Choosing between a 15-year and 30-year mortgage is a pivotal financial decision that significantly affects the overall cost of homeownership and monthly budgeting, notes Streamline Property Management professionals. A 15-year mortgage requires higher monthly payments but offers lower interest rates and quicker loan payoff, while a 30-year mortgage provides more affordable monthly payments with a longer repayment horizon but results in substantially higher total interest costs. Understanding these differences is essential for aligning your mortgage choice with your financial situation and long-term objectives.

Each mortgage term presents distinct financial implications that extend beyond just monthly payments. The 15-year mortgage, with its shorter timeline, enables homeowners to build equity much faster, which can be beneficial if you plan to sell or refinance in the near future. On the other hand, the 30-year mortgage offers a degree of comfort and flexibility that can be important for those managing other financial priorities or uncertain income streams. Carefully assessing your personal circumstances will help determine which path best fits your lifestyle and goals.

Moreover, the choice between these mortgage terms can influence your overall financial health and future opportunities. A 15-year mortgage may free you from debt sooner, allowing for greater financial freedom and the ability to redirect funds towards retirement or other investments. Conversely, a 30-year mortgage’s lower payments can provide the breathing room needed to build emergency savings or invest in higher-yield opportunities. Balancing these considerations with your risk tolerance and financial discipline is key to making an informed decision.

Key Differences Between 15-Year and 30-Year Mortgages

The fundamental distinction between 15-year and 30-year mortgages lies in the loan term duration, which impacts monthly payments, interest rates, and total interest paid. A 15-year mortgage requires larger monthly payments but has a lower interest rate, resulting in significantly less interest over the life of the loan and faster equity accumulation. In contrast, a 30-year mortgage spreads payments over twice as long, making monthly payments smaller but increasing the overall interest burden and slowing equity growth.

Beyond just the payment size and rates, the amortization schedules differ considerably. With a 15-year term, a larger portion of each payment goes toward principal reduction early on, while the 30-year mortgage allocates more to interest in the initial years. This results in slower equity build-up for the longer term loan. Borrowers who intend to stay in their home for an extended period may find the accelerated equity growth of a 15-year loan particularly advantageous.

Additionally, the qualification process varies between the two loan types. Because of the higher monthly payment obligations on a 15-year mortgage, lenders often impose stricter debt-to-income ratio requirements, which can make qualifying for a 15-year loan more challenging for some borrowers. In contrast, the lower payments on a 30-year mortgage can make it easier to secure financing, especially for first-time buyers or those with other debt obligations.

Advantages of a 15-Year Mortgage

A 15-year mortgage offers considerable benefits for borrowers who can afford the higher monthly payments. One of the primary advantages is the substantial interest savings, often exceeding $100,000 compared to a 30-year loan on a typical principal amount. The lower interest rate on a 15-year mortgage also amplifies these savings. Additionally, the shorter term means the homeowner builds equity faster, which can be advantageous for refinancing or selling the property sooner.

Another benefit of a 15-year mortgage is the psychological and financial relief of being debt-free earlier, which can improve long-term financial security. This loan term also enforces a form of forced savings by requiring consistent, higher payments that reduce principal more quickly. This discipline can help homeowners avoid prolonged debt and achieve greater financial freedom in retirement or other life stages.

Moreover, having a 15-year mortgage can provide peace of mind by reducing exposure to interest rate fluctuations if you have a fixed-rate loan. The quicker payoff timeline also means you can reallocate funds to other financial goals much sooner, such as investing, travel, or paying for education. For many, the accelerated payoff schedule supports a more goal-oriented financial plan and can act as a motivator to maintain disciplined budgeting habits.

Disadvantages of a 15-Year Mortgage

The primary drawback of a 15-year mortgage is the significantly higher monthly payment, which can strain household budgets and reduce cash flow flexibility. This increased financial obligation may leave less room for other important expenditures, such as retirement contributions, emergency savings, or education expenses. If income is not stable or experiences a downturn, meeting these payments could become challenging, increasing financial stress.

