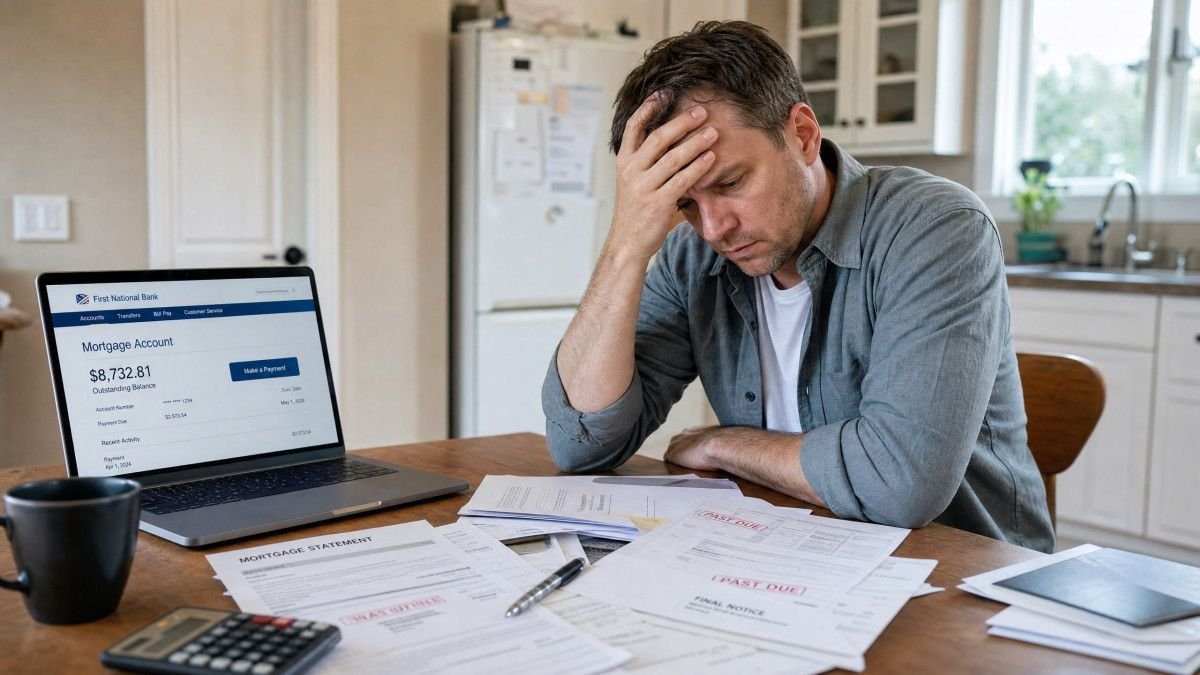

When homeowners find themselves unable to keep up with mortgage payments, it can quickly become a stressful and overwhelming experience, observes property management Fort Lauderdale FL. The risk of losing one’s home combined with the prospect of long-lasting credit damage makes it essential to act quickly. Facing financial hardship proactively allows homeowners the opportunity to explore solutions and prevent the situation from escalating into foreclosure. The sooner you address the problem, the more options you will have to protect your housing stability and financial future.

Financial difficulties that affect mortgage payments often arise unexpectedly and can stem from a wide range of life events. Job loss, reduction in work hours, unexpected medical bills, divorce, or even widespread economic downturns can all impact your ability to pay. Recognizing these challenges early and understanding that most lenders have programs designed to assist borrowers during tough times is critical. These programs are intended to provide relief and help homeowners regain their footing rather than lose their homes.

Knowing what steps to take when mortgage payments become unaffordable can empower homeowners to navigate this difficult period with greater confidence. It is essential to become familiar with available options such as temporary payment adjustments, loan modifications, refinancing opportunities, and other alternatives that may prevent foreclosure. Taking decisive action early can safeguard your credit, preserve your home, and provide the breathing room needed to stabilize your finances.

