As noted by Azure Sky Management, mortgage scams are a serious threat that cost American homeowners hundreds of millions annually. These scams exploit individuals during the home buying or foreclosure process, often resulting in devastating financial losses and sometimes the loss of the home itself. Being aware of common fraud tactics and taking proactive steps can significantly reduce the risk of falling victim to these schemes.

Scammers use sophisticated methods such as email phishing, false loan modification offers, and deceptive refinancing schemes to trick borrowers. The FBI reported a staggering 1,100 percent increase in mortgage closing phishing attempts between 2015 and 2017, with losses approaching $1 billion in real estate transaction costs in 2017 alone. Understanding these risks is essential for all homeowners and prospective buyers.

Federal agencies including the Consumer Financial Protection Bureau (CFPB), HUD, and the FDIC provide extensive resources to help consumers identify and avoid mortgage fraud. Recognizing red flags, verifying communications, and knowing where to report suspicious activity are critical components of protecting your home and finances from these costly scams.

The scope of mortgage fraud extends beyond individual victims and affects the overall housing market and financial institutions. Mortgage scams erode trust in real estate transactions, increase costs for legitimate buyers, and can lead to higher insurance premiums and stricter lending requirements. The collaborative efforts of federal agencies aim to educate consumers and enforce regulations that deter fraudsters, but vigilance at the individual level remains paramount to prevention.

Many mortgage scams target vulnerable populations, including first-time buyers, seniors, and those facing financial hardship. Scammers often exploit the urgency or desperation of homeowners by offering seemingly quick solutions that are too good to be true. Being informed about the variety of fraudulent schemes and understanding how to verify legitimate offers empowers consumers to make sound decisions and protect their assets effectively.

Understanding Mortgage Scams and Their Impact

Mortgage scams broadly consist of fraudulent schemes targeting homeowners and buyers at various stages of homeownership. The FBI categorizes these scams into “fraud for profit,” often perpetrated by industry insiders manipulating transactions, and “fraud for housing,” where borrowers misrepresent information to obtain loans. Both types cause significant financial damage and undermine trust in the housing market.

Statistics reveal the scale of the problem: the FDIC reports over $31 million lost to home loan modification scams in a single recent year. Closely related are mortgage closing scams, which surged by 1,100 percent between 2015 and 2017. These scams alone were responsible for nearly $1 billion in losses in 2017. The financial and emotional toll on homeowners can be devastating, emphasizing the need for awareness and prevention strategies.

Mortgage fraud not only results in monetary losses but also leads to prolonged legal battles and credit damage for affected homeowners. Victims often face difficulties in securing future financing or refinancing due to compromised credit scores and unresolved liens. Additionally, fraudulent transactions can delay legitimate sales or transfers, causing stress and uncertainty in the housing market. Recognizing the multifaceted impact of mortgage scams helps emphasize the importance of early detection and intervention.

The involvement of licensed professionals in fraud for profit schemes highlights vulnerabilities within the industry itself. When appraisers, brokers, or attorneys participate in fraudulent activities, they exploit their trusted positions and technical knowledge to deceive borrowers and lenders. This form of internal fraud complicates detection and necessitates improved oversight and consumer education to identify suspicious behavior during the mortgage process.

Common Types of Mortgage Scams

Mortgage closing scams, or wire fraud, involve criminals hacking into real estate professionals’ email accounts and sending falsified wiring instructions to homebuyers. Victims unknowingly wire down payments or closing costs to fraudulent accounts, often losing tens of thousands of dollars. These emails appear legitimate, making this scam highly effective.

Loan modification and foreclosure relief scams prey on homeowners struggling with payments. Scammers promise to stop foreclosures or modify loans but demand upfront fees or ask victims to stop paying their mortgage. Variations include lease-back scams where homeowners sign over deeds only to be evicted later, partial interest bankruptcy scams delaying foreclosure while collecting payments, and refinance scams that trick victims into transferring property ownership unknowingly.

Additional mortgage scams involve identity theft and synthetic identities, where fraudsters use stolen or fabricated personal information to obtain loans or refinance properties illicitly. Some scammers engage in occupancy fraud, falsely claiming a property as a primary residence to secure better loan terms or insurance rates. These deceptive practices can lead to foreclosure or legal disputes when uncovered, causing long-term harm to homeowners and lenders alike.