Moreover, the opportunity cost of paying more monthly towards a mortgage can be considerable. Borrowers might be better off investing the difference at a higher return rather than locking the funds into home equity. This is particularly relevant for those with a diversified investment strategy or other high-priority financial goals. Therefore, the 15-year mortgage is less suitable for individuals with unpredictable income or limited financial reserves.

In addition, committing to higher payments reduces financial flexibility in the face of unexpected events such as job loss, medical emergencies, or major repairs. Some borrowers may find the pressure of larger monthly obligations restrictive, potentially leading to missed payments or financial hardship. It is essential to evaluate not only your current financial state but also your ability to sustain these payments over the long term before choosing a 15-year mortgage.

Advantages of a 30-Year Mortgage

A 30-year mortgage provides lower monthly payments, which enhances cash flow flexibility and budgeting ease for many borrowers. This affordability can be crucial for individuals with variable income, young families, or those prioritizing other financial goals such as retirement savings or funding education. The lower payment also makes it easier to qualify for a mortgage, as lenders consider debt-to-income ratios when approving loans.

Another benefit is the option to make extra principal payments when possible, allowing borrowers to reduce the loan term or interest paid without committing to a higher fixed monthly payment. This hybrid approach offers flexibility to adjust payments according to financial circumstances. Borrowers can also choose to invest the difference between the 15-year and 30-year payments, potentially achieving higher returns than the interest saved.

Additionally, the longer term can provide a sense of financial security by preserving cash for emergencies or other opportunities. The smaller required payments reduce monthly financial stress and allow homeowners to maintain a higher standard of living or fund other priorities. This flexibility is particularly valuable for those early in their careers or facing fluctuating expenses, offering a cushion that can help prevent financial strain.