Immediate Steps to Take If You Can’t Afford Payments

The very first action to take upon recognizing that mortgage payments may become unaffordable is to contact your mortgage servicer immediately. Waiting until after a payment is missed can limit your options and increase fees or penalties. By communicating early, you demonstrate your willingness to resolve the issue and open the door to potential assistance. It is important to be honest and thorough when explaining the nature of your hardship, as this information guides the servicer in recommending appropriate programs.

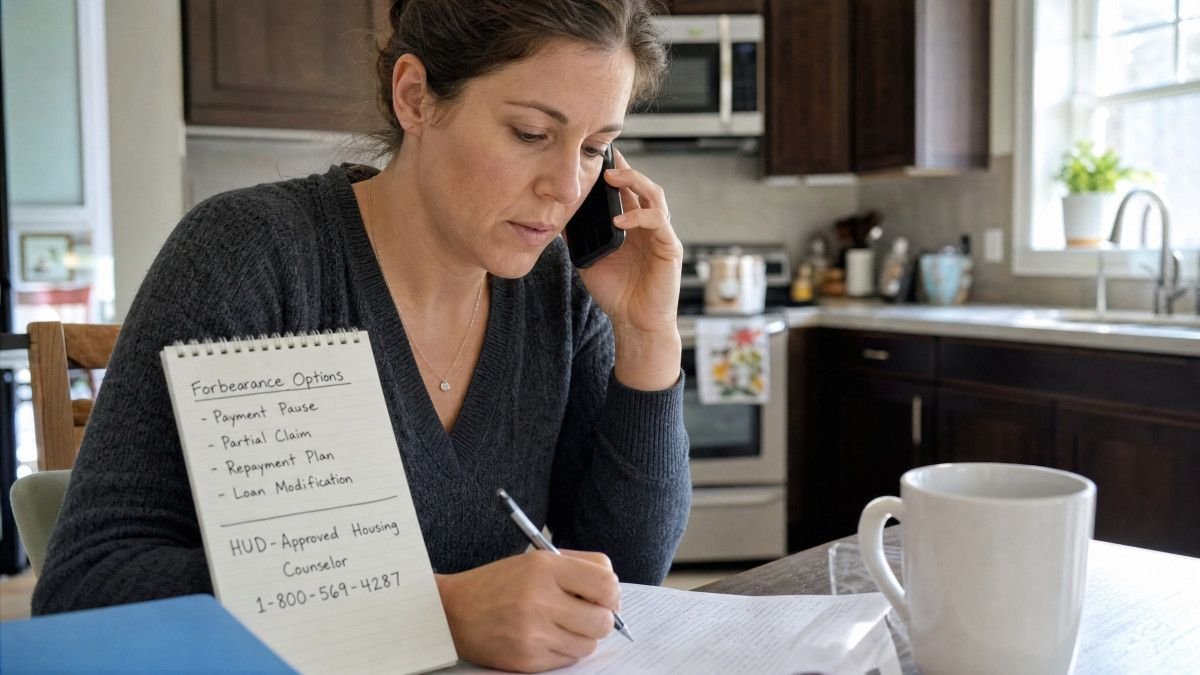

Beyond contacting the servicer, reaching out to a HUD-approved housing counselor can be an invaluable resource. These counselors are trained professionals who offer free, confidential advice tailored to your financial situation. They can help you understand complex lender communications, explain the pros and cons of various loss mitigation options, and even assist you in submitting paperwork. Many homeowners find that working with a counselor reduces stress and helps them make better-informed decisions during a difficult time.

Another immediate step is to gather all relevant financial documents including recent pay stubs, tax returns, bank statements, and information about monthly expenses. Having this documentation ready can speed up the review process when applying for assistance programs. Keeping a detailed record of all communications with your servicer and any housing counselors is also recommended, as it can help resolve disputes and ensure everyone is on the same page. Being organized and proactive increases the likelihood of a positive outcome.

Loss Mitigation Options Available to Homeowners

Loss mitigation options serve as tools to help homeowners manage mortgage payments during periods of financial distress. Forbearance is a popular choice, offering a temporary suspension or reduction in payments to provide short-term relief. During this time, borrowers can focus on stabilizing their income or addressing emergency expenses without falling further behind. While forbearance does not erase missed payments, it prevents immediate foreclosure and allows flexibility in repayment timing.

