Navigating the world of home finance often feels like learning a completely new language. You sit down to review a loan estimate for a new house, and immediately, two different percentages jump off the page, points out CHL Rentals team. One is labeled the interest rate, and right next to it is the Annual Percentage Rate, or APR. They are almost never the same number. This discrepancy is a common source of confusion for homebuyers trying to figure out exactly how much their new mortgage will cost.

The distinction between these two figures is not just a matter of financial jargon. It represents a fundamental difference in how lenders calculate the cost of borrowing money. The interest rate dictates your monthly principal and interest payment, while the APR provides a broader view of the total cost of the loan over its entire lifespan. Grasping this difference is essential for making informed decisions and accurately comparing loan offers from different financial institutions.

What is an Interest Rate?

The interest rate is the basic, annualized cost of borrowing the principal loan amount, expressed as a percentage. It does not include any additional fees or charges associated with securing the mortgage. This rate directly determines the portion of your monthly payment that goes toward interest rather than paying down the loan balance.

When a lender quotes you a 6.5% interest rate on a 30-year fixed-rate mortgage, they are telling you the baseline cost of the money you are borrowing. If you take out a $300,000 loan at that 6.5% rate, your monthly payment for principal and interest alone will be approximately $1,896. This figure is straightforward. It is the cost of the capital itself.

Interest rates are heavily influenced by broader economic factors, particularly the actions of the Federal Reserve and the bond market. Lenders also adjust the rate they offer you based on your personal financial profile. A borrower with a credit score of 780 will generally secure a lower interest rate than someone with a score of 650. The type of loan also matters. A 15-year mortgage typically carries a lower interest rate than a 30-year mortgage because the lender’s money is tied up for a shorter period, reducing their risk.

What is Annual Percentage Rate (APR)?

The Annual Percentage Rate (APR) is a comprehensive measure of the total yearly cost of a loan, expressed as a percentage. It includes the base interest rate plus other mandatory fees and charges associated with the mortgage, such as origination fees, discount points, and mortgage insurance premiums.

Because the APR rolls these additional costs into the calculation, it is almost always higher than the base interest rate. According to the Consumer Financial Protection Bureau, the APR is designed to give borrowers a more complete picture of what they will actually pay to secure the financing. For example, you might be offered a mortgage with a 6.5% interest rate, but after factoring in a 1% origination fee ($3,000 on a $300,000 loan) and $1,500 in other closing costs, the APR might jump to 6.75%.

It can be genuinely frustrating to navigate multiple loan offers, each with slightly different interest rates and a myriad of fees, making direct comparisons feel like a puzzle. You might see one lender offering a 6.25% interest rate with high upfront fees, resulting in a 6.8% APR. Another lender might offer a 6.5% interest rate with very low fees, resulting in a 6.6% APR. The APR helps level the playing field, allowing you to see which loan is actually cheaper over the long haul, assuming you keep the mortgage for its full term.

Why the Difference Matters for Homebuyers

Understanding the difference between APR and interest rate allows homebuyers to accurately compare loan offers and assess the true financial burden beyond just the monthly principal and interest. Relying solely on the interest rate can lead to unexpected costs at closing and over the life of the loan.

Imagine you are comparing two loan estimates. Loan A offers a tantalizingly low interest rate of 5.99%. Loan B offers a rate of 6.25%. At first glance, Loan A seems like the obvious choice. However, when you look closer, Loan A requires you to pay two discount points upfront—essentially prepaying interest to lower the rate—which costs $6,000 on a $300,000 mortgage. This pushes Loan A’s APR to 6.4%. Loan B, on the other hand, has zero points and minimal fees, resulting in an APR of 6.3%.

If you plan to stay in the home for 30 years, Loan B is actually the less expensive option overall, despite the higher initial interest rate. This is why the APR is a critical tool. It forces you to look past the marketing appeal of a low headline rate and consider the total cost structure. Sometimes, paying higher upfront fees for a lower rate makes sense if you plan to keep the loan for decades. If you plan to move or refinance in five years, those upfront costs might not be worth it, making a loan with a higher interest rate but lower APR the smarter financial move.

Factors Influencing APR and Interest Rate

Both the interest rate and the overall APR are determined by a combination of macroeconomic conditions, lender-specific pricing models, and the borrower’s individual financial profile, including credit score, down payment size, and the chosen loan term.

Your credit score is arguably the most significant personal factor. Lenders use it to gauge risk. A borrower with an excellent credit score, typically defined as 740 or higher, will qualify for the most competitive interest rates. A lower score indicates higher risk, prompting the lender to charge a higher interest rate to compensate. The size of your down payment also plays a role. Putting down 20% or more reduces the lender’s risk and often eliminates the need for private mortgage insurance (PMI), which directly lowers your APR.

Lender fees vary wildly. One bank might charge a flat $1,000 origination fee, while another charges 1% of the total loan amount. These variations directly impact the APR. It is sometimes baffling how two reputable institutions can offer such wildly different fee structures for the exact same loan product. This variability underscores the necessity of shopping around and requesting official Loan Estimates from at least three different lenders before making a commitment.

FAQ: Clarifying Common Questions

Is a lower interest rate always better?

A lower interest rate is not always better if it comes with excessively high upfront fees that inflate the APR. You must evaluate how long you plan to keep the mortgage to determine if paying those fees to secure the lower rate is financially advantageous.

Do all loans have an APR?

