For many aspiring homeowners, the dream of buying a house often collides with the reality of student loan debt. This financial obligation, while an investment in education, can significantly influence your ability to qualify for a mortgage, points out BridgeHaus Property Managers Oceanside. Understanding how lenders view student loans and what steps you can take to mitigate their impact is crucial for navigating the home-buying process successfully.

Understanding Your Debt-to-Income Ratio (DTI) with Student Loans

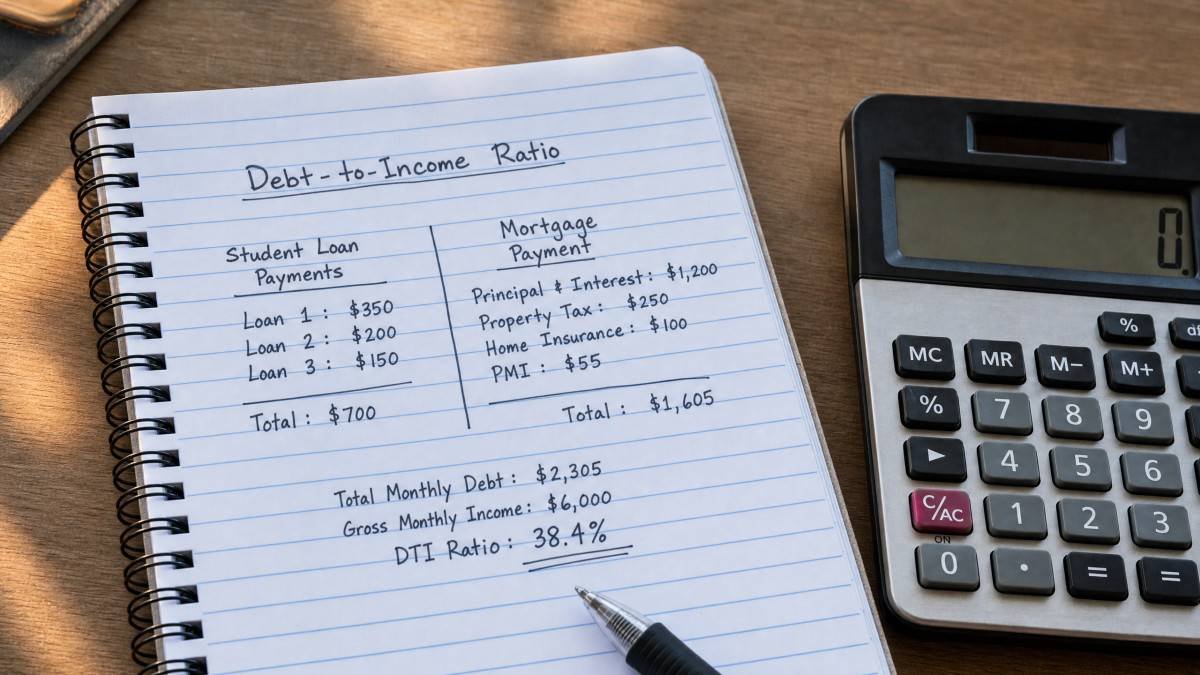

Your debt-to-income (DTI) ratio is a critical factor lenders use to assess your ability to manage monthly payments and repay debts, including a new mortgage. Generally, a lower DTI indicates less risk, making you a more attractive borrower. Student loan payments directly contribute to this ratio, potentially pushing it higher and impacting your eligibility. Lenders typically prefer a DTI of 43% or less, though this can vary significantly by loan type and individual circumstances, with some programs allowing up to 50% for highly qualified borrowers. This ratio is essentially a snapshot of your financial health, telling lenders how much of your gross monthly income is consumed by debt payments.

How Lenders Calculate DTI with Student Loan Payments

Lenders calculate your DTI by dividing your total monthly debt payments by your gross monthly income. When it comes to student loans, the calculation isn’t always uniform, which can be a source of considerable frustration for applicants. For federal student loans, if your payment is deferred or on an income-driven repayment (IDR) plan with a $0 payment, some lenders might still use a hypothetical payment. This hypothetical payment is often calculated as 0.5% or 1% of the outstanding loan balance, regardless of your actual current payment. For example, a $50,000 student loan balance could translate to a $250 to $500 monthly payment in the lender’s DTI calculation, even if you’re currently paying nothing. This approach is designed to account for potential future payment obligations once deferment or IDR terms expire. For private student loans, lenders almost always use the actual monthly payment reported on your credit report, as these loans typically have less flexible repayment options.

