The debt-to-income (DTI) ratio is the percentage of your gross monthly income that goes toward paying monthly debts. Mortgage lenders use this ratio to evaluate your ability to manage monthly payments and repay borrowed funds, points out Alta Property Management team. Calculating your DTI accurately is critical to determining your mortgage eligibility and understanding how much you can afford to borrow.

Because the DTI ratio reflects your financial obligations relative to your income, it serves as a vital indicator of your overall financial health. Lenders rely heavily on this metric to assess risk and ensure borrowers can handle additional debt without undue hardship. A well-managed DTI ratio often translates to more favorable loan terms, such as lower interest rates or reduced down payment requirements. Conversely, a high DTI can signal financial strain and increase the chances of mortgage denial or less advantageous loan conditions.

Mortgage lenders and loan programs have varying standards for acceptable DTI ratios, which can influence your borrowing options. Conventional loans, FHA loans, and VA loans each apply different maximum DTI limits based on underwriting guidelines and borrower qualifications. Understanding these limits and how your DTI is calculated can empower you to prepare your finances effectively, improve your mortgage application, and secure a loan that fits your financial situation.

Understanding Debt-to-Income Ratio and Its Importance

The debt-to-income ratio is a key metric lenders use to assess a borrower’s financial health and repayment capacity. It expresses what portion of your monthly gross income is committed to debt payments. This ratio helps lenders evaluate risk and decide if you can afford additional debt, like a mortgage.

A lower DTI suggests you have sufficient income relative to your debts, which generally increases the likelihood of mortgage approval and improved loan conditions. Conversely, a higher DTI indicates more of your income is tied up in debt, which may limit borrowing capacity or result in higher interest rates. Accurately calculating your DTI is essential for realistic mortgage planning.

Beyond mortgage qualification, maintaining a healthy DTI ratio contributes to long-term financial stability. A manageable DTI can reduce stress associated with debt repayment and improve your creditworthiness for future loans or credit lines. Lenders often view the DTI alongside other factors such as credit history and reserves, but it remains one of the most influential indicators of a borrower’s ability to meet their financial obligations consistently.

Step-by-Step Calculation of Your Debt-to-Income Ratio

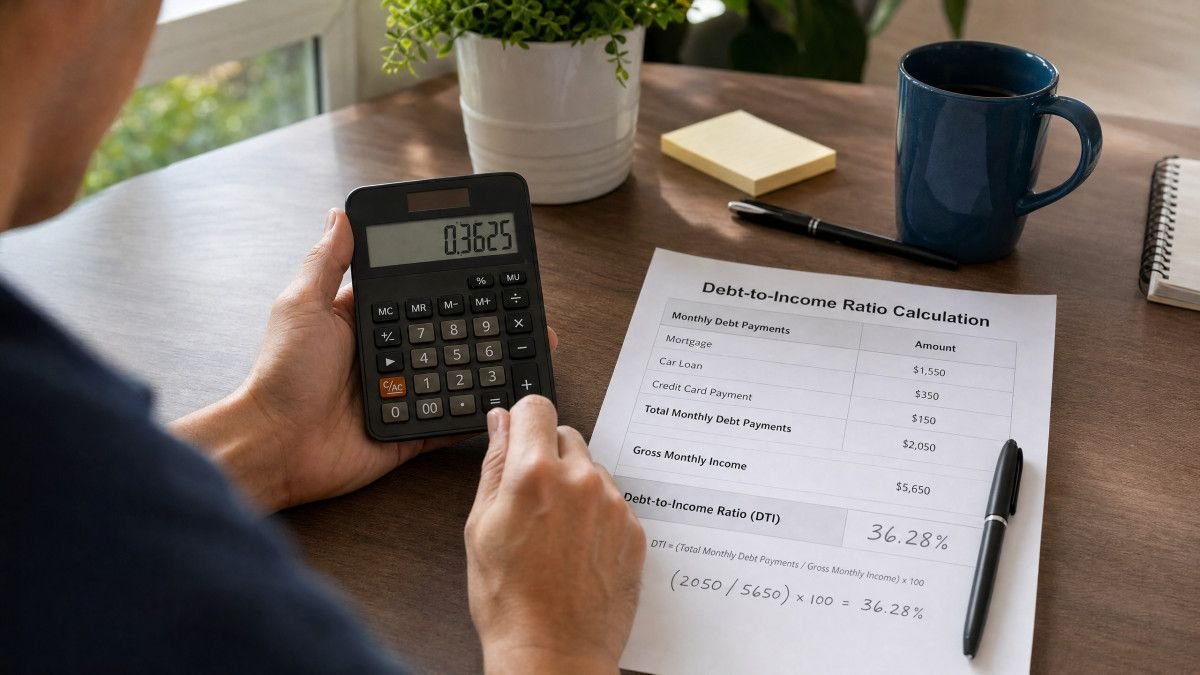

Calculating your debt-to-income ratio involves summing all monthly debt obligations and dividing that total by your gross monthly income. Start by adding up recurring debts such as mortgage payments (including principal, interest, taxes, and insurance), car loans, student loans, credit card minimum payments, and any other installment debts. Lenders also include alimony or child support payments lasting longer than ten months and net rental property losses.

