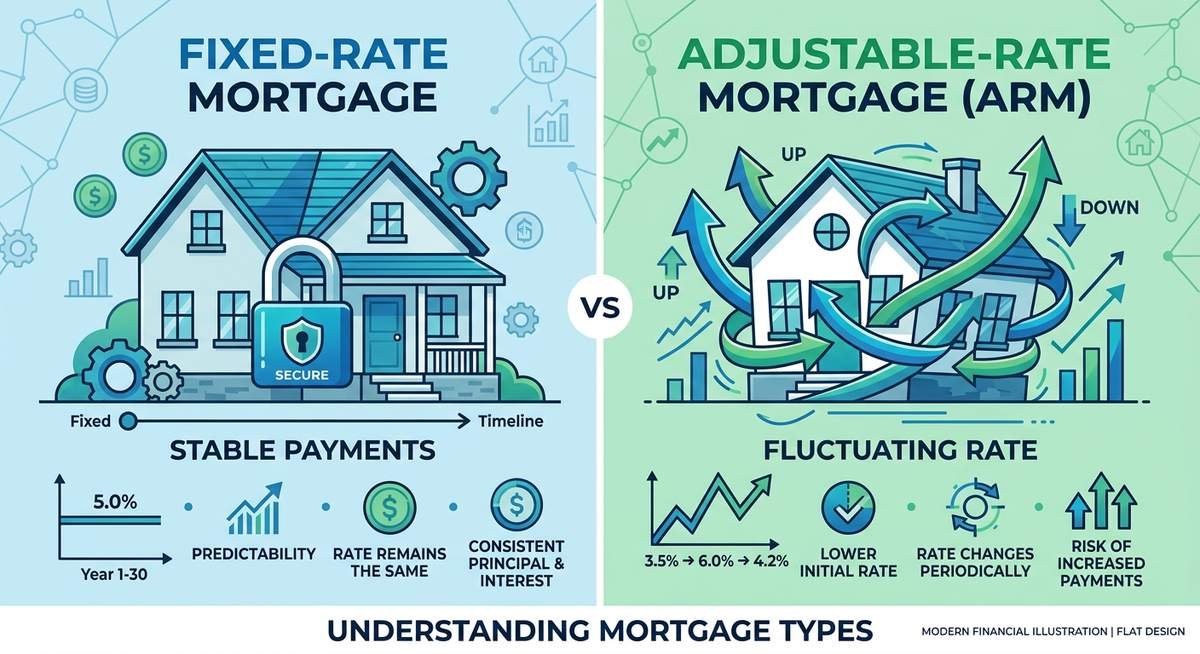

The fixed rate vs adjustable mortgage decision is one of the most consequential choices a homebuyer makes, yet most borrowers spend less than an hour comparing the two. A fixed-rate mortgage locks your interest rate for the entire loan term, keeping monthly payments identical from the first payment to the last. An adjustable-rate mortgage (ARM) starts with a lower introductory rate that can rise or fall after an initial fixed period, typically three to ten years. For most long-term homeowners, the fixed rate offers certainty worth paying for. For buyers who plan to sell or refinance within seven years, an ARM can cut thousands in interest costs during that window.

How a Fixed-Rate Mortgage Works

A fixed-rate mortgage carries the same interest rate from origination to payoff, regardless of what happens to market rates. If you close at 6.75%, that number stays put whether the Fed raises rates ten more times or cuts them to near zero.

The most common terms are 15 years and 30 years, though lenders also offer 10- and 20-year options. On a 30-year fixed loan, your principal-and-interest payment never changes, which makes budgeting straightforward for decades at a time.

According to Freddie Mac’s Primary Mortgage Market Survey, the 30-year fixed rate averaged around 6.8% through early 2026, down from the 7.8% peak seen in late 2023. The 15-year fixed ran about 75 to 100 basis points lower.

The predictability has a real dollar cost. Because lenders assume all the rate risk on a fixed product, they charge a premium above where short-term rates sit. That spread is the price of certainty.

How an Adjustable-Rate Mortgage Works

An ARM starts with a fixed introductory rate, then adjusts periodically based on a benchmark index, most commonly the Secured Overnight Financing Rate (SOFR). The naming convention tells you the structure: a 5/1 ARM holds its initial rate for five years, then resets annually. A 7/6 ARM fixes for seven years, then adjusts every six months.

