Per Astoria Charm Towson Management, the VA loan program, administered by the U.S. Department of Veterans Affairs, stands as one of the most impactful home financing tools available to eligible service members, Veterans, and their surviving spouses. Designed to make homeownership more attainable, VA loans are extended by private lenders but carry a government-backed guarantee. This guarantee reduces risk for lenders, enabling them to offer more favorable terms than conventional mortgage products.

Over the years, the VA loan program has grown tremendously in popularity and impact. In fiscal year 2025 alone, more than 525,000 VA loans were financed nationwide, with a combined loan volume exceeding $205 billion. These figures underscore the program’s widespread acceptance and effectiveness in addressing common financial challenges faced by veterans. Beyond the basic loan product, the VA provides additional protections and support services that help veterans navigate the complexities of home financing.

VA loans are remarkably versatile, offering options for purchase financing as well as refinancing, home improvements, and energy efficiency upgrades. The program’s flexible eligibility criteria, including adaptable credit and income standards, expand access to many borrowers who might otherwise struggle to secure traditional financing. Veterans benefit from a lifetime entitlement that can be utilized multiple times, including the possibility of holding concurrent VA loans under specific circumstances. This comprehensive approach highlights the VA loan’s role as a cornerstone in veteran homeownership support.

Key Benefits of VA Loans

VA loans provide an array of financial advantages that significantly lower the barriers to homeownership for those who have served. The elimination of a down payment requirement, the absence of private mortgage insurance, and competitive interest rates combine to facilitate more affordable monthly payments and reduce upfront costs. These aspects make VA loans a highly attractive alternative to conventional or FHA loans, especially for buyers who may have limited savings.

In addition to these primary benefits, VA loans offer more flexible credit standards, allowing many veterans to qualify despite imperfect credit histories. The program also limits closing costs and prohibits prepayment penalties, enabling borrowers to refinance or pay off their mortgages early without additional fees. These features, combined with the ability to use the entitlement multiple times during a lifetime, create a loan structure tailored to support veterans throughout their homeownership journey.

Another important benefit is the VA’s commitment to protecting veterans from predatory lending practices. The VA appraisal process ensures that homes meet minimum property standards, safeguarding borrowers from purchasing properties with significant defects. This protective measure helps maintain the long-term value and safety of the veteran’s investment. Additionally, VA loans are assumable under certain conditions, providing an advantage in resale markets when interest rates rise, as buyers can take over an existing favorable loan.

Comparison of VA Loans versus Conventional and FHA Loans

When compared with conventional and FHA loans, VA loans stand out in several key areas that impact cost and accessibility. Unlike conventional loans that typically require a 5% down payment or more, and FHA loans that mandate at least 3.5%, VA loans allow for 100% financing with no down payment. This feature alone can save veterans thousands of dollars upfront, making homeownership more immediately feasible.

Mortgage insurance requirements also differ significantly. Conventional loans require private mortgage insurance if the down payment is less than 20%, and FHA loans impose upfront and annual mortgage insurance premiums. VA loans, on the other hand, do not require monthly mortgage insurance, which can translate into monthly savings of over $100 on a $250,000 loan compared to other loan types. Interest rates for VA loans are typically lower as well, often ranging from 0.5% to 1% beneath conventional rates, which can result in tens of thousands of dollars saved over the life of the loan.

Credit requirements under VA loans are generally more lenient, accommodating veterans who might not meet the more stringent standards of conventional loans. While FHA loans are also known for flexible credit guidelines, the VA program often offers even greater flexibility. Closing costs on VA loans are capped and may include seller concessions of up to 4%, reducing out-of-pocket expenses at settlement. Additionally, VA loans do not impose prepayment penalties, allowing veterans to refinance or pay down their mortgage without penalty, whereas conventional loans sometimes include such fees. Lastly, VA loans can be assumable by qualified buyers, which is uncommon in conventional and FHA loans, giving veterans a potential advantage when selling their homes.