Another prevalent scam targets those refinancing their mortgages by offering predatory refinancing schemes with hidden fees, inflated appraisals, or unfavorable loan terms. Unsuspecting borrowers may unknowingly agree to loans that increase their debt burden or result in loss of equity. Recognizing these deceptive tactics and consulting with trusted professionals before refinancing are crucial steps in avoiding such pitfalls.

Identifying Red Flags in Mortgage Fraud

Fannie Mae highlights several red flags that may indicate mortgage fraud. Examples include occupancy fraud, where borrowers claim a property is a primary residence but intend it as an investment, and straw buyer schemes that use third parties to secure loans with falsified information. Non-arm’s length transactions, often between related parties, may hide inflated prices or other deceptive terms.

Other warning signs include property flipping through false appraisals, income fraud by overstating earnings, and appraiser identity theft where unlicensed appraisers assume licensed professionals’ identities. Synthetic identity fraud, involving fictitious identities created with real and fake data, is also a growing concern. Recognizing these signs before committing to a mortgage transaction can prevent major losses.

Additional indicators of potential mortgage fraud include sudden changes in loan application details, such as inconsistent income or employment history that cannot be verified. Requests for unusual payment arrangements or reluctance to provide documentation also warrant caution. Awareness of typical fraud patterns helps consumers and lenders scrutinize transactions more closely and avoid fraudulent schemes.

Industry insiders emphasize the importance of independently verifying all parties involved in a mortgage transaction. Confirming licensing credentials of appraisers, brokers, and attorneys, as well as cross-checking property valuations against market data, can uncover discrepancies. Being alert to pressure tactics or requests for secrecy during a transaction often signals fraudulent intent and should prompt further investigation.

Comparison of Legitimate Mortgage Assistance vs. Mortgage Scams

Understanding the difference between legitimate mortgage help and scams can prevent costly mistakes. Legitimate assistance is typically provided by HUD-approved housing counselors who offer free or low-cost services without demanding upfront fees. They do not guarantee outcomes but guide homeowners through options and documentation.

In contrast, mortgage scams often pressure victims to pay upfront fees, promise guaranteed foreclosure prevention, and request payments to third parties or unfamiliar accounts. Scammers may rush victims to sign documents without full disclosure or understanding. Verifying the source and carefully reviewing terms are essential safeguards.

Legitimate mortgage assistance programs operate transparently and provide verifiable contact information, often affiliated with government or nonprofit organizations. These counselors educate homeowners about realistic options, including repayment plans, refinancing, or loan modifications, based on individual circumstances. They also encourage clients to consult legal or financial advisors before making decisions.

Mortgage scams frequently use high-pressure sales tactics, unsolicited communications, and vague or incomplete disclosures. Victims may be asked to send money to untraceable accounts or sign documents that transfer property ownership unknowingly. Being skeptical of unsolicited offers and researching any organization thoroughly before engaging protects consumers from falling prey to fraudulent schemes.

| Feature | Legitimate Mortgage Assistance (HUD-Approved Counselor) | Mortgage Scams |

|---|---|---|

| Upfront Fees | No upfront fees; services are often free | Often demands upfront fees |

| Payment Instructions | Payments made directly to your established loan servicer | Requests payments to third-party or unfamiliar accounts |

| Guarantees | Offers guidance and options with no guaranteed outcomes | Guarantees to stop foreclosure or modify loans |

| Document Review | Encourages thorough review and understanding of documents | Pressures immediate signing, often with blank or incomplete forms |

| Communication | Transparent, verifiable contact information from government or nonprofit sources | Unsolicited offers via suspicious emails or phone calls |

| Source of Help | Government agencies and nonprofit organizations | Unregulated companies or individuals with no official credentials |

Steps to Prevent Mortgage Scams

Protecting yourself from mortgage scams requires vigilance and adherence to key safety practices. Always verify any wiring instructions or payment changes by contacting your trusted real estate or settlement agent using a previously established phone number. Never trust phone numbers or links in unsolicited emails, as scammers frequently spoof legitimate contacts.

Be cautious of unsolicited mortgage assistance offers, especially those demanding upfront fees or promising guaranteed foreclosure prevention. Legitimate housing counselors approved by HUD provide free assistance and never charge fees before results. Carefully read all documents before signing and seek legal advice if anything is unclear. Protect your personal information by avoiding sharing sensitive data over unverified channels and regularly monitor your credit reports and bank accounts for suspicious activity.