Lenders set the margin, typically 2.25% to 3%, which gets added to the index at each adjustment. If SOFR is sitting at 4.5% and your margin is 2.5%, your new rate is 7%. That arithmetic runs every adjustment period for the remaining life of the loan.

The appeal is simple: introductory ARM rates typically run 0.5% to 1.5% lower than comparable fixed rates. On a $400,000 loan, a 1% rate difference translates to roughly $235 per month in savings during the initial period.

Fixed-Rate vs. Adjustable-Rate Mortgage: Head-to-Head Comparison

The fixed rate vs adjustable mortgage comparison comes down to one core trade-off: stability versus initial cost savings. Fixed-rate mortgages eliminate payment uncertainty entirely; ARMs offer lower entry costs in exchange for future rate risk.

| Feature | Fixed-Rate Mortgage | Adjustable-Rate Mortgage (ARM) |

|---|---|---|

| Interest rate | Locked for entire loan term | Fixed initially, then adjusts periodically |

| Monthly payment | Never changes (P&I) | Can rise or fall after initial period |

| Common terms | 10, 15, 20, 30 years | 3/1, 5/1, 7/1, 7/6, 10/1 ARMs |

| Typical starting rate (2026) | 6.5%–7.2% (30-yr) | 5.9%–6.6% (7/1 ARM) |

| Rate risk | None — lender bears it | Borrower bears it after initial period |

| Best for | Long-term owners, fixed-income budgets | Short-term owners, falling rate environments |

| Refinancing need | Optional | Often strategically timed before reset |

| Rate protection | Complete | Partial (rate caps apply) |

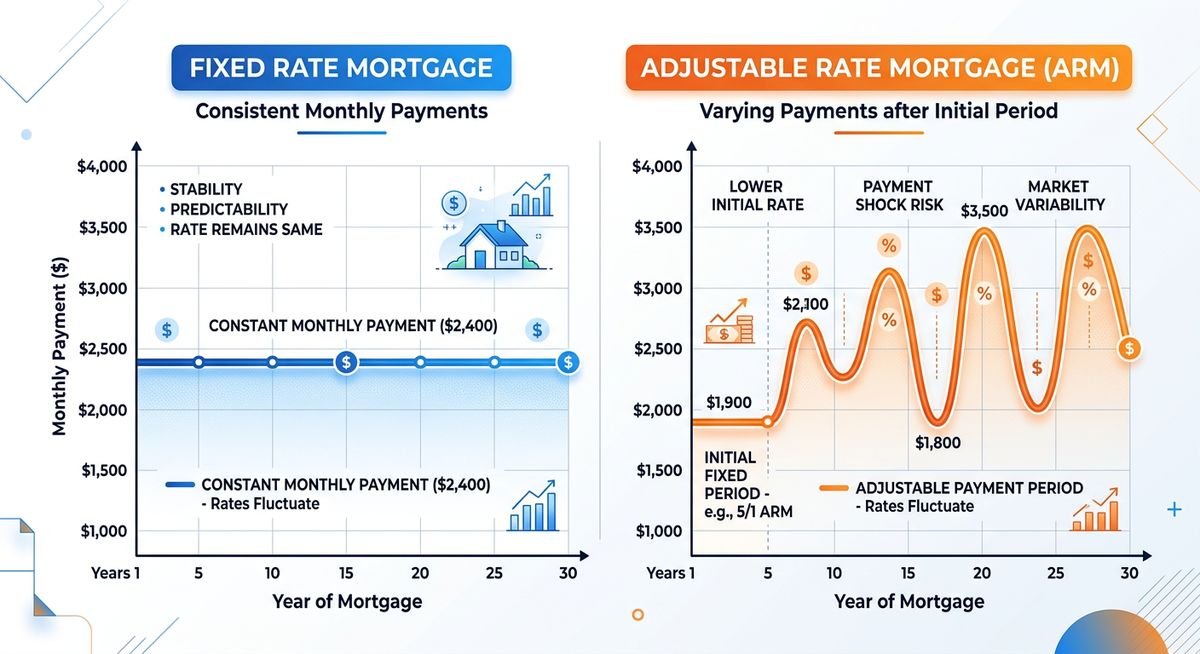

Payment example on a $400,000 loan at current rates: a 30-year fixed at 6.9% produces a monthly principal and interest payment of approximately $2,646. A 7/1 ARM at 6.3% produces approximately $2,481 per month for the first seven years, saving $165 monthly and $13,860 over the initial fixed window.

