Fixed-Rate Mortgages Overview

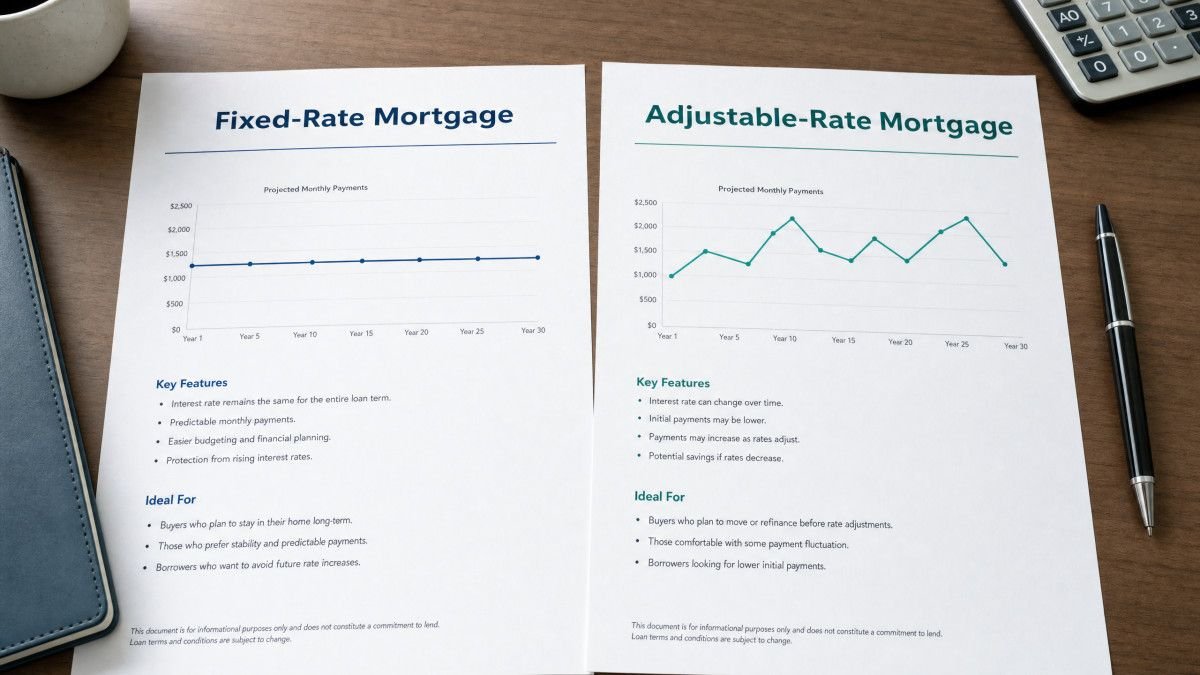

A fixed-rate mortgage features an interest rate that remains constant for the entire term of the loan, typically 15 or 30 years. This means the principal and interest portion of your monthly payment does not change, allowing for consistent budgeting. While property taxes and insurance can cause some monthly payment variation, the main loan payment is stable over time. Fixed-rate mortgages are often preferred by borrowers intending to stay in their homes for 10 years or more, as they offer long-term financial predictability and protection against rising interest rates.

One of the primary advantages of a fixed-rate mortgage is payment stability, which helps homeowners plan their finances without concern for interest rate fluctuations. Additionally, fixed-rate loans are straightforward, with clear terms from the outset. The main drawback is the typically higher initial interest rate compared to adjustable-rate mortgages, which can mean higher payments in the early years. Borrowers do not benefit from falling interest rates unless they refinance, which involves additional costs such as closing fees and appraisal expenses.

Adjustable-Rate Mortgages Overview

An adjustable-rate mortgage begins with a fixed interest rate for a specified initial period, commonly three, five, or ten years, after which the rate can adjust periodically—usually every six or twelve months. The interest rate is tied to an index such as the Secured Overnight Financing Rate (SOFR), plus a fixed margin set by the lender. For example, if the index is 3% and the margin is 2.5%, the borrower’s rate would be 5.5%. ARMs typically have caps that limit how much the interest rate can increase at the first adjustment, during subsequent adjustments, and over the life of the loan.