Repayment plans are another option designed to help borrowers gradually catch up on missed payments while maintaining regular monthly payments. These plans spread the overdue amounts over a predetermined period, reducing the shock of paying a lump sum all at once. Loan modifications, on the other hand, offer a more permanent solution by adjusting terms such as interest rates or loan duration to lower monthly payments sustainably. This option can be especially beneficial for those facing long-term financial changes rather than temporary hardship.

Refinancing may be possible if you qualify, which involves replacing your current mortgage with a new loan that has better terms. This can result in a lower interest rate or extended loan term, thereby decreasing monthly payments. However, refinancing requires good credit and sufficient equity in the home, which may not be feasible for all borrowers. In cases where staying in the home is not an option, alternatives like short sales or deeds in lieu of foreclosure provide ways to avoid the full foreclosure process. These options usually require lender approval and have varying impacts on credit and future homeownership.

Comparison of Loss Mitigation Options

Understanding how different loss mitigation options compare helps homeowners choose the best path forward based on their unique circumstances. Each option varies in terms of duration, payment structure, and credit consequences. For instance, while forbearance provides temporary relief, it requires repayment of missed amounts later, which could be a challenge if income does not improve. Loan modifications adjust the loan terms permanently, offering more stability but potentially affecting the total interest paid over the life of the loan.

Credit impact is another important consideration when evaluating these options. Some solutions may be reported as late payments or modifications, which can affect credit scores differently. For example, short sales and deeds in lieu of foreclosure typically have a more severe and lasting negative impact on credit, but they might be preferable to a full foreclosure in certain circumstances. Weighing the pros and cons of each option in light of your financial goals and future plans is essential for making an informed decision.

It is also critical to recognize that eligibility requirements and program availability can vary by lender and loan type. Some loss mitigation options may be available only for federally backed loans, while others might apply to private mortgages. Consulting with your mortgage servicer and housing counselor can clarify which options you qualify for and the specific steps required to apply. Being well-informed about these differences can prevent surprises and ensure you pursue the most effective solution.

Understanding Foreclosure Timeline and Credit Impact

Foreclosure is a legal process that lenders use to recover the balance of a loan from a borrower who has stopped making payments. The timeline for foreclosure generally begins after three to six missed payments, but the exact timing can vary significantly depending on state laws and the type of foreclosure process used. Judicial foreclosure states require court approval, which may extend the timeline, while non-judicial states allow lenders to proceed more quickly without court intervention. Understanding your state’s foreclosure process can help you anticipate deadlines and act accordingly.

The impact of foreclosure on credit is substantial and long-lasting. A foreclosure can cause a credit score to drop by 100 to 160 points, making it harder to qualify for future loans, credit cards, or even rental applications. The foreclosure remains on credit reports for up to seven years, signaling to lenders a higher risk. Missed payments leading up to foreclosure also negatively affect credit, often by 90 to 110 points. Alternatives such as short sales or deeds in lieu of foreclosure may still impact credit but sometimes less severely than a full foreclosure. Early intervention can help avoid reaching the foreclosure stage altogether.

In addition to credit damage, foreclosure can have other financial and emotional consequences. It may involve legal fees, deficiency judgments if the sale of the home does not cover the loan balance, and the stress of finding new housing. Awareness of these factors highlights why taking early steps to communicate with lenders and explore options is so important. Avoiding foreclosure preserves not only credit but also peace of mind and financial stability.

Additional Resources and Government Protections

Several government initiatives and resources are designed to assist homeowners experiencing difficulty with mortgage payments. The CARES Act, enacted in response to the COVID-19 pandemic, provided temporary forbearance rights for many federally backed loans, allowing borrowers to pause payments without penalty. While these protections were initially time-limited, similar programs may be extended or available through other government agencies. State and local housing finance agencies also sometimes offer assistance programs tailored to their communities.

Access to HUD-approved housing counselors is a vital resource for homeowners in distress. These counselors provide expert advice free of charge and can help you understand eligibility for various government and private programs. They also assist with paperwork and negotiations, making the process less daunting. Programs such as Making Home Affordable have provided loan modification and refinancing options for eligible borrowers, aiming to reduce monthly payments and prevent foreclosure. Staying informed about available assistance programs and taking advantage of them when needed can make a significant difference in managing mortgage challenges.

