When prospective homebuyers begin exploring mortgage options, they often encounter a variety of loan types, among which FHA loans and conventional loans are the most common. Each has its own set of qualifications, benefits, and limitations that can significantly affect affordability and eligibility. FHA loans are backed by the government through the Federal Housing Administration, which helps reduce risk for lenders and allows borrowers with less-than-perfect credit or smaller down payments to qualify more easily. Conventional loans, by contrast, are offered by private lenders and are not insured by the government, often requiring higher credit standards but offering more flexibility in some areas, points out Apex Property Management, a trusted Boise property management.

The decision between an FHA loan and a conventional loan can influence the overall cost of homeownership, including the size of the down payment, monthly mortgage payments, and mortgage insurance requirements. FHA loans generally require lower credit scores and down payments, making them attractive to first-time buyers and those with limited savings. Conventional loans tend to favor borrowers with stronger credit and larger down payments, offering the potential to eliminate mortgage insurance once enough equity is built. Understanding these distinctions is essential to selecting the loan that best matches a borrower’s financial situation and homeownership goals.

Beyond credit and down payment considerations, other factors such as debt-to-income ratios, loan limits, property eligibility, and mortgage insurance premium structures also differ between FHA and conventional loans. These elements can impact a borrower’s ability to qualify and the total cost over time. A thorough understanding of how each loan type functions enables buyers to make informed choices that optimize their long-term financial outcomes and align with their plans for homeownership.

FHA Loans: Key Facts and Requirements

FHA loans are mortgages insured by the Federal Housing Administration, a division of HUD, designed to increase homeownership accessibility, especially for first-time buyers and those with less-than-ideal credit. Established in 1934, FHA loans allow for lower down payments and more flexible credit standards compared to conventional loans.