Next, determine your gross monthly income, which is your total income before taxes and deductions. This may include salary, overtime, bonuses, commissions, self-employment income, Social Security or disability payments, and consistent rental income. Once you have these numbers, divide your total monthly debt payments by your gross monthly income and multiply by 100 to express the ratio as a percentage.

For example, if your total monthly debt payments equal $2,000 and your gross monthly income is $6,000, your DTI ratio is (2,000 / 6,000) × 100 = 33%. This figure helps lenders understand how much of your income is already allocated to debts and whether you can afford additional mortgage payments.

It is important to include all relevant monthly debt obligations accurately. For debts such as credit cards, lenders typically use the minimum monthly payment or a calculated percentage of the outstanding balance, depending on the lender’s policies. Similarly, installment loans are counted according to their monthly payment amount. Accurately capturing all recurring debts ensures a precise DTI calculation, which improves your chances of a smooth mortgage approval process.

Debt-to-Income Ratio Limits for Common Mortgage Loan Types

Different mortgage loan programs have varying maximum DTI limits that borrowers must meet for approval. Conventional loans manually underwritten by Fannie Mae usually require a total DTI of 36%, which can increase to 45% if the borrower satisfies specific credit score and reserve requirements. Automated underwriting through Desktop Underwriter (DU) can allow DTI ratios up to 50%.

FHA loans typically have a maximum DTI of 43%, but with strong compensating factors and approval by automated underwriting systems, borrowers may qualify with ratios up to 50-57%. VA loans recommend a DTI around 41%, but the Department of Veterans Affairs treats this as a guideline rather than a strict limit. Lenders may approve loans with DTIs as high as 65-70%, especially if the borrower demonstrates sufficient residual income.

These varying DTI limits highlight how underwriting criteria differ based on the loan program and borrower profile. For example, Fannie Mae’s Eligibility Matrix outlines specific conditions under which a higher DTI is acceptable, including minimum credit scores and liquid asset reserves. Meanwhile, VA loans focus heavily on residual income, which is the amount left over after monthly debts and living expenses, allowing for flexibility in approving borrowers with higher DTIs but strong income stability.

| Loan Type | Typical Maximum DTI | Maximum DTI with Compensating Factors | Key Considerations |

|---|---|---|---|

| Conventional (Manual Underwriting) | 36% [2] | Up to 45% [2] | Requires specific credit score and reserve requirements for higher DTI [2]. |

| Conventional (Automated Underwriting) | Up to 50% [2] | N/A | Underwritten through Desktop Underwriter (DU) [2]. |

| FHA Loan | 43% [3] | Up to 50-57% [3] [4] | Higher DTIs require strong compensating factors and AUS approval [3]. |

| VA Loan | 41% (Recommended) [6] [7] | Up to 65-70% [8] [9] | Focuses heavily on residual income; DTI is a guide, not a strict limit [6]. |

Common Misconceptions About Debt-to-Income Ratio

A common misconception is that a high DTI automatically disqualifies you from mortgage approval. In reality, lenders consider compensating factors such as credit scores, cash reserves, and down payments. Government-backed loans like FHA and VA tend to allow higher DTIs when these factors are strong, making approval possible even with ratios above typical limits.

Another misunderstanding is that all debts are treated equally in DTI calculations. Only recurring monthly debts are included. Non-recurring expenses or debts with fewer than ten months remaining are usually excluded unless they significantly affect repayment ability. Additionally, consistent income sources such as bonuses or commissions may be included if verifiable, expanding the borrower’s qualifying income.

Some borrowers also believe that utility bills, groceries, or other living expenses factor into the DTI calculation, but these costs are excluded since they are not considered debt obligations. This distinction allows lenders to focus on fixed financial commitments rather than variable monthly expenses. Understanding which debts are counted and how income is calculated helps borrowers provide accurate information and better estimate their qualifying DTI.

Finally, many assume that the DTI ratio is a fixed number across all lenders and loan programs. However, underwriting guidelines vary significantly, and lenders may offer flexibility based on overall borrower strength and market conditions. Being aware of these nuances can guide borrowers in selecting loan programs that best suit their financial profile and goals.