| Feature | VA Loan | Conventional Loan | FHA Loan |

|---|---|---|---|

| Down Payment | 0% (for eligible Veterans) [1, 2] | Typically 5% or more; 20% to avoid PMI [2] | Minimum 3.5% [2] |

| Mortgage Insurance | No PMI required [2, 3] | PMI required if down payment < 20% [2] | Upfront and annual mortgage insurance required [2] |

| Interest Rates | Often 0.5% to 1% lower than conventional [2] | Market-driven, can be higher than VA [2] | Generally competitive, but can be higher than VA [2] |

| Credit Requirements | More flexible credit standards [2] | Stricter, higher credit scores often required [2] | More flexible than conventional, less than VA [2] |

| Closing Costs | Limited by VA; seller concessions allowed up to 4% [2, 3] | Negotiable, can be higher [2] | Limited, but generally higher than VA [2] |

| Prepayment Penalty | None [2, 3] | Varies by lender and loan type | None |

| Assumability | Yes, under certain conditions [2] | Generally not assumable | Generally not assumable |

Eligibility Requirements for VA Loans

To be eligible for a VA loan, applicants must obtain a Certificate of Eligibility (COE) that confirms their service meets the VA’s standards. Generally, this involves meeting minimum active-duty service durations, which vary depending on the period and branch of service. National Guard and Reserve members also qualify if they meet specific service thresholds. There are exceptions for those discharged due to hardship or service-connected disabilities, which can broaden eligibility for certain veterans.

Surviving spouses may also qualify for VA loans if they meet certain conditions, such as receiving Dependency and Indemnity Compensation or if their veteran spouse was Missing in Action or a Prisoner of War. Beyond the military service requirements, applicants must satisfy credit, income, and occupancy guidelines set by the VA and participating lenders to ensure they have the financial capacity to repay the loan. These comprehensive eligibility criteria help maintain the program’s integrity while providing access to those who served.

The process for obtaining the COE has been streamlined through online portals and direct lender access, allowing many veterans to receive their eligibility confirmation quickly. This ease of access helps expedite the loan approval process and reduces administrative hurdles. Additionally, the VA works closely with lenders to clarify eligibility questions and assist veterans in gathering necessary documentation, further facilitating access to the program.

Additional VA Loan Features and Considerations

VA loans come with several unique features beyond competitive rates and favorable terms. One such feature is the prohibition of prepayment penalties, meaning veterans can pay off their loans early or refinance without incurring extra charges. This flexibility can lead to significant interest savings over time. The VA also offers foreclosure avoidance assistance, providing counseling and support for veterans facing financial difficulties, which helps reduce the risk of losing their homes.

The VA appraisal process is another critical aspect that protects borrowers by ensuring properties meet minimum safety and habitability standards. This helps prevent veterans from purchasing homes with significant defects or health hazards. The appraisal also helps determine the reasonable market value of the home, preventing overpaying and protecting both the borrower and lender.

Income calculations for VA loans consider military allowances such as Basic Allowance for Housing (BAH) and disability compensation, expanding the types of income that lenders accept. This broadened income recognition increases the chances that veterans with non-traditional income sources can qualify. The VA loan program includes a variety of loan types, such as purchase loans, cash-out and interest rate reduction refinance loans, renovation loans for home improvements, and energy-efficient mortgages that allow financing of energy-saving upgrades. This diversity enables veterans to use their VA benefit in ways that best fit their financial and housing needs.

Assumability is a notable feature allowing qualified buyers to assume the existing VA loan under certain conditions. This can be especially advantageous in markets with rising interest rates, as the assumable loan may carry a lower interest rate than current market offerings. This feature can enhance the resale value of the property and provide financial benefits to both sellers and buyers.

Frequently Asked Questions about VA Loans

Do I need a down payment for a VA loan?

Eligible veterans do not need to make a down payment when purchasing a home with a VA loan. This zero down payment benefit contrasts with conventional loans, which typically require at least 5% down, and FHA loans, which require a minimum of 3.5%. Eliminating the down payment requirement can save veterans thousands of dollars upfront, easing the financial burden of homeownership and making it accessible even for those with limited savings.

Is Private Mortgage Insurance (PMI) required with a VA loan?

VA loans do not require Private Mortgage Insurance (PMI), which is commonly mandated on conventional loans when the down payment is less than 20%, and FHA loans require upfront and annual mortgage insurance premiums. The absence of PMI on VA loans results in monthly savings estimated at around $100 or more on a $250,000 mortgage, reducing the overall cost of homeownership for veterans and making monthly payments more affordable.

Can I use my VA loan benefit more than once?

The VA loan benefit is a lifetime entitlement that veterans can use multiple times. After paying off a VA loan and selling the property, veterans can restore their entitlement for future home purchases. Additionally, if another eligible veteran assumes the loan, the original borrower’s entitlement may be restored. In certain circumstances, veterans may hold more than one VA loan simultaneously, increasing flexibility in managing multiple properties or relocations.