Additional nonprofit organizations and community groups may offer emergency financial assistance, temporary housing support, or legal aid related to housing issues. Exploring these resources early can provide much-needed support and broaden the options available. Proactive outreach to these organizations can help bridge gaps in income or expenses during times of hardship. Combining government protections with local resources often leads to more comprehensive solutions that meet individual needs more effectively.

Frequently Asked Questions

What is the first step if I can’t afford my mortgage?

The initial step is to contact your mortgage servicer as soon as you realize you may have trouble making your payments. Early communication allows you to explain your financial hardship and inquire about available assistance programs. Acting before missing any payments increases the likelihood of securing options such as forbearance or repayment plans. It also helps avoid late fees and negative credit reporting. Prompt outreach demonstrates your commitment to resolving the issue and can open the door to solutions tailored to your situation.

What is forbearance and how does it work?

Forbearance is an arrangement between a borrower and lender that temporarily reduces or suspends mortgage payments. This agreement typically lasts from three to twelve months and is intended to provide short-term relief during financial hardship. While payments are paused or lowered, the missed amounts are not forgiven; instead, they are either added to the end of the loan term or repaid through a repayment plan after the forbearance period ends. Forbearance helps avoid immediate foreclosure but requires a plan for catching up on missed payments.

What does loan modification mean?

Loan modification refers to a permanent change in the terms of your existing mortgage to make payments more affordable. This could involve lowering the interest rate, extending the length of the loan to reduce monthly payments, or, in some cases, reducing the principal balance. Loan modifications are intended for borrowers who anticipate long-term financial challenges rather than temporary setbacks. By adjusting the loan terms, a modification can help prevent foreclosure and provide stability by aligning payments with your current financial capacity.

How can a HUD housing counselor help me?

HUD-approved housing counselors offer free and confidential assistance to homeowners facing mortgage difficulties. They can explain your options, help you understand lender communications, and guide you through the application process for loss mitigation programs. Counselors also provide budgeting advice and support to improve your overall financial health. You can reach them by calling the national hotline at 1-800-569-4287. Their expertise can help reduce confusion, avoid mistakes, and increase your chances of successfully managing mortgage challenges.

When does foreclosure usually start?

Foreclosure proceedings typically begin after three to six consecutive missed mortgage payments, but the exact timing depends on state laws and whether the foreclosure is judicial or non-judicial. Judicial states require the lender to file a lawsuit in court, which can lengthen the timeline, while non-judicial states allow lenders to foreclose without court involvement, sometimes making the process faster. Understanding your state’s specific process and timeline is crucial so you can take timely action to avoid losing your home.

Can refinancing help if I can’t afford my mortgage?

Refinancing can be a helpful option for homeowners who qualify, as it replaces the existing mortgage with a new loan that often has lower interest rates or longer terms, resulting in reduced monthly payments. However, qualifying for refinancing generally requires good credit and sufficient home equity. If your financial situation has deteriorated significantly, refinancing might not be available. In such cases, other loss mitigation options like loan modifications or forbearance may be more appropriate. Consulting with your lender or counselor can clarify which solutions fit your circumstances best.

Conclusion

Facing the inability to afford mortgage payments is undoubtedly a stressful challenge, but taking swift and informed action can make a meaningful difference. Opening lines of communication with your mortgage servicer before missing payments allows access to various loss mitigation programs designed to help homeowners manage their financial difficulties. Utilizing free resources such as HUD-approved housing counselors can provide valuable guidance and support throughout the process, helping to clarify options and reduce uncertainty.

Understanding the foreclosure process, its timeline, and the impact on credit empowers homeowners to make strategic decisions that protect their financial wellbeing. Although foreclosure is a serious and impactful event, exploring alternatives like forbearance, loan modifications, or refinancing can help preserve homeownership or minimize damage. Early engagement, careful planning, and using available assistance are key factors in achieving the best possible outcome during financial hardship.