Adjustable-rate mortgages usually start with a lower interest rate than fixed-rate mortgages, resulting in lower initial monthly payments. This makes ARMs attractive for borrowers who expect to move or refinance before the adjustable period begins. However, the variability of payments after the initial fixed period introduces financial uncertainty, as rates can rise significantly depending on market conditions. ARMs are more complex due to their indexing, margin, and cap structures, and some include prepayment penalties if the loan is paid off or refinanced early.

Key Factors in Choosing Between Fixed and ARM

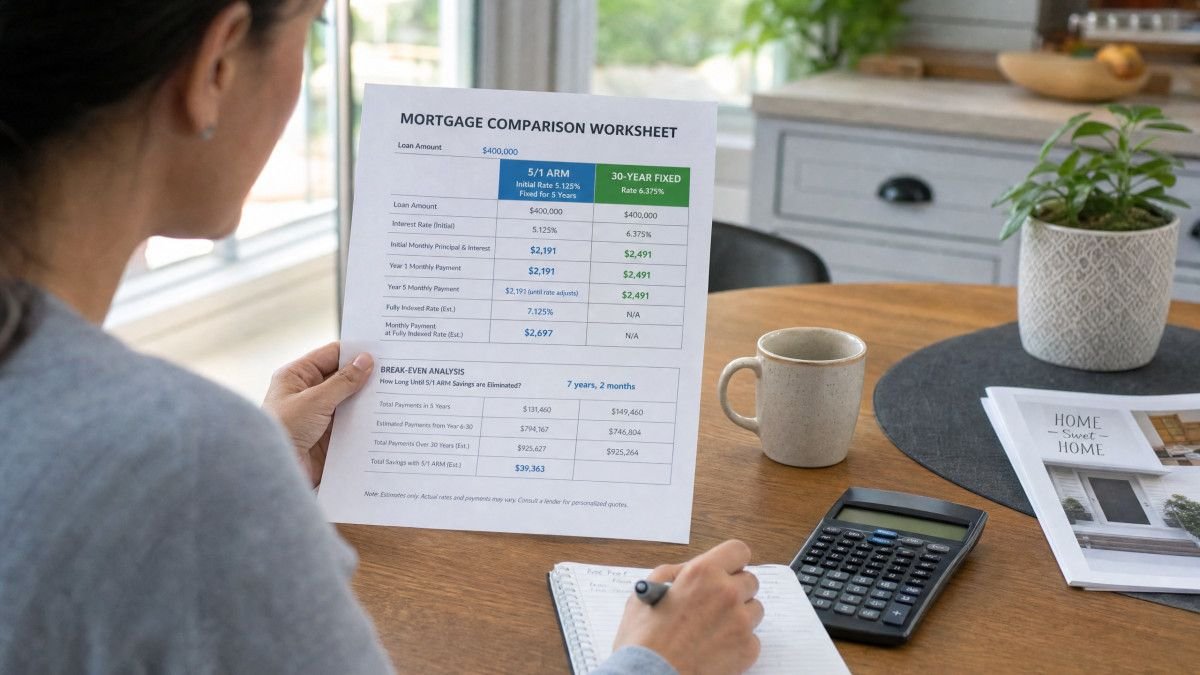

The decision between a fixed-rate mortgage and an adjustable-rate mortgage depends heavily on how long you plan to stay in the home. If your plan is to remain for 10 years or more, a fixed-rate mortgage offers stable payments and shields you from interest rate increases. Conversely, if you expect to move or refinance within five years, an ARM can provide lower initial payments and potential interest savings. This timing consideration is crucial because ARMs typically have initial fixed-rate periods matching common move timelines, such as a 5/6 ARM with five years fixed and adjustments every six months thereafter.

Another significant factor is the current interest rate environment. When long-term fixed rates are high, ARMs become more appealing due to their lower initial rates. If fixed rates are low, locking in a fixed-rate mortgage can provide long-term savings and payment certainty. Financial flexibility is also important; if you cannot comfortably absorb potential payment increases after the initial ARM period, a fixed-rate mortgage is generally safer. Additionally, understanding the complexity and potential prepayment penalties of ARMs is essential before deciding.

