An adjustable-rate mortgage (ARM) is a home loan with an interest rate that changes periodically after an initial fixed-rate period, explains TJC Real Estate solutions. This structure causes monthly payments to vary over time, differing from a fixed-rate mortgage where the interest stays the same throughout the loan term. ARMs often start with lower interest rates compared to fixed-rate loans, making them appealing for certain borrowers depending on their financial plans and market conditions.

The defining characteristic of an ARM is its two-phase interest rate system. During the initial fixed period, the interest rate remains stable, providing predictable payments. After this phase ends, the rate adjusts at regular intervals based on a market index plus a margin determined by the lender. These adjustments can lead to either increases or decreases in monthly payments, depending on market rates and the loan agreement’s cap limits.

Understanding how ARMs are structured and how their interest rates are calculated is vital before committing to one. Different ARM types have varying fixed periods and adjustment frequencies, influencing the loan’s risk and affordability. Borrowers should also be aware of rate caps, which limit how much the interest rate can change over time. This knowledge helps evaluate whether an ARM suits an individual’s financial situation or long-term homeownership plans.

Many borrowers are attracted to ARMs because of their initial affordability and potential for savings, especially in environments where interest rates are expected to remain stable or decline. However, it is crucial to weigh the potential benefits against the risks associated with payment variability in the future. The choice between an ARM and a fixed-rate mortgage often hinges on personal circumstances such as the length of time one plans to remain in the home and their tolerance for financial uncertainty.

Additionally, the evolving landscape of financial markets can influence the attractiveness of ARMs. When market indexes fluctuate due to economic changes, the rates on ARMs will reflect these shifts, which means borrowers need to stay informed about economic trends to anticipate possible changes in their mortgage costs. This dynamic nature of ARMs makes them a more complex but potentially rewarding financing option for certain homebuyers.

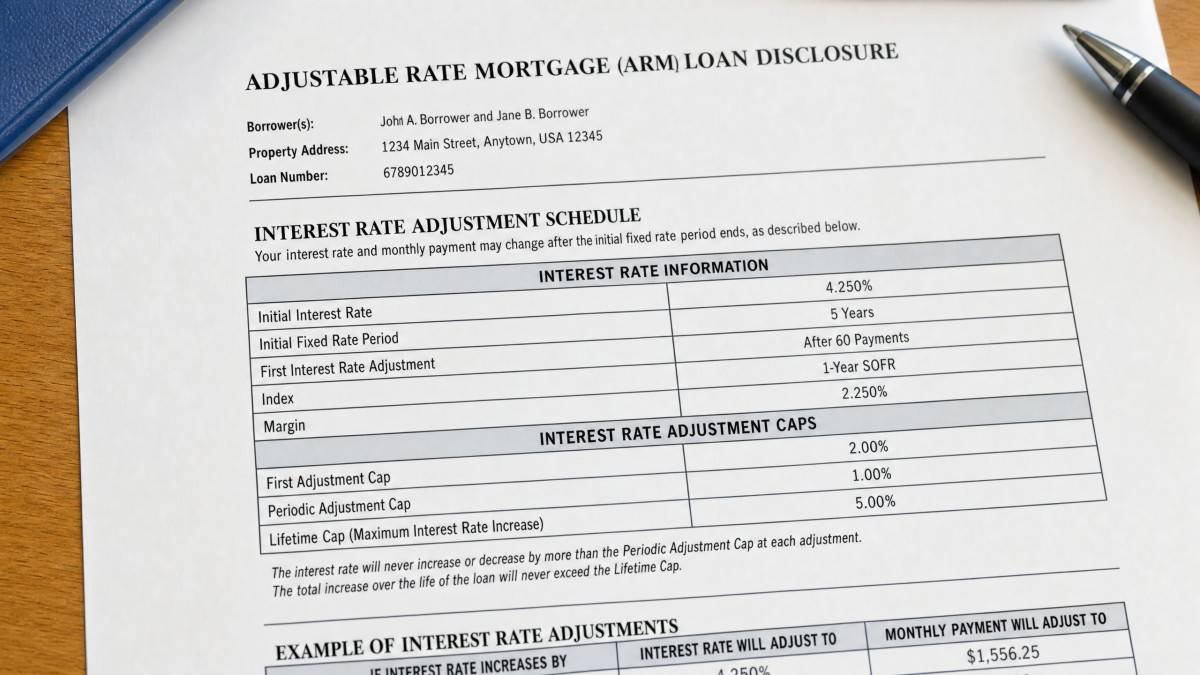

ARM Structure and Interest Rate Calculation

An adjustable-rate mortgage is typically described using a two-number format such as 5/1 ARM, where the first number represents the initial fixed-rate period in years, and the second number indicates how often the rate adjusts thereafter. For example, a 5/1 ARM means the interest rate is fixed for five years and then adjusts annually. Other common types include 7/1 and 10/1 ARMs, and sometimes 5/6 ARMs, which adjust every six months after the fixed period.