Another essential preventive measure is to maintain open communication with your mortgage lender or loan servicer. If you receive unexpected notices or requests for payment changes, contact your lender directly using verified contact information. Scammers often impersonate lenders to redirect payments or collect personal information. Staying informed about your loan status and payment schedule reduces the likelihood of falling victim to fraudulent schemes.

Consumers should also educate themselves about common scam tactics and stay updated on recent fraud trends by consulting federal agency resources. Participating in community workshops or seeking advice from trusted housing counselors can enhance awareness. Taking proactive steps such as securing email accounts with strong passwords and enabling two-factor authentication helps protect sensitive information from cybercriminals involved in mortgage fraud.

Frequently Asked Questions (FAQs)

How can I verify if a mortgage assistance company is legitimate?

Legitimate mortgage assistance is typically offered by HUD-approved housing counseling agencies that provide free or low-cost services. These counselors do not charge upfront fees or guarantee loan modifications. Be cautious of companies that pressure you to sign documents quickly or demand payment before services are rendered. You can find HUD-approved counselors by calling 1-888-995-HOPE (4673) or visiting the HUD website.

What should I do if I receive an email with new wiring instructions for my mortgage closing?

If you receive new wiring instructions via email, immediately contact your real estate agent or settlement agent using a phone number you have previously verified, not any provided in the email. Mortgage closing wire fraud caused nearly $1 billion in losses in 2017 alone. Do not click on links or call numbers in suspicious emails as scammers often spoof legitimate addresses.

Can I lose my home to a mortgage scam even if I’m not in foreclosure?

Yes. Some scams, such as refinance fraud or lease-back schemes, trick homeowners into signing over deeds without realizing it. This can lead to loss of property ownership even if mortgage payments are current. Always review documents carefully and consult legal advice if uncertain before signing any paperwork.

What are the warning signs of a loan modification scam?

Warning signs include demands for upfront fees, guarantees to stop foreclosure, advice to stop mortgage payments, requests to send payments to anyone other than your loan servicer, pressure to sign documents without full understanding, or claims of “government-approved” loan modifications. Legitimate assistance from HUD-approved counselors is free and does not require upfront payment.

