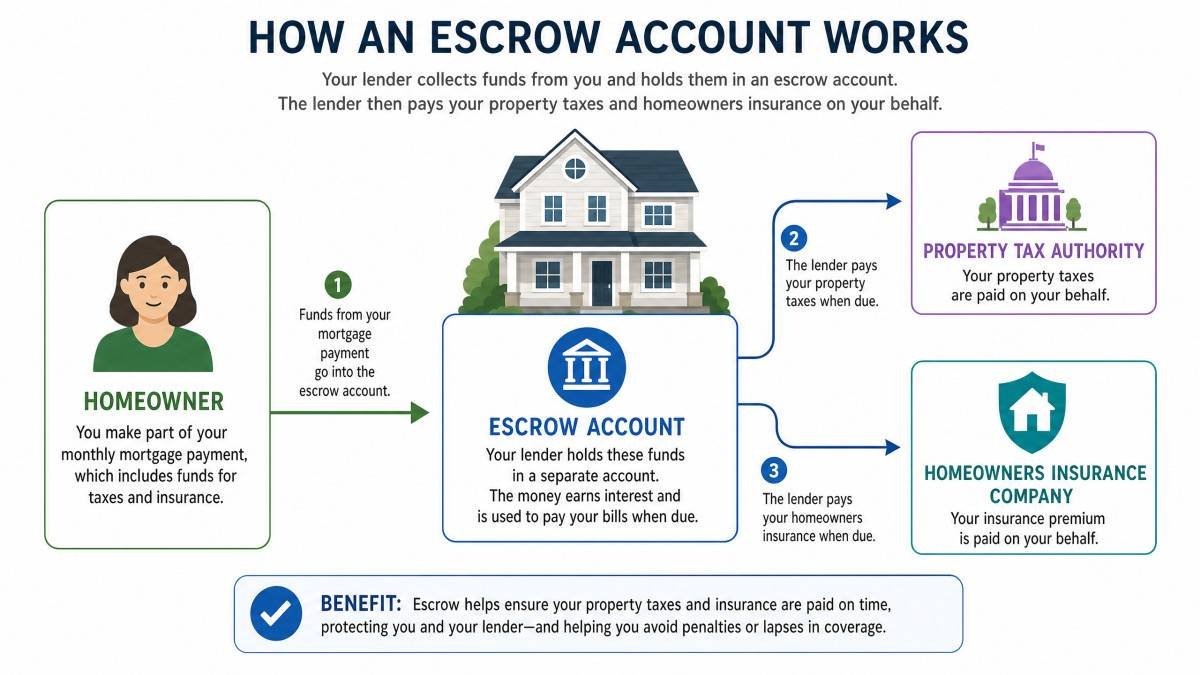

An escrow account is a specialized financial account used in mortgage lending to hold funds for property taxes, homeowners insurance, and sometimes other related expenses. It acts as a neutral holding place managed by the mortgage servicer, ensuring these bills are paid on time. Borrowers contribute a portion of these costs monthly alongside their mortgage payment so the servicer can disburse the funds when due. This arrangement protects both lenders and borrowers from missed payments or sudden large expenses, reports Abilene Leasing, a trusted Clyde property management.

Escrow accounts are particularly important when borrowers do not make a large down payment, or when government-backed loans like FHA, VA, or USDA loans are involved. By collecting funds gradually, escrow accounts reduce the risk of default and simplify bill management for homeowners. Regulatory guidelines, primarily under the Real Estate Settlement Procedures Act (RESPA), strictly govern how these accounts operate, including how servicers must conduct annual analyses and handle shortages or surpluses.

Understanding the purpose, rules, and mechanics of escrow accounts is essential for homeowners and prospective borrowers alike. These accounts influence monthly mortgage payments and can affect overall affordability. They also provide transparency through required annual statements and options to manage escrow shortages. This article explains what escrow accounts are, their regulatory framework, payment calculations, and how borrowers can interact with these accounts throughout their mortgage term.

Escrow Account Basics and Regulatory Framework

An escrow account is designed to collect and hold funds specifically for recurring property-related expenses, most commonly property taxes and homeowners insurance. Instead of paying these bills directly, the borrower pays the mortgage servicer a monthly amount that includes principal, interest, and the escrow portion. The servicer then holds the escrow funds in a trust account separate from the mortgage principal and interest payments. This separation ensures the escrow funds are used only to pay the designated bills.

The use of escrow accounts is mandated or strongly encouraged by lenders to protect their financial interest in the property. For loans insured or guaranteed by federal agencies such as the Federal Housing Administration (FHA), Veterans Affairs (VA), and the United States Department of Agriculture (USDA), escrow accounts are required regardless of down payment size. Conventional loans often require escrow if the borrower’s down payment is less than 20 percent. This protects the lender by making sure taxes and insurance are kept current, reducing the risk of liens or uninsured losses.