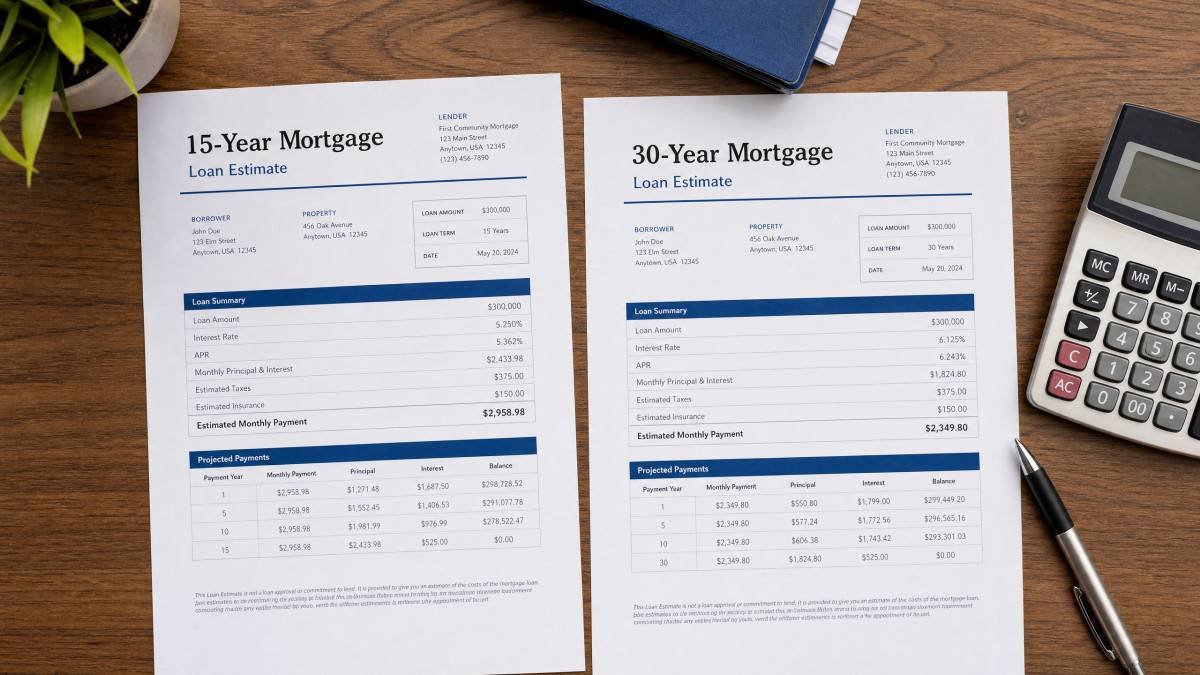

Comparison Table of 15-Year vs. 30-Year Mortgage

This table summarizes the key aspects of 15-year and 30-year mortgages based on a $300,000 loan example with respective interest rates of 6.5% and 7%.

| Aspect | 15-Year Mortgage | 30-Year Mortgage |

|---|---|---|

| Interest Rate | 6.5% | 7% |

| Monthly Payment | $2,613 | $1,996 |

| Total Interest Paid | $77,340 | $218,560 |

| Loan Payoff Time | 15 years | 30 years |

| Equity Build-up Speed | Faster | Slower |

| Cash Flow Flexibility | Lower | Higher |

| Qualification Ease | Harder | Easier |

Choosing the Right Mortgage for Your Financial Situation

The decision between a 15-year and 30-year mortgage should be guided by your income stability, existing debts, emergency savings, and financial priorities. Borrowers with a steady, high income, no significant high-interest debts, and a robust emergency fund are better positioned to handle the higher payments of a 15-year loan. This strategy helps reduce overall interest costs and accelerates debt freedom, which can be especially beneficial for those nearing retirement or seeking long-term financial security.

Conversely, borrowers with variable income, tighter budgets, or competing savings goals might find a 30-year mortgage more suitable. The lower monthly payment facilitates budgeting and allows funds to be allocated toward other priorities such as retirement accounts or college savings plans. Starting with a 30-year loan also provides flexibility to make extra payments as income allows, creating an effective compromise between cost savings and financial adaptability.

It is also advisable to consider your future plans when selecting a mortgage term. If you anticipate moving, changing jobs, or encountering major life events within the next decade, the flexibility of a 30-year mortgage might outweigh the cost savings of a 15-year loan. On the other hand, if you plan to stay in your home long-term and want to build equity rapidly, a 15-year mortgage could align better with your goals. Consulting with financial advisors or mortgage professionals can provide personalized insights based on your circumstances.

Frequently Asked Questions About 15-Year vs. 30-Year Mortgages

What is the rate difference between 15-year and 30-year mortgages?

Typically, 15-year mortgages carry interest rates about 0.5 to 0.75 percentage points lower than 30-year mortgages. This rate difference contributes significantly to the overall interest savings of the shorter loan term, as the borrower benefits from both a lower rate and a reduced repayment period. However, rates can vary based on lender policies and market conditions, so it’s important to shop around and compare offers.

