Federal laws such as RESPA and regulations under TRID ensure buyers receive clear disclosures about closing costs, including the Loan Estimate and Closing Disclosure documents. These protections help buyers compare lenders and avoid surprises at settlement.

Closing costs can vary widely depending on factors like the property’s location, the lender’s policies, and the complexity of the transaction. For instance, urban areas with higher property values often have correspondingly higher closing fees due to increased recording or transfer taxes. Additionally, buyers using specialized loan programs may encounter unique fees or premiums that affect their total closing costs. Understanding these variables helps buyers prepare more accurately for the financial commitment at closing.

Another important consideration is that some closing costs are paid upfront at closing, while others may be prepaid or escrowed for future payments, such as property taxes and homeowners insurance. This means buyers not only pay for services rendered during the transaction but also for expenses that cover periods after closing. Properly estimating these prepaid items is critical to avoid unexpected out-of-pocket costs immediately after moving into a new home.

Breakdown of Common Closing Costs for Buyers

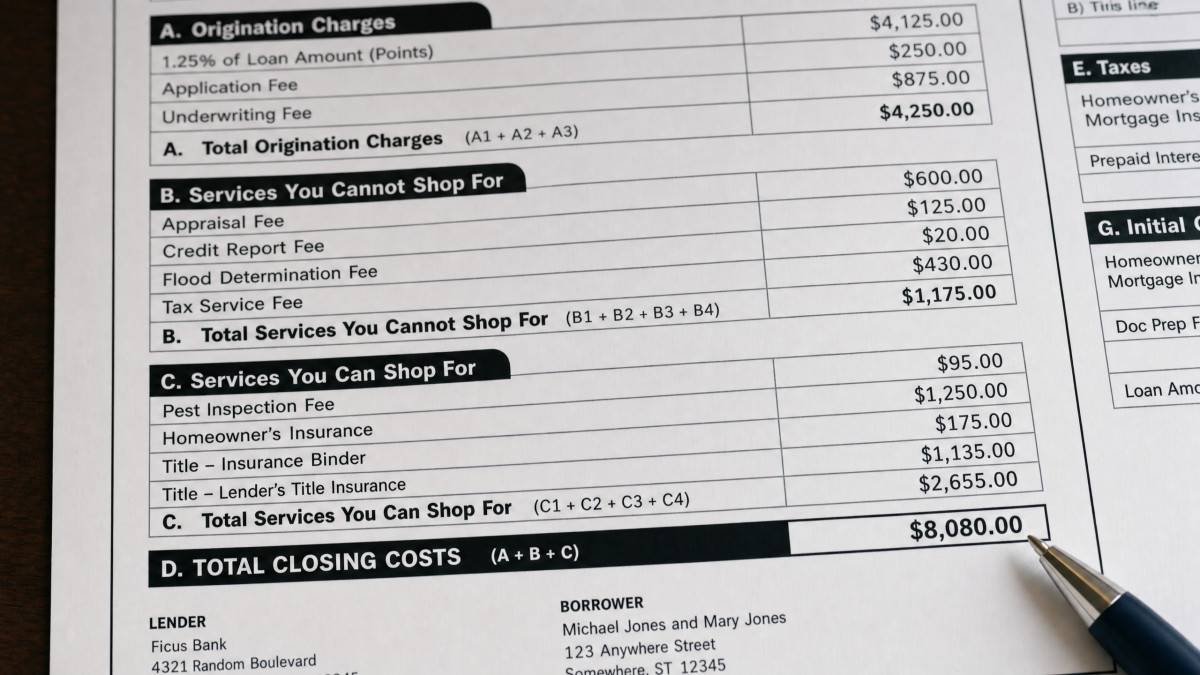

Closing costs for buyers consist of lender fees, third-party fees, and prepaid expenses. Lender fees include the loan origination fee, typically ranging from 0.5% to 1% of the loan amount, which covers administrative costs. An application fee, which can be up to $500, may also be charged. The credit report fee usually ranges from $50 to $110. Buyers may choose to pay discount points, where one point equals 1% of the loan amount and typically reduces the interest rate by 0.25%.

Third-party fees include appraisal costs of $300 to $600, or higher for VA loans ($650 to $1300), along with title search and title insurance fees. Title insurance protects both lender and buyer against title defects. Real estate attorney fees, closing or escrow fees, recording fees, survey fees, and tax service provider fees also contribute to third-party costs and vary by location. Prepaid expenses cover homeowners insurance premiums, often around $2,110 annually, prorated property taxes averaging $2,000 annually, prepaid interest from closing until the first mortgage payment, escrow deposits for future taxes and insurance, and potentially HOA dues.