The Real Estate Settlement Procedures Act (RESPA), enforced through Regulation X (12 CFR Part 1024), governs escrow accounts for most federally related mortgage loans. RESPA sets rules on how servicers must manage escrow accounts, including limits on the amount of money that can be held as a cushion, requirements for annual escrow account analyses, and mandates for timely refunds of surplus funds. These protections were created to prevent borrowers from being overcharged or left uninformed about their escrow status.

Requirements and Conditions for Escrow Accounts

Escrow accounts are required for all FHA loans regardless of down payment amount, for VA and USDA loans, and for conventional loans with less than 20% down payment. This ensures that essential property-related bills are paid promptly, which protects both the borrower and lender. For conventional loans where the down payment is 20% or more, escrow accounts are usually optional and may be waived by the lender under certain conditions.

When escrow accounts are maintained, servicers typically collect one-twelfth of the estimated annual property taxes and insurance premiums each month. For example, if annual property taxes total $4,800 and homeowners insurance costs $1,200 annually, the borrower pays $500 monthly into the escrow account. This steady collection prevents the borrower from facing large lump sum payments when bills come due. The servicer then disburses these funds as required to cover the bills.

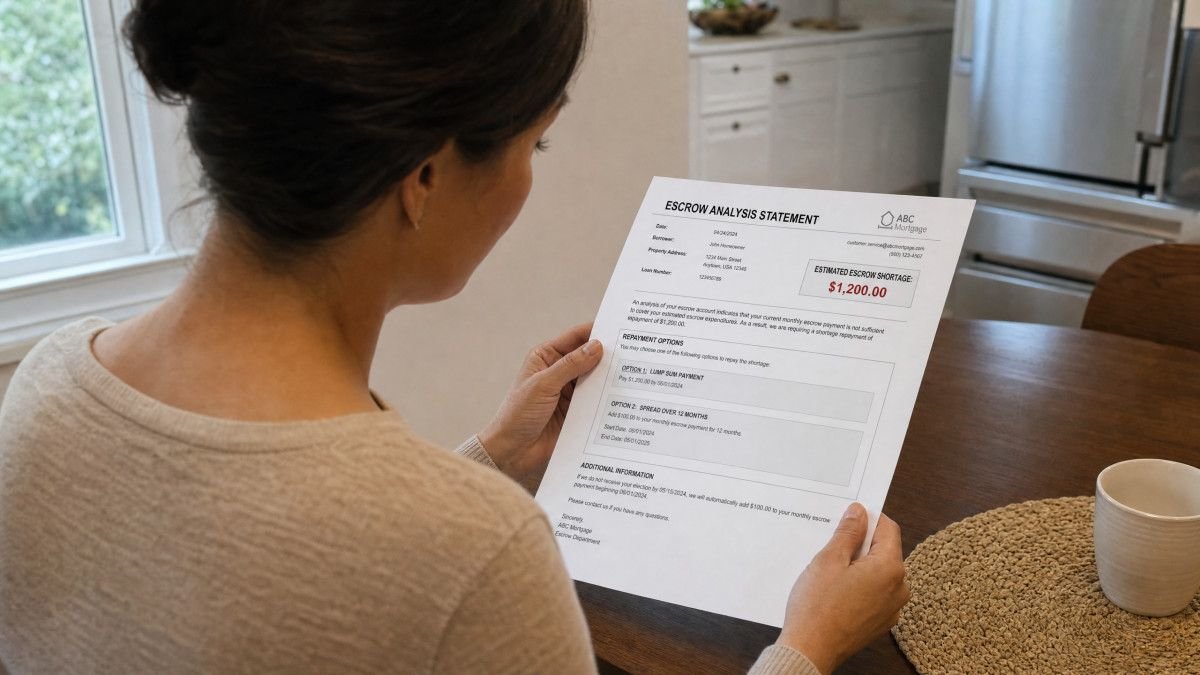

RESPA also allows servicers to maintain a cushion in the escrow account, but this cushion cannot exceed two months’ worth of escrow payments. This cushion protects against minor fluctuations in tax and insurance costs. If the escrow analysis reveals a shortage beyond this cushion, the borrower is offered the option to repay it either as a lump sum or spread over 12 months. Surpluses exceeding $50 must be refunded within 30 days, ensuring borrowers are not overcharged.

| Loan Type | Down Payment | Escrow Required | Notes |

|---|---|---|---|

| FHA | Any | Yes | Mandatory for life of loan if down payment < 10%; MIP and escrow removable after 11 years if ≥10% down |

| VA | Any | Yes | Escrow generally required; protects government guarantee |

| USDA | Any | Yes | Escrow mandatory to protect property and taxes |

| Conventional | < 20% | Yes | Escrow required to reduce lender risk |

| Conventional | ≥ 20% | Optional | Borrowers may waive escrow; lender may charge fee |

Calculating and Managing Escrow Payments

The monthly escrow payment is calculated by adding the total annual property tax amount to the annual homeowners insurance premium and dividing the sum by 12. For example, if a home’s annual property taxes are $4,800 and the insurance premium is $1,200, the total annual escrow payment is $6,000. Dividing this by 12 results in a monthly escrow payment of $500. This amount is collected along with the monthly principal and interest payments to form the total monthly mortgage payment.