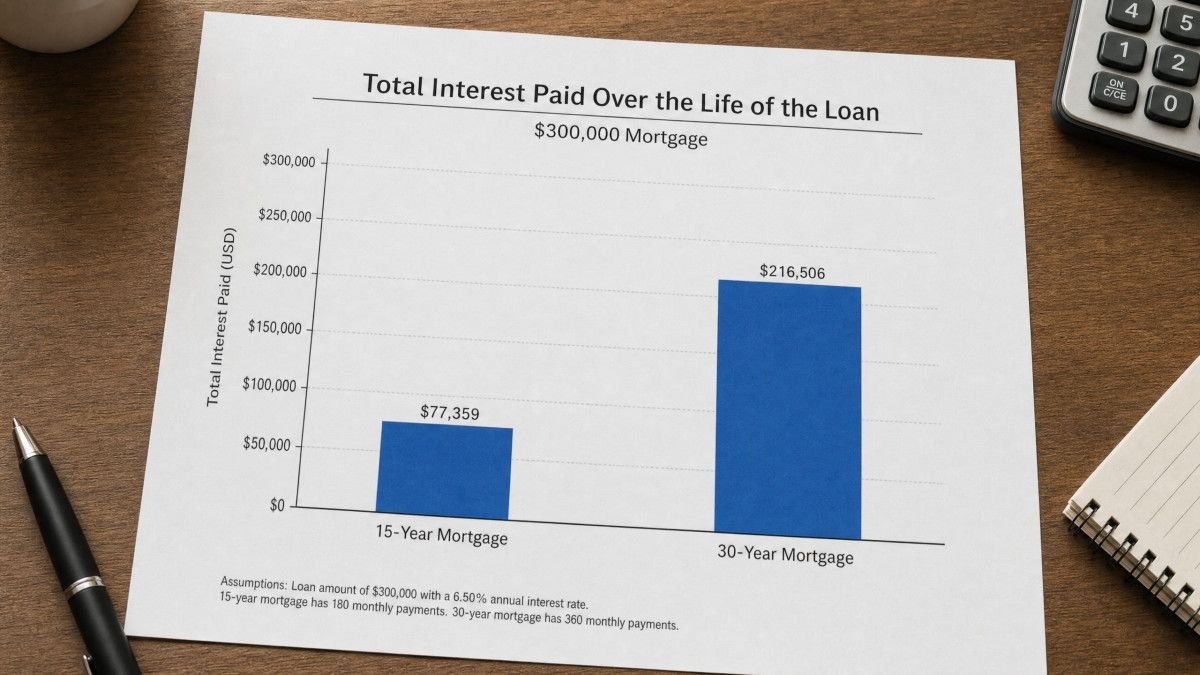

How much interest can be saved with a 15-year mortgage?

On a $300,000 loan, a 15-year mortgage can save over $100,000 in interest compared to a 30-year loan. This substantial saving results from faster principal repayment and the lower interest rate associated with the shorter term, which reduces the total interest accrued over the life of the loan. These savings can be used to build wealth or provide greater financial security over time.

How do monthly payments differ between the two terms?

Monthly payments on a 15-year mortgage are typically 25 to 35 percent higher than those on a 30-year mortgage. For example, a $300,000 loan might require $2,613 monthly under a 15-year term versus $1,996 for 30 years, reflecting the accelerated repayment schedule of the shorter loan. Borrowers should carefully evaluate their budget to ensure they can comfortably meet the higher payments.

Can I make extra payments on a 30-year mortgage?

Yes, borrowers can make additional principal payments on a 30-year mortgage to reduce interest costs and shorten the loan term. This approach offers flexibility by allowing lower required monthly payments while giving the option to pay off the loan faster if finances permit. It’s important to confirm with the lender that extra payments will be applied to principal without penalties.

Which mortgage term is better for me?

The better mortgage term depends on your income stability, cash flow needs, and financial goals. A 15-year mortgage suits those with strong, steady income and a desire to minimize interest costs, while a 30-year mortgage is preferable for those seeking lower payments and greater flexibility to focus on other financial priorities. Evaluating your personal circumstances and future plans will guide you toward the most suitable option.

Conclusion

The choice between a 15-year and a 30-year mortgage involves balancing immediate affordability with long-term cost savings. A 15-year mortgage offers lower interest rates, significant total interest savings, and faster equity build-up but demands higher monthly payments and reduced financial flexibility. In contrast, a 30-year mortgage provides more manageable monthly payments and the option to invest or allocate funds elsewhere, though it results in much higher interest costs and a longer repayment period.

Careful evaluation of your financial stability, cash flow needs, and long-term objectives is crucial to making the optimal mortgage decision. For those with stable incomes and strong savings, a 15-year mortgage may accelerate wealth building and reduce debt. Borrowers requiring flexibility or prioritizing other investments may find a 30-year mortgage more practical, especially if combined with a strategy of making extra payments when possible.