The Impact of Income-Driven Repayment (IDR) Plans on DTI

Income-driven repayment (IDR) plans, such as PAYE, REPAYE, IBR, and ICR, are designed to make federal student loan payments more affordable by capping them at a percentage of your discretionary income. While these plans can lower your monthly student loan payments, sometimes even to $0, which might seem beneficial for your DTI, their impact on mortgage qualification is complex. As mentioned, some mortgage lenders, particularly for conventional loans backed by Fannie Mae, may not use the $0 or reduced IDR payment. Instead, they might calculate a “qualifying payment” based on a percentage of your loan balance, typically 1%. This can significantly increase your perceived monthly debt obligation and, consequently, your DTI, making it harder to meet eligibility thresholds. This is one of those areas where the answer depends on factors your lender won’t always explain upfront, requiring you to ask very specific questions about their DTI calculation methodology for IDR plans. For instance, if you have a $100,000 student loan balance on an IDR plan with a $50 monthly payment, a lender using the 1% rule would factor in a $1,000 monthly payment for DTI purposes, a substantial difference.

Credit Score and Student Loan Debt: What Lenders Look For

Your credit score is another cornerstone of mortgage eligibility, reflecting your creditworthiness and payment history. Student loan debt, when managed responsibly with consistent, on-time payments, can actually help build a positive credit history, demonstrating your ability to handle long-term financial commitments. However, missed or late payments can severely damage your score, making it harder to qualify for a mortgage or secure favorable interest rates. Lenders look for a history of timely payments, a reasonable amount of credit utilization across all your accounts, and a diverse credit mix. A strong credit score signals to lenders that you are a reliable borrower, capable of fulfilling your financial obligations.

Building and Maintaining a Strong Credit Score

To build and maintain a strong credit score while managing student loan debt, consistency is key. Always make your student loan payments on time, as payment history accounts for a significant portion (around 35%) of your FICO score. Keep your credit utilization low on other credit lines, such as credit cards, ideally below 30% of your available credit limit. For example, if you have a credit card with a $10,000 limit, try to keep your balance below $3,000. Avoid opening too many new credit accounts close to applying for a mortgage, as each new inquiry can temporarily lower your score by a few points. A FICO score above 620 is generally considered the minimum for conventional loans, but higher scores (e.g., 740+) unlock the best rates and terms, potentially saving you tens of thousands of dollars over the life of the loan. Regularly checking your credit report for errors and disputing any inaccuracies can also help ensure your score accurately reflects your financial behavior.

Exploring Mortgage Programs for Borrowers with Student Loan Debt

Several mortgage programs exist, each with different guidelines regarding student loan debt. Understanding these differences can help you choose the best path forward. Some programs are more forgiving of student loan debt or offer more flexible DTI calculations, while others have stricter requirements. It’s important to research each option thoroughly to see which aligns best with your financial situation, as the right program can make a significant difference in your ability to secure a home loan. The nuances between these programs can be substantial, and what works for one borrower might not work for another.

Conventional Loans and Student Debt

Conventional loans, backed by government-sponsored enterprises like Fannie Mae and Freddie Mac, typically have stricter DTI requirements and specific rules for student loan debt. For deferred student loans or those in forbearance, Fannie Mae generally requires lenders to use either 1% of the outstanding loan balance as a monthly payment or the actual documented payment if it’s greater than $0. For example, a $75,000 student loan in deferment would be assessed a $750 monthly payment for DTI purposes. Freddie Mac, on the other hand, allows lenders to use the actual payment reported on the credit report, even if it’s $0, for income-driven repayment plans, provided certain conditions are met, such as the payment being fixed or scheduled to increase gradually. This distinction between Fannie Mae and Freddie Mac guidelines can be significant for borrowers with IDR plans, making it crucial to understand which type of conventional loan your lender is offering.

FHA, VA, and USDA Loans: Special Considerations

Government-backed loans often offer more flexibility for borrowers with student loan debt. FHA loans, insured by the Federal Housing Administration, for instance, generally require lenders to use 0.5% of the outstanding student loan balance as a monthly payment if the actual payment is deferred or on an IDR plan that results in a $0 payment. This can be more favorable than conventional loan calculations for some borrowers. VA loans, available to eligible service members, veterans, and surviving spouses, are often the most lenient, allowing lenders to exclude deferred student loan payments that won’t begin for at least 12 months after the mortgage closing. This policy recognizes the unique financial situations of military personnel. USDA loans, designed for rural properties, also have specific guidelines, often using 0.5% of the outstanding balance for deferred loans. According to the Department of Education (2023), over 43 million Americans hold federal student loan debt, totaling over $1.6 trillion, highlighting the widespread impact of these policies and the need for flexible mortgage options.