Comparison of Fixed-Rate and Adjustable-Rate Mortgages

This table summarizes the key features of fixed-rate mortgages and adjustable-rate mortgages to help clarify their differences and suitability based on borrower needs.

| Feature | Fixed-Rate Mortgage (FRM) | Adjustable-Rate Mortgage (ARM) |

|---|---|---|

| Interest Rate | Remains constant for the full loan term, often 30 years. | Fixed for an initial period (e.g., 5 years), then adjusts periodically based on an index plus margin. |

| Monthly Payment (Principal & Interest) | Stable and predictable throughout the loan term. | Can increase or decrease after the initial fixed period depending on market rates. |

| Initial Interest Rate | Typically higher, e.g., 6.5% for a 30-year FRM in a rising rate environment. | Typically lower, e.g., 5.0% for a 5/6 ARM initial period. |

| Best For | Long-term homeownership (10+ years) and budgeting stability. | Short-term ownership (less than 5 years) or when long-term fixed rates are high. |

| Complexity | Simple and straightforward loan structure. | More complex; involves understanding indices, margins, and rate caps. |

Common Misconceptions About Fixed and ARM Loans

One common misconception is that adjustable-rate mortgage interest rates always increase. In reality, ARM rates can decrease if the underlying index falls, although borrowers should prepare for the possibility of rising rates. Another mistaken belief is that refinancing an ARM before the rate adjusts is always easy. Refinancing depends on creditworthiness, home value, and market conditions; if the home’s value drops or credit worsens, refinancing may not be feasible. Misunderstanding these points can lead to unexpected financial challenges.

Additionally, some borrowers think fixed-rate mortgages guarantee a fully unchanging monthly payment. While principal and interest remain constant, total monthly payments may vary due to changes in property taxes or insurance premiums. Finally, some assume ARMs never have prepayment penalties. In fact, many ARMs include penalties if the loan is paid off or refinanced during the initial fixed-rate period, often lasting three to five years, and these penalties can amount to several thousand dollars.

Frequently Asked Questions

What is the main difference between a fixed-rate and an adjustable-rate mortgage?

The main difference is the interest rate structure. Fixed-rate mortgages have an interest rate that stays the same for the entire loan term, resulting in stable monthly principal and interest payments. Adjustable-rate mortgages start with a lower fixed rate for an initial period, after which the rate can change periodically based on a market index plus a fixed margin, causing payments to fluctuate.

How do rate caps work on an ARM?

Rate caps limit how much the interest rate on an ARM can increase or decrease. There are usually three caps: an initial cap limiting the first adjustment increase, a periodic cap limiting changes at each subsequent adjustment, and a lifetime cap capping the total possible increase over the loan’s life. For example, a 2/1/5 cap means the rate can increase by 2% at the first adjustment, 1% on subsequent adjustments, and no more than 5% total above the initial rate.

When is an ARM a good idea?

An ARM is beneficial if you plan to sell or refinance before the initial fixed-rate period ends, such as within five years on a 5/6 ARM. It also makes sense when long-term fixed rates are relatively high and you want to take advantage of lower initial payments. However, you should be comfortable with the risk of payment increases after the fixed period.

Can my monthly payment change with a fixed-rate mortgage?

While the principal and interest portion of the payment remains fixed, your total monthly payment can change if property taxes or homeowners insurance premiums increase or decrease. These costs vary independently of the mortgage interest rate and can cause fluctuations in the overall payment amount.

Are there penalties for paying off an ARM early?

Some adjustable-rate mortgages include prepayment penalties if you pay off or refinance the loan during the initial fixed-rate period, usually the first three to five years. These penalties can be several thousand dollars, so it is important to review your loan terms carefully before committing to an ARM.

Conclusion

Selecting between a fixed-rate mortgage and an adjustable-rate mortgage requires careful consideration of your financial goals, how long you plan to live in the home, and your tolerance for payment risk. Fixed-rate mortgages provide long-term payment stability and are generally better suited for homeowners intending to stay in one place for 10 years or more. Adjustable-rate mortgages offer lower initial rates and potential savings for borrowers planning shorter stays or looking to capitalize on lower initial payments.

Both mortgage types have advantages and disadvantages that impact monthly budgets and long-term costs. Understanding the structure of ARMs, including indices, margins, and rate caps, is essential to avoid surprises. Likewise, weighing the certainty of fixed payments against the potential cost savings of an ARM can help borrowers make an informed choice aligned with their financial situation and housing plans.