Loan origination fees represent the lender’s charge for processing and underwriting the mortgage, and they can be negotiated in some cases. While the typical range is from 0.5% to 1%, some lenders might offer competitive rates or waive certain fees to attract borrowers. The credit report fee is usually a modest expense but is required to assess the buyer’s creditworthiness. Discount points are optional and represent a trade-off between upfront costs and long-term interest savings. Buyers should carefully evaluate whether paying points will be beneficial based on how long they plan to stay in the home.

Third-party fees often constitute a significant portion of closing costs. The appraisal fee is critical because it protects the lender by confirming the property’s market value. Title insurance, which includes both lender’s and owner’s policies, safeguards against title defects and potential legal disputes. While the lender’s title insurance is mandatory, the owner’s policy is highly recommended for buyers’ protection. Real estate attorney fees vary widely depending on state requirements; some states mandate attorney involvement, while others do not. Survey fees, required in some cases, ensure accurate property boundaries, which can prevent future disputes. Recording fees are set by local government agencies and cover the official documentation of property transfer.

Laws, Regulations, and Government Programs Affecting Closing Costs

Federal laws such as the Real Estate Settlement Procedures Act (RESPA) and the Truth in Lending Act (TILA) protect consumers by requiring transparent disclosures and prohibiting kickbacks or unearned fees. The TILA-RESPA Integrated Disclosure (TRID) rule mandates lenders provide a Loan Estimate within three business days of application and a Closing Disclosure at least three business days before closing, detailing final costs clearly.

Government-backed loan programs impact closing costs differently. FHA loans typically have closing costs between 2% and 6%, and include an Upfront Mortgage Insurance Premium (UFMIP) of 1.75% of the loan amount, which can be financed. Sellers can contribute up to 6% of the sales price or appraised value toward closing costs. VA loans generally have closing costs ranging from 3% to 5% of the loan amount, with a VA Funding Fee varying by circumstances (e.g., 2.15% for first-time use with less than 5% down). Disabled veterans are exempt. VA loans limit buyer-paid fees and allow sellers to pay all standard closing costs plus 4% in concessions.

RESPA also prohibits certain practices that can inflate closing costs, such as kickbacks between settlement service providers. This ensures fees are fair and competitive. The TRID disclosures, specifically the Loan Estimate and Closing Disclosure, give buyers a clear understanding of their expected costs early in the process and a final detailed accounting before closing, preventing last-minute surprises. These regulations have greatly improved transparency and consumer protection in real estate transactions.

Regarding government loan programs, FHA loans require mortgage insurance premiums to protect lenders against borrower default, which adds to closing costs but allows buyers with lower credit scores and smaller down payments to qualify. VA loans offer significant benefits, including no required mortgage insurance and limits on allowable fees, reducing upfront costs for qualified veterans. Additionally, sellers can negotiate concessions to help cover closing costs, which can be especially helpful for buyers with limited cash reserves. Understanding the specific rules for each program helps buyers plan their finances accordingly.

Comparison of Closing Costs by Loan Type

Closing costs vary significantly based on the type of mortgage loan. Conventional loans often require private mortgage insurance if the down payment is under 20%, FHA loans mandate mortgage insurance premiums including the upfront fee, and VA loans have unique funding fees and restrictions on allowable fees. Seller concessions and financing options for closing costs also differ among these loan types.

| Feature | Conventional Loan | FHA Loan | VA Loan |

|---|---|---|---|

| Typical Closing Costs | 2% – 5% of loan amount | 2% – 6% of purchase price | 3% – 5% of loan amount |

| Unique Fees | Private Mortgage Insurance (PMI) if down payment < 20% | Upfront Mortgage Insurance Premium (UFMIP) at 1.75% | VA Funding Fee (e.g., 2.15% for first use, <5% down) |

| Seller Concession Limits | 3% – 9% depending on down payment | Up to 6% of sales price or appraised value | Up to 4% in concessions; no limit on standard closing costs |

| Financing Closing Costs | Generally not allowed for purchase | UFMIP can be financed | VA Funding Fee can be financed |

| Non-Allowable Fees | None specific | None specific | Prohibits buyer from paying attorney fees, broker commissions, etc. |

Conventional loans, while typically having the lowest overall closing costs percentage, may require buyers to pay private mortgage insurance (PMI) if their down payment is less than 20%. This insurance protects the lender but increases monthly costs rather than upfront closing fees unless prepaid PMI is required. FHA loans have higher closing costs partly because of the mandatory mortgage insurance premiums, including the Upfront Mortgage Insurance Premium (UFMIP) of 1.75%, which can be financed but adds to the loan balance.