Strategies to Improve Your Mortgage Eligibility

Even with student loan debt, there are proactive steps you can take to enhance your mortgage eligibility. These strategies often involve improving your financial profile and understanding how to best present your situation to lenders. A combination of approaches usually yields the best results, and starting early can make a substantial difference in your home-buying journey. It’s about being strategic and disciplined with your finances.

Reducing Your Student Loan Burden

One direct way to improve your DTI is to reduce your student loan burden. This could involve making extra payments to pay down a portion of your principal balance before applying for a mortgage, which directly lowers your monthly payment and thus your DTI. For example, paying an extra $5,000 on a $50,000 loan could reduce your monthly payment by $50-$100, significantly impacting your DTI. Consolidating or refinancing your student loans into a lower interest rate or a shorter repayment term can also reduce your monthly outflow, though be cautious about extending the repayment period too much if it significantly increases the total interest paid over the life of the loan. Always evaluate the long-term financial implications and ensure that any refinancing doesn’t negatively impact your credit score right before a mortgage application. Some borrowers even consider aggressive repayment strategies like the debt snowball or debt avalanche methods to eliminate student loan debt faster.

Boosting Your Overall Financial Profile

Beyond student loans, strengthening your overall financial profile can significantly boost your mortgage eligibility. This includes increasing your savings for a larger down payment, which reduces the loan amount needed and can lower your monthly mortgage payment. A larger down payment also signals financial stability to lenders. Improving your credit score by paying all bills on time and reducing other debts, like credit card balances, is also crucial. Aim to pay off credit card balances entirely each month if possible. Demonstrating a stable employment history, ideally with at least two years in the same field, and consistent income further reassures lenders of your financial reliability. Sometimes, even a small increase in income or a slight reduction in other monthly debts can make a difference in your DTI, pushing you over the eligibility threshold. Consider taking on a side hustle or temporarily cutting discretionary spending to accelerate debt reduction or savings.

FAQ

Q1: How do student loans affect my debt-to-income ratio for a mortgage?

A1: Student loans directly impact your debt-to-income (DTI) ratio by adding to your total monthly debt obligations, which lenders use to assess your ability to afford a mortgage. Lenders typically prefer a DTI of 43% or less, and your student loan payment is a key component of this calculation, sometimes even if your current payment is $0.

Q2: Can I get a mortgage with student loan debt if my payments are deferred or on an income-driven plan?

A2: Yes, it is possible, but lenders may calculate a hypothetical monthly payment (e.g., 0.5% or 1% of the loan balance) for deferred or income-driven repayment plans, even if your actual payment is $0, which can significantly affect your DTI. This varies by loan type (Conventional, FHA, VA) and individual lender policies.

Q3: What credit score do I need for a mortgage if I have student loan debt?

A3: While student loan debt itself doesn’t dictate a specific credit score, maintaining good payment history on your student loans is vital for a strong score. A FICO score above 620 is generally a minimum for conventional loans, but higher scores (e.g., 740+) improve your chances and secure better interest rates and terms.

Q4: Are there specific mortgage programs for people with student loan debt?

A4: While not exclusively for student loan debt, government-backed programs like FHA, VA, and USDA loans often offer more flexible DTI calculations or considerations for student loans compared to conventional loans. Each program has specific guidelines regarding how student loan payments are factored into eligibility.

Q5: What steps can I take to improve my chances of getting a mortgage with student loan debt?

A5: To improve your chances, focus on reducing your overall debt-to-income ratio by paying down student loan principal, increasing your credit score through timely payments and low credit utilization, saving for a larger down payment, and exploring government-backed loan programs that may be more flexible with student loan debt.

Conclusion

Navigating the path to homeownership with student loan debt requires careful planning and a thorough understanding of mortgage eligibility criteria. While student loans can present challenges, they are by no means an insurmountable barrier. By proactively managing your debt-to-income ratio, maintaining a strong credit score, and exploring the various mortgage programs available, you can significantly improve your chances of securing a home loan. The journey might involve some strategic financial adjustments and diligent research into lender-specific policies, but with the right approach and a clear understanding of the financial landscape, owning a home remains an achievable goal for many. Don’t let student loan debt deter you from your homeownership dreams; instead, empower yourself with knowledge and a solid financial strategy.