Yes, the Truth in Lending Act requires lenders to disclose the APR for consumer loans, including mortgages, auto loans, and credit cards. This federal regulation ensures borrowers have a standardized metric to compare the true cost of credit across different financial products.

What are common fees included in APR for a mortgage?

Common fees included in a mortgage APR are origination fees, discount points, mortgage broker fees, and private mortgage insurance (PMI) premiums. However, it typically does not include costs like appraisal fees, title insurance, or credit report fees.

Can my APR change over time?

Your APR can change over time if you have an adjustable-rate mortgage (ARM), where the base interest rate fluctuates based on market conditions. If you have a fixed-rate mortgage, your APR remains constant for the entire life of the loan.

Where can I find the APR on a loan offer?

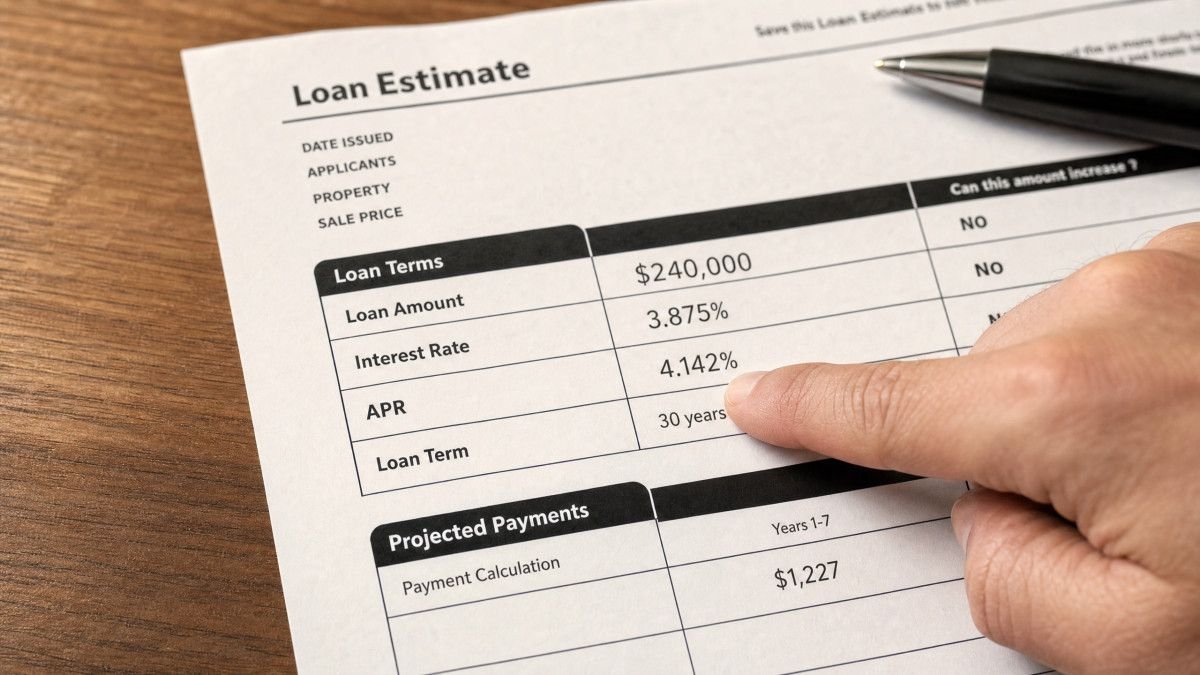

You can find the APR prominently displayed on page one of the official Loan Estimate document provided by the lender. It is typically located in the “Comparisons” section, specifically designed to help you evaluate the total cost of the loan.

How to Use APR When Comparing Loan Offers

When you receive multiple Loan Estimates, the APR is the single most useful number for a side-by-side comparison — but only if you use it correctly. Comparing APRs across loans works best when the loan terms are identical: same loan amount, same type (fixed vs. adjustable), and same repayment period. Comparing a 30-year fixed APR against a 15-year fixed APR will mislead you, because the shorter loan amortizes fees over fewer payments, which mechanically inflates the APR.

One practical approach is to request the Loan Estimate from at least three lenders on the same day. Mortgage rates shift daily, sometimes hourly, so comparing estimates pulled a week apart introduces noise that has nothing to do with lender pricing. Once you have same-day estimates in hand, line up the interest rates, the APRs, and the total closing costs side by side. The gap between a lender’s interest rate and its APR tells you how fee-heavy that lender is. A large gap — say, a 6.25% rate with a 6.55% APR — signals significant upfront costs. A small gap suggests a leaner fee structure.

There is one important caveat with adjustable-rate mortgages. The APR on an ARM is calculated using assumptions about future rate adjustments, and those assumptions may not match reality. The disclosed APR on a 5/1 ARM, for instance, is based on a projected rate path that regulators require lenders to use for disclosure purposes. It is not a guarantee of what you will actually pay after the initial fixed period ends. For ARMs, treat the APR as a rough directional indicator rather than a precise cost figure.

Conclusion

The interplay between interest rates and APRs forms the foundation of mortgage pricing. While the interest rate dictates your immediate monthly cash flow, the APR reveals the true, long-term financial commitment you are making. A low interest rate might catch your eye, but the APR tells you what that rate actually costs to obtain. By carefully analyzing both figures and understanding the fees that bridge the gap between them, you position yourself to select a mortgage that aligns with your specific financial timeline and goals. Navigating these numbers requires patience, but mastering them ensures you are not caught off guard by hidden costs at the closing table.