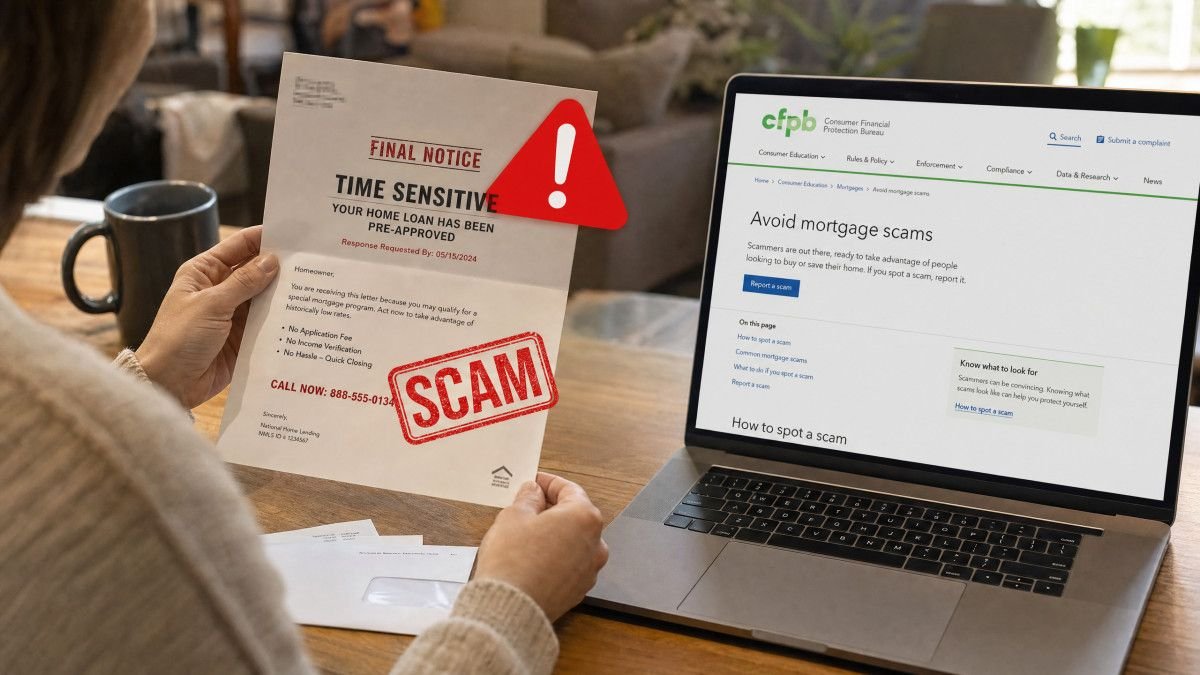

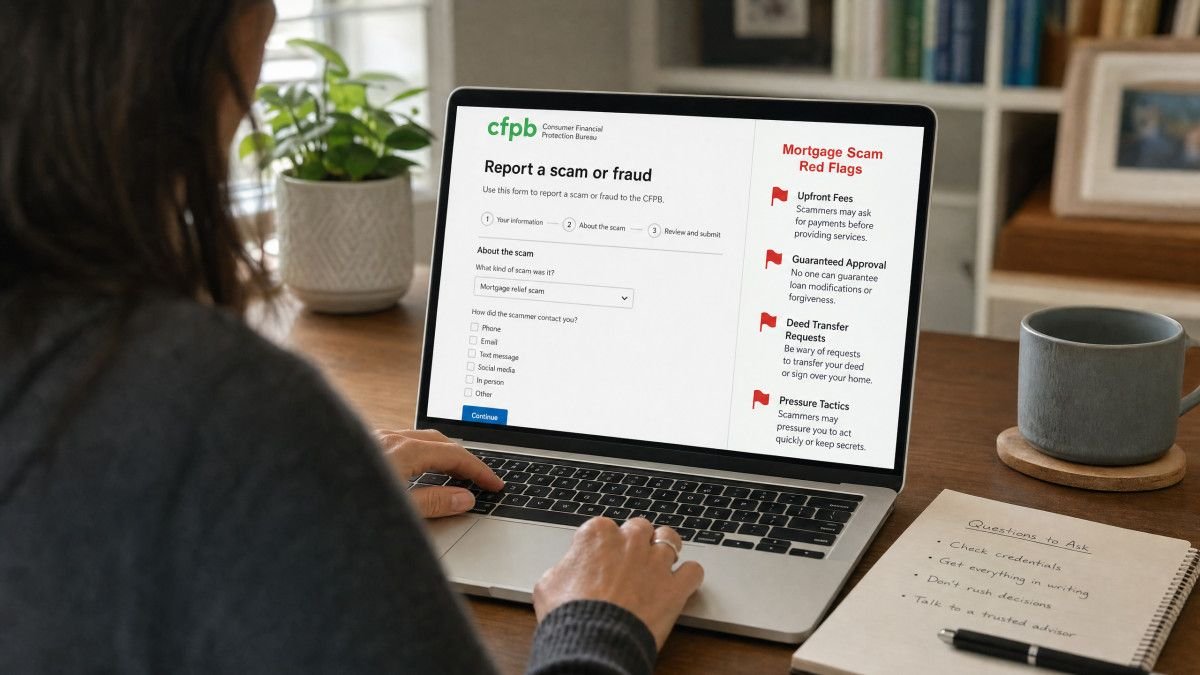

Where can I report a mortgage scam?

You can report mortgage scams to the FBI’s Internet Crime Complaint Center (IC3) at www.ic3.gov, the Consumer Financial Protection Bureau (CFPB), the U.S. Department of Housing and Urban Development (HUD), or the Federal Trade Commission (FTC). Prompt reporting helps authorities investigate and prevent further fraud.

Conclusion

Mortgage scams pose significant financial risks to homeowners and prospective buyers, with losses reaching billions annually. Awareness of common fraud tactics, such as wire fraud during closing and deceptive loan modification offers, is critical. Consumers must verify all communications, avoid upfront fees, and use trusted sources for mortgage assistance. Regularly monitoring credit and safeguarding personal information further reduces vulnerability to scams.

Federal agencies like the CFPB, HUD, FBI, and FTC provide valuable resources for identifying and reporting mortgage fraud. Homeowners facing difficulties should seek help only from HUD-approved counselors and remain cautious of unsolicited offers. Taking these precautions empowers consumers to protect their homes and financial security against increasingly sophisticated mortgage scams.