Are VA loan interest rates always lower than conventional loans?

VA loan interest rates are often 0.5% to 1% lower than conventional mortgage rates, which can translate into substantial savings over the loan term. However, interest rates vary with market conditions and individual borrower qualifications. While VA loans tend to offer more competitive rates, they are not guaranteed to always be the lowest, but their combination with other benefits makes them a compelling option for eligible borrowers.

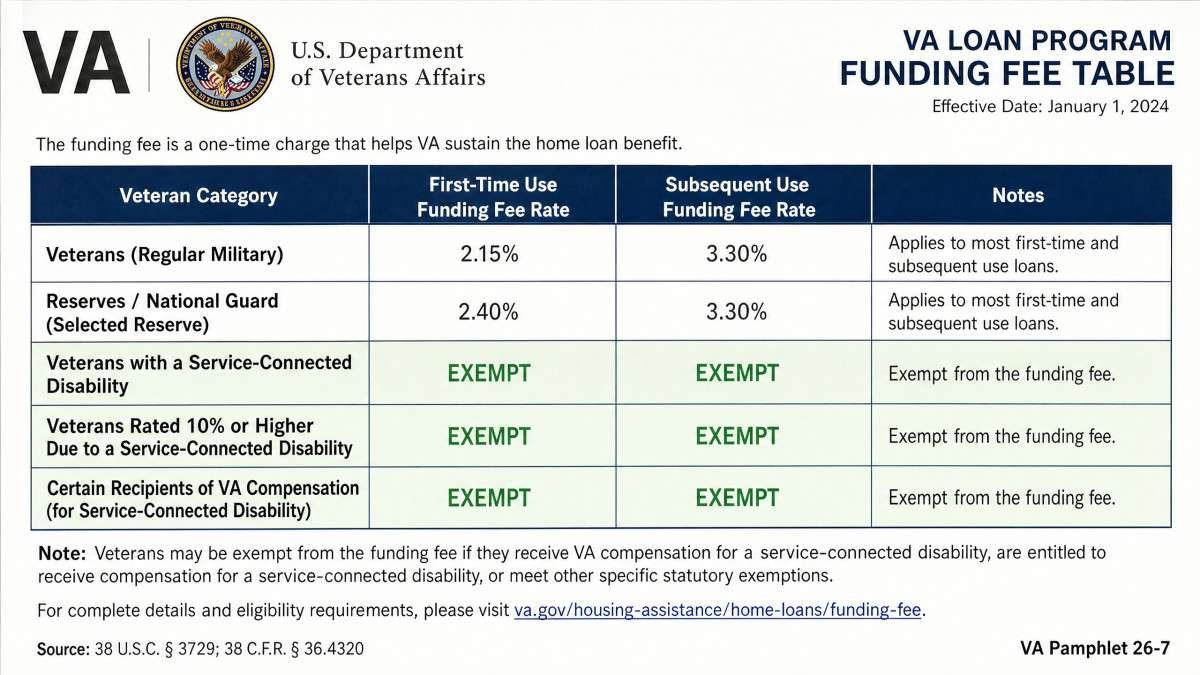

What is the VA Funding Fee, and can it be waived?

The VA Funding Fee is a one-time charge paid by borrowers to help sustain the VA loan program, typically ranging from 2.15% to 3.3% of the loan amount depending on factors such as first-time or subsequent use and down payment size. Certain veterans are exempt from paying this fee, including those receiving VA disability compensation for service-connected disabilities, active-duty Purple Heart recipients, and eligible surviving spouses. Waiving the funding fee reduces the overall cost of the loan for these veterans.

Conclusion

The VA loan program provides veterans, active-duty service members, and their families with exceptional home financing opportunities. By eliminating down payment requirements and private mortgage insurance, offering competitive interest rates, and maintaining flexible credit standards, the program lowers both upfront and ongoing costs associated with homeownership. Additional protections such as limited closing costs, no prepayment penalties, and foreclosure counseling create a supportive environment for borrowers throughout the loan lifecycle.

These combined features establish VA loans as a uniquely advantageous option for eligible borrowers. The program’s broad range of loan types, including purchase, refinance, renovation, and energy-efficient mortgages, along with the VA’s appraisal and eligibility safeguards, further enhance its value. Veterans looking to purchase or refinance a home can benefit greatly by utilizing their VA loan entitlement to maximize affordability and access.