VA loans are distinct in that they generally have higher closing costs in percentage terms but no mortgage insurance requirement. The VA Funding Fee varies based on the borrower’s down payment and service history; disabled veterans are exempt from this fee. VA loans also limit the fees that buyers can be charged, prohibiting payment of broker commissions and attorney fees by the buyer, which can reduce out-of-pocket expenses. Sellers can contribute up to 4% in concessions, helping buyers cover closing costs or prepaid items.

Common Misconceptions About Closing Costs

A widespread myth is that closing costs are fixed and non-negotiable. In reality, many fees such as lender origination, appraisal, and title fees can be shopped for or negotiated. Comparing Loan Estimates from multiple lenders helps buyers find lower fees and better loan terms. Government recording fees are typically fixed, but other costs can vary.

Another misconception is that “no closing cost” loans mean no fees. Usually, these costs are either rolled into the mortgage balance or compensated by a higher interest rate, increasing total payments over time. Buyers also often confuse down payment with closing costs; these are separate expenses. For instance, FHA rules require the 3.5% minimum down payment to be separate from closing costs. Finally, many buyers believe they must pay all closing costs out of pocket, but sellers can contribute through concessions, and some fees like FHA’s UFMIP or VA Funding Fee can be financed into the loan.

Many buyers assume that all closing costs must be paid in cash at closing, but various loan programs and seller concessions can reduce upfront cash requirements. For example, FHA and VA loans allow certain fees to be rolled into the loan or paid by the seller, easing the buyer’s immediate financial burden. Additionally, buyers often overlook that prepaid expenses such as property taxes and homeowners insurance premiums are part of closing costs, which can sometimes be negotiated or prorated. Understanding the distinction between mandatory fees, optional fees, and prepaid items empowers buyers to better manage their cash flow.

Another common misunderstanding is that the disclosed closing costs are the final and only costs. Sometimes, buyers encounter additional fees post-closing, such as HOA transfer fees or outstanding utility bills, which are not included in the closing statement. Awareness of these potential extra expenses can help buyers plan more effectively and ask targeted questions during the closing process. Engaging experienced professionals and carefully reviewing all disclosure documents reduces the chances of unexpected costs.

Frequently Asked Questions (FAQs)

How much should I expect to pay in closing costs?

Buyers typically pay between 2% and 6% of the loan amount or home’s purchase price in closing costs. For a $300,000 home, this means budgeting between $6,000 and $18,000. The exact amount depends on loan type, lender, and location, so obtaining Loan Estimates early is recommended. Additionally, government-backed loans like FHA or VA loans may include unique fees such as mortgage insurance premiums or funding fees, which can affect the total.

Can I roll my closing costs into my mortgage?

Rolling closing costs into the mortgage depends on loan type. Standard purchase loans usually do not allow financing most closing costs. However, FHA loans permit financing the Upfront Mortgage Insurance Premium of 1.75%, and VA loans allow the VA Funding Fee (e.g., 2.15% for first-time users with less than 5% down) to be included in the loan amount. Conventional loans generally do not allow financing closing costs, except in certain refinance scenarios.

What is the difference between a Loan Estimate and a Closing Disclosure?

A Loan Estimate is provided within three business days of applying for a mortgage and offers an estimate of loan terms and closing costs. The Closing Disclosure is given at least three business days before closing and details the finalized costs and loan terms the buyer will pay at settlement. These disclosures are required by federal law to ensure transparency and allow buyers to compare offers and prepare financially.

Are closing costs tax-deductible?

Most closing costs are not tax-deductible. However, certain expenses paid at closing, such as prepaid mortgage interest (points) and property taxes, may be deductible. The deduction for mortgage insurance premiums expired at the end of 2021. Buyers should consult a tax professional for advice specific to their situation, as tax laws can be complex and subject to change.

How can I reduce my closing costs?

Closing costs can be reduced by comparing Loan Estimates from multiple lenders to find lower fees. Buyers can negotiate seller concessions where the seller pays part of the closing costs. Additionally, state or local homebuyer assistance programs may offer grants or loans to cover closing expenses. Choosing loan programs like VA loans, which limit buyer fees, can also help lower upfront costs. Being informed about which fees are negotiable and shopping around are key strategies.

Conclusion

Closing costs represent a significant but necessary expense for homebuyers, typically ranging from 2% to 6% of the purchase price. Understanding the components of these costs, including lender fees, third-party charges, and prepaid expenses, helps buyers budget appropriately. Federal laws and regulations ensure transparency through required disclosures like the Loan Estimate and Closing Disclosure, empowering buyers to make informed decisions and avoid unexpected fees.

Buyers can mitigate closing costs by shopping around for lenders, negotiating with sellers for concessions, and exploring financing options for certain fees within FHA and VA loan programs. Awareness of common misconceptions also helps prevent confusion about down payments, “no closing cost” loans, and payment responsibilities. Thorough preparation and understanding of closing costs contribute to a smoother homebuying process.