ARM Rate Caps: The Math Behind Your Worst-Case Payment

Rate caps are the contractual limits on how much an ARM rate can move, and understanding them is non-negotiable before signing. Every ARM has three cap numbers, typically expressed as a sequence like 2/2/5.

- Initial cap: Maximum rate change at the first adjustment. A 2% initial cap means if you started at 6.3%, your first reset cannot push the rate above 8.3%.

- Periodic cap: Maximum change at any subsequent adjustment. A 2% periodic cap prevents the rate from jumping more than 2 percentage points in any single adjustment period.

- Lifetime cap: Maximum increase over the original start rate for the life of the loan. A 5% lifetime cap means a 6.3% ARM can never exceed 11.3%.

Most conventional ARMs today carry a 2/2/5 cap structure. Working through the worst case on that $400,000 loan: if the 7/1 ARM at 6.3% hits its lifetime cap of 11.3% after seven years, the monthly payment would climb from $2,481 to approximately $4,013. That is a $1,532 monthly increase on a single rate adjustment scenario playing out to maximum. The Consumer Financial Protection Bureau (CFPB) requires lenders to show borrowers the worst-case payment scenario in writing before closing, which gives you concrete numbers to stress-test against your income.

Most borrowers do not hit lifetime caps. But the fact that the number exists at all is the honest reason many people choose the fixed option.

When to Choose a Fixed-Rate Mortgage

The fixed rate makes the most financial sense when you plan to stay in the home long enough to absorb the rate premium through stability, typically beyond seven to ten years.

Specific situations that point strongly toward fixed:

- You are buying a long-term family home and do not plan to move within the ARM’s introductory window.

- Your income is relatively fixed, including salaried employees, retirees on fixed income, or single-income households where payment predictability is critical.

- Current ARM rates are close to fixed rates, narrowing the break-even period to the point where the risk is not worth the modest savings.

- You believe interest rates will trend higher over the next decade, meaning ARMs are likely to reset upward.

- You have experienced difficulty qualifying and want no risk of payment increases affecting your ability to stay current.

There is something worth acknowledging about the psychology here: millions of homeowners who locked 30-year rates between 2020 and 2022 at 2.75% to 3.5% have stayed in homes they might otherwise have sold, because their payment is irreplaceable at current market rates. The fixed rate is not just a financial instrument. It is occasionally a life anchor.

When an ARM Makes Financial Sense

ARMs are genuinely the better financial product in a narrow but real set of circumstances. The math works in your favor when your ownership timeline is shorter than the ARM’s introductory window.

A 7/1 ARM is a straightforward win if you are buying a home you intend to sell or refinance within five to six years. You capture seven years of below-market rates and exit before the first adjustment. The savings can easily reach $15,000 to $25,000 on a standard loan amount.

Other scenarios where ARMs perform well:

- Medical residents or early-career professionals who expect significant income growth and may refinance into a fixed rate once equity builds.

- Buyers in a high-rate environment who expect rates to fall materially within the ARM’s introductory period, positioning them to refinance into a better fixed rate before the ARM adjusts.

- Buyers purchasing a starter home who plan to move up within seven years as family or career circumstances change.

- Investors who plan to sell a property within a defined time horizon.

According to data from the Mortgage Bankers Association, ARM applications historically spike when the spread between fixed and adjustable rates widens beyond 150 basis points. At that differential, the break-even calculation decisively favors the ARM for ownership periods under seven years.

Fixed vs. ARM in 2026: What the Current Rate Environment Changes

The fixed vs. ARM decision does not exist in a vacuum. The interest rate environment shapes which product makes more tactical sense at any given time.

As of early 2026, the 30-year fixed rate sits in the 6.7%–7.2% range according to Freddie Mac’s weekly Primary Mortgage Market Survey (PMMS), while many 7/1 ARMs are being offered in the 6.0%–6.5% range. That spread of roughly 50 to 75 basis points is narrower than the historical average of 100 to 150 basis points, which compresses the ARM’s advantage. The break-even period for choosing an ARM over a fixed rate at that spread extends to roughly nine to twelve years of ownership for the math to pay out, which is longer than many ARM borrowers expect to stay.