Frequently Asked Questions About Debt-to-Income Ratio

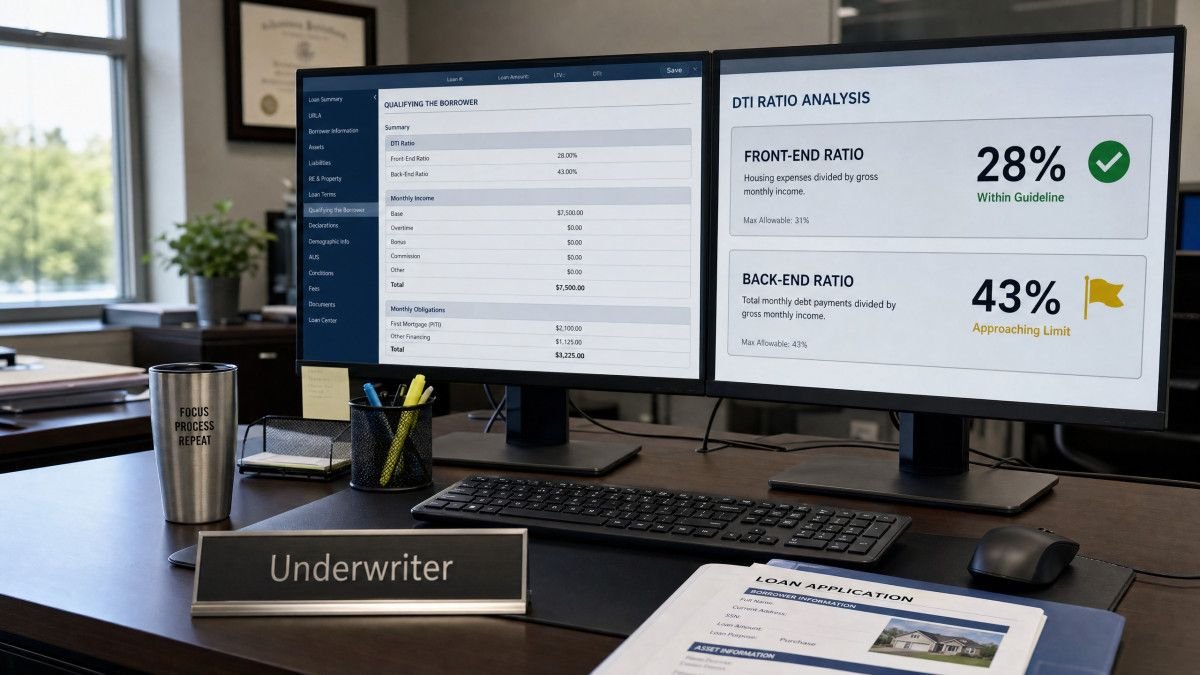

What is the difference between front-end and back-end DTI?

The front-end DTI ratio calculates the percentage of your gross monthly income spent on housing expenses, including mortgage principal, interest, property taxes, and homeowners insurance (PITI). The back-end DTI ratio includes all monthly debt obligations, such as credit card payments, auto loans, student loans, and the proposed housing payment. Lenders typically focus more on the back-end DTI when evaluating mortgage applications to assess total debt burden. Front-end ratios are often capped lower, such as 31%, while back-end ratios can be higher depending on loan type and compensating factors.

Does my credit score affect the maximum DTI allowed?

Yes, credit scores significantly influence the maximum DTI a lender will accept. For example, Fannie Mae allows a maximum DTI of 36% for manually underwritten loans but permits up to 45% if the borrower meets specific credit score and reserve requirements. Higher credit scores give lenders confidence to approve loans with elevated DTI ratios, improving borrowing flexibility. Conversely, lower credit scores may result in stricter DTI limits or require additional documentation and compensating factors to secure loan approval.

Are utility bills or groceries included in my DTI calculation?

No, utility bills, groceries, health insurance premiums, and other living expenses are excluded from the DTI calculation. DTI considers only recurring debt obligations such as loan payments, credit card minimums, alimony, or child support. This distinction ensures that essential living expenses outside of debts do not negatively impact mortgage qualification. Lenders focus on fixed monthly obligations that directly impact your ability to repay debts.

How can I lower my DTI ratio before applying for a mortgage?

You can lower your DTI by reducing monthly debt payments or increasing your gross monthly income. Paying off credit card balances or small loans, avoiding new debt, and increasing income through additional work or raises are effective strategies. Lowering your DTI improves mortgage approval chances and may result in better loan terms. Additionally, consolidating debts to reduce monthly payments or refinancing existing loans can also help improve your DTI ratio.

Do student loans in deferment count towards my DTI?

Yes, student loans in deferment are generally included in your DTI calculation. Lenders estimate a monthly payment based on a percentage of the outstanding balance—typically between 0.5% and 1%—or use the fully amortizing payment amount, even if no payments are currently required, to assess your debt obligations accurately. This approach ensures that deferred loans do not artificially lower your DTI and reflects your likely future payment responsibilities.

Conclusion

Calculating your debt-to-income ratio accurately is essential for understanding your mortgage eligibility and preparing for loan approval. By summing all recurring monthly debts and dividing by your gross monthly income, you obtain a percentage that lenders use to assess your financial capacity. Knowing the specific DTI limits for different loan types, such as conventional, FHA, and VA loans, helps borrowers set realistic expectations and plan accordingly.

While a high DTI can present challenges, it is not an automatic disqualifier. Lenders consider compensating factors including credit scores, reserves, and residual income. Understanding common misconceptions and using the proper calculation methods enables borrowers to improve their financial profile and enhance their chances of securing mortgage financing under favorable terms.