After the initial fixed phase, the interest rate is determined by adding a margin to a chosen index. The index is a market benchmark rate, such as the Secured Overnight Financing Rate (SOFR), which reflects current market conditions. The lender’s margin is a fixed percentage, usually between two and three percent, representing their profit. For instance, if the SOFR is 4% and the margin is 2.5%, the new interest rate becomes 6.5%. This combined rate dictates subsequent payment amounts until the next adjustment.

The process of calculating the adjusted interest rate involves reviewing the current value of the index on the adjustment date and applying the predetermined margin. Borrowers should understand that while the index fluctuates with market conditions, the margin remains constant for the life of the loan. This means that even if the index rate falls, the minimum interest rate will not drop below the sum of the margin and the index, unless a floor rate is specified.

Moreover, the timing of adjustments and the frequency can greatly affect the total interest paid over the life of the loan. Some ARMs allow adjustments annually, while others may adjust semi-annually or at other intervals, adding complexity to future payment planning. It is also important to note that some ARMs may offer initial teaser rates or introductory rates that are below the fully indexed rate, which can increase significantly once the fixed period ends.

Rate Caps and Protections in ARMs

Rate caps are limitations placed on how much an ARM’s interest rate can increase during certain periods, providing borrowers some protection against large payment shocks. These caps come in three forms: initial adjustment caps, periodic adjustment caps, and lifetime caps. The initial cap limits the rate increase at the first adjustment after the fixed period, often ranging from two to five percent. This cap helps prevent sudden steep increases immediately after the fixed phase ends.

The periodic cap restricts the amount the rate can change at each subsequent adjustment, commonly between one and two percent. Finally, the lifetime cap is the maximum total increase allowed over the life of the loan, typically five or six percent above the initial rate. Caps are often presented in a three-number format, such as 2/2/5, indicating the initial, periodic, and lifetime caps respectively. These features play a critical role in managing long-term risk for borrowers.

In addition to caps, some ARMs include rate floors that set the minimum interest rate, preventing the rate from falling below a certain level regardless of how low the index drops. This ensures lenders maintain a baseline return on their loan. Borrowers benefit from caps by having a ceiling on potential payment increases, which can aid in budgeting and financial planning. However, even with caps, the possibility of rising payments underscores the importance of understanding the terms fully before proceeding.

Borrowers should also be aware of margin adjustments in some ARMs, which might be subject to change under certain loan agreements. Though less common, these adjustments can impact the overall cost of borrowing. Knowing the exact terms around caps and margins can help borrowers anticipate the worst-case scenario and decide if the ARM fits their comfort level with financial risk.

| Feature | Description | Typical Range |

|---|---|---|

| Initial Fixed Period | Duration with fixed interest rate before adjustments begin | 3 to 10 years (commonly 5, 7, or 10 years) |

| Adjustment Frequency | How often the interest rate changes after the fixed period | Every 6 months to annually |

| Index | Market-based benchmark rate used to determine new interest rate | SOFR (Secured Overnight Financing Rate) |

| Margin | Fixed percentage added to index by lender | 2% to 3% |

| Rate Caps (Initial/Periodic/Lifetime) | Limits on interest rate increases during adjustments | 2/2/5 or 5/2/5 (percent) |

Advantages and Disadvantages of Adjustable-Rate Mortgages

Adjustable-rate mortgages offer certain advantages that may appeal to specific borrowers. One key benefit is the lower initial interest rate compared to fixed-rate mortgages, resulting in smaller initial monthly payments. This can improve affordability during the early years of homeownership, especially when prevailing fixed rates are high. ARMs are also beneficial for borrowers planning to sell or refinance before the adjustable period begins, allowing them to take advantage of lower rates without exposure to future increases.

However, ARMs come with notable disadvantages. Payment uncertainty after the fixed period can pose budgeting challenges, as interest rates may rise significantly. The complexity of ARM terms, including understanding indexes, margins, and caps, can be confusing for many borrowers. Additionally, there is refinancing risk: if interest rates rise or a borrower’s financial situation worsens, refinancing to a fixed-rate loan may not be feasible or affordable, potentially leading to higher payments or default risk.

Another advantage of ARMs is their potential for savings when market interest rates decline. Unlike fixed-rate mortgages, ARMs can adjust downward, which may reduce monthly payments during periods of falling rates. This flexibility can be appealing to borrowers who expect interest rates to decrease or remain stable over time. Moreover, the lower initial payments could allow homeowners to allocate funds toward other financial goals, such as investments or home improvements.