Mortgage servicers conduct an annual escrow analysis to verify that the amount collected each month is sufficient to cover the upcoming year’s property tax and insurance bills. During this review, servicers compare the actual disbursements made with the amounts collected and projected expenses. If the analysis shows a shortage, borrowers may have to make up the difference either in a lump sum or through a 12-month repayment plan. Conversely, if there is a surplus greater than $50, the servicer must refund the excess or apply it toward future payments.

Under RESPA, servicers must provide borrowers with an escrow account statement within 30 days after completing the annual analysis. This statement details the previous year’s payments, current escrow balance, projected payments for the coming year, and any shortage or surplus. Borrowers can use this information to understand how their escrow funds are managed and to plan for any required repayments or refunds accordingly.

Escrow Waivers, Interest on Balances, and Borrower Rights

In some cases, borrowers with conventional loans and a loan-to-value ratio of 80% or less may be eligible to waive an escrow account. Lenders may grant escrow waivers to borrowers with good payment histories, but often charge a fee ranging from 0.125% to 0.25% of the loan amount annually for this privilege. Borrowers opting for a waiver take on the responsibility of paying property taxes and insurance premiums directly, which requires careful budgeting and timely payments to avoid penalties or liens.

Only 15 states require lenders to pay interest on escrow account balances. These states include California, Connecticut, Iowa, Maine, Maryland, Massachusetts, Minnesota, New Hampshire, New Jersey, New York, Oregon, Rhode Island, Utah, Vermont, and Wisconsin. In these states, mortgage servicers must credit interest earned on escrow funds to the borrower, either through a direct refund or by applying it to future escrow payments. In other states, no such requirement exists, so escrow balances typically do not earn interest for the borrower.

Borrowers also have rights under RESPA if the mortgage servicer fails to pay property taxes or insurance premiums from the escrow account, which could result in liens or insurance lapses. In such cases, borrowers can file complaints with the Consumer Financial Protection Bureau (CFPB). This federal agency oversees compliance with RESPA and can enforce corrective actions. Additionally, annual escrow statements provide transparency, enabling borrowers to monitor account activity and dispute errors promptly.

What is an escrow account?

An escrow account is a trust account managed by a mortgage servicer to collect and hold funds for property taxes and homeowners insurance. Borrowers pay a portion of these bills monthly along with their mortgage payments. The servicer disburses the funds when the bills are due, ensuring timely payment and protecting both the borrower and lender from missed or late payments.

Why are escrow accounts required on some loans?

Escrow accounts are required to protect the lender’s interest by ensuring property taxes and insurance premiums are paid on time. This prevents liens or uninsured losses that could jeopardize the lender’s security. Federal programs like FHA, VA, and USDA loans mandate escrow accounts, while conventional loans require them if the down payment is less than 20%.

How is the monthly escrow payment calculated?

The monthly escrow payment is calculated by adding the total annual property taxes and annual homeowners insurance premiums, then dividing by 12. For example, if annual taxes are $4,800 and insurance is $1,200, the total $6,000 divided by 12 results in a $500 monthly escrow payment included with the mortgage.

What happens if there is an escrow shortage?

If an annual escrow analysis shows a shortage greater than the allowed cushion (two months of payments), the borrower must repay the shortage either as a lump sum or spread over 12 months. The servicer must provide an escrow statement with these options so the borrower can select the preferred repayment method.

Can borrowers waive escrow accounts?

Borrowers with conventional loans and at least 20% down payment may request an escrow waiver if they have a strong payment history. Lenders may charge a fee for the waiver, and borrowers then become responsible for paying property taxes and insurance directly. This option is not available for most government-backed loans, which require escrow accounts.

Conclusion

Escrow accounts serve as an important safeguard in mortgage lending by ensuring that property taxes and insurance premiums are paid timely through a managed trust account. The monthly escrow payments are carefully calculated to cover annual bills evenly, reducing the risk of large lump sum payments for borrowers. Federal regulations like RESPA impose strict rules on escrow accounts, requiring servicers to conduct annual analyses, limit account cushions, and return surpluses promptly. These rules promote transparency and fairness.

While escrow accounts are mandatory for most government-backed loans and conventional loans with smaller down payments, borrowers with sufficient equity and good payment histories may waive escrow for conventional loans, often for a fee. Understanding the roles and management of escrow accounts enables borrowers to budget effectively and recognize their rights. Escrow accounts ultimately provide stability and protection for homeowners and lenders alike, ensuring key property expenses are consistently managed throughout the life of a mortgage.