The Federal Reserve began easing rates in late 2024, and market expectations through 2025 anticipated continued cuts. That trajectory, if sustained, benefits ARM holders because the index rate underlying most ARM adjustments would fall, pulling adjusted payments lower or keeping them near the introductory rate. Borrowers who took ARMs in 2023 at their peak rates have already seen their first adjustments come in below their introductory rate in some cases, a counterintuitive outcome that reflects how rate cycles work in practice.

The honest answer in 2026 is that neither product is obviously superior at current spreads. The fixed rate is not dramatically overpriced, and the ARM’s discount is not compelling enough to override the stability argument for most long-term owners. The decision comes back to ownership timeline and risk tolerance, as it always has.

“We’re in year 3 of our 7/1 ARM and the rate just adjusted for the first time. It went down by 0.3% because SOFR dropped. We’re paying less than our initial rate now. People act like ARMs always go up, but they move with market rates — that cuts both ways.”

— r/Mortgages, October 2024 (9 upvotes)

This aligns with how ARM mechanics actually work: the adjustment formula is purely mathematical, tied to an index that moves in both directions. The Wikipedia overview of adjustable-rate mortgages provides a useful reference on how index benchmarks influence ARM resets across different rate environments.

Frequently Asked Questions

Which is better: fixed rate vs adjustable mortgage?

Neither is universally better in the fixed rate vs adjustable mortgage comparison. A fixed-rate mortgage is better for homeowners planning to stay long-term who want payment certainty. An ARM is better for buyers who will sell or refinance before the introductory period ends, because the lower starting rate reduces total interest paid over a short ownership window.

What happens when an ARM adjusts?

When an ARM’s introductory period ends, the lender calculates a new rate by adding the margin (typically 2.25%–3%) to the current benchmark index, usually SOFR. The result is your new interest rate, subject to the periodic and lifetime caps outlined in your loan documents. The adjusted rate applies to the remaining loan balance, and your monthly payment is recalculated accordingly.

Can an ARM rate go down after adjustment?

Yes. If the benchmark index falls between adjustment dates, your ARM rate can decrease, resulting in a lower monthly payment. This happened for many ARM borrowers in 2024 and 2025 as the Federal Reserve cut rates, with some seeing their rate adjust downward at the first reset. ARM rates move in both directions with market conditions.

How long do you need to stay home for an ARM to save money?

For a 7/1 ARM with a 0.75% rate advantage over a fixed loan, you need to sell or refinance before approximately year eight for the ARM to deliver net savings, accounting for the risk that the adjusted rate will exceed the fixed rate after the introductory window. At narrower spreads of 0.5% or less, the ARM’s advantage disappears before year six.

What does a 2/2/5 cap structure mean on an ARM?

A 2/2/5 cap structure means the rate can increase no more than 2% at the first adjustment, no more than 2% at any subsequent adjustment, and no more than 5% above the original start rate over the life of the loan. On a 6.3% ARM with a 2/2/5 cap, the rate can never exceed 11.3%, regardless of how high market rates climb.

Should I refinance my ARM before it resets?

Refinancing before your ARM’s first adjustment is a sound strategy if current fixed rates are acceptable relative to your existing rate, you plan to stay in the home long-term, and refinancing costs can be recouped within two to four years. If fixed rates are significantly higher than your ARM’s current rate, you may be better served waiting to see where the adjustment lands given prevailing market conditions.

As a first-time buyer, should I choose a fixed or ARM?

Most financial advisors recommend fixed-rate mortgages for first-time buyers because the payment predictability supports budgeting stability during a period when other homeownership costs (maintenance, property taxes, insurance) are also new and uncertain. An ARM can still make sense for first-time buyers who are confident they will move or refinance within the introductory period and have enough income cushion to absorb a worst-case payment increase if plans change.

The Bottom Line

The fixed-rate vs. adjustable-rate mortgage decision is ultimately a bet on how long you will stay and where rates will go, two things no one can know with certainty.

For homeowners planning to stay more than ten years, the fixed rate offers something that cannot be quantified entirely in monthly payment savings: the ability to set your housing cost and walk away from rate anxiety entirely. For buyers with a clear short-term timeline and meaningful income flexibility, an ARM can cut real costs over the ownership window.

Run the numbers on both options with current rate quotes, model the ARM’s worst-case payment against your income, and align the choice with how long you honestly expect to own the home. The math will usually point you in the right direction.