On the downside, the unpredictability of future payments can cause stress or financial strain, especially if rates increase rapidly or significantly. Borrowers who do not have sufficient financial buffers may struggle to meet higher monthly obligations. Moreover, the complexity of ARM contracts requires careful review and understanding, often necessitating professional advice to avoid surprises. The potential for negative amortization in certain ARM types, where payments do not cover accrued interest leading to increased loan balances, is another risk to consider.

Who Should Consider ARMs and Who Should Avoid Them

Adjustable-rate mortgages tend to suit borrowers with specific financial plans or risk tolerance. They are often appropriate for individuals who expect to sell their home or refinance within the initial fixed-rate period. Borrowers anticipating a rise in income or improved creditworthiness may also benefit, as they can manage potential payment increases later. ARMs can be a strategic choice when fixed interest rates are unusually high, allowing for lower initial borrowing costs.

Conversely, ARMs are less suitable for long-term homeowners who intend to stay in their property for many years, as they face the risk of rising payments. Borrowers on fixed or limited incomes may find fluctuating monthly payments difficult to manage. Those who prefer predictability or cannot tolerate financial uncertainty should avoid ARMs. Understanding individual financial circumstances and future plans is critical when deciding on an adjustable-rate mortgage.

Individuals with irregular or unstable income streams may find ARMs particularly challenging, as they might struggle to adjust to sudden increases in mortgage payments. Those nearing retirement or with limited savings may also want to avoid ARMs due to the risk of payment hikes during fixed or reduced income periods. On the other hand, borrowers who have a strong financial cushion and a flexible budget might find ARMs advantageous as they can absorb potential rate changes without major disruptions.

Financial goals and lifestyle preferences play a significant role in determining if an ARM fits a borrower’s needs. For example, someone who plans to upgrade homes frequently or relocate for work may benefit from the lower initial costs and the limited time spent in the adjustable period. Conversely, individuals who prioritize long-term stability and peace of mind may prefer the certainty offered by fixed-rate loans regardless of higher initial interest rates.

Frequently Asked Questions About ARMs

What does a 5/1 ARM mean?

A 5/1 ARM refers to a mortgage loan with a fixed interest rate for the first five years. After this period, the rate adjusts once every year based on a market index plus a lender’s margin. The initial five years provide payment stability, while subsequent annual adjustments can cause the rate to increase or decrease depending on market conditions.

Which index is commonly used for ARMs?

The Secured Overnight Financing Rate (SOFR) is the primary index used for adjustable-rate mortgages. It replaced LIBOR as the standard benchmark in 2023. SOFR reflects the cost of borrowing cash overnight collateralized by Treasury securities and is considered a reliable indicator of market interest rates.

What does a rate cap of 2/2/5 mean?

A rate cap of 2/2/5 represents limits on how much the interest rate can increase on an ARM. The initial cap of 2% restricts the increase at the first adjustment. The periodic cap of 2% limits changes at each subsequent adjustment. The lifetime cap of 5% is the maximum total increase allowed over the loan’s term above the original rate.

How do ARMs compare to fixed-rate mortgages?

Adjustable-rate mortgages usually offer lower initial interest rates than fixed-rate mortgages, which can reduce early payments. Fixed-rate mortgages provide predictable payments throughout the loan term, eliminating the risk of rising rates. ARMs carry payment variability risk after the fixed period, while fixed-rate loans maintain stable costs but may have higher initial rates.

When is it advantageous to choose an ARM?

Choosing an ARM is advantageous when a borrower plans to sell or refinance before the initial fixed period ends, avoiding potential rate increases. It also suits situations where fixed mortgage rates are high, and the borrower expects rates to decline or income to rise. ARMs are less suitable for long-term homeowners seeking payment stability.

Conclusion

Adjustable-rate mortgages offer a unique loan structure with an initial fixed-rate period followed by periodic interest rate adjustments based on market indexes and lender margins. Their lower introductory rates can provide affordability advantages for borrowers with specific financial plans, such as those intending to move or refinance within a few years. Understanding the detailed components of ARMs, including rate caps and adjustment schedules, is essential to managing potential payment fluctuations and risks.

While ARMs can be beneficial under certain circumstances, they also introduce uncertainty and complexity that may not suit all borrowers. Individuals considering an ARM should carefully assess their long-term housing plans, income stability, and risk tolerance. Knowledge of ARM mechanics helps borrowers make informed decisions aligned with their financial goals and capacity to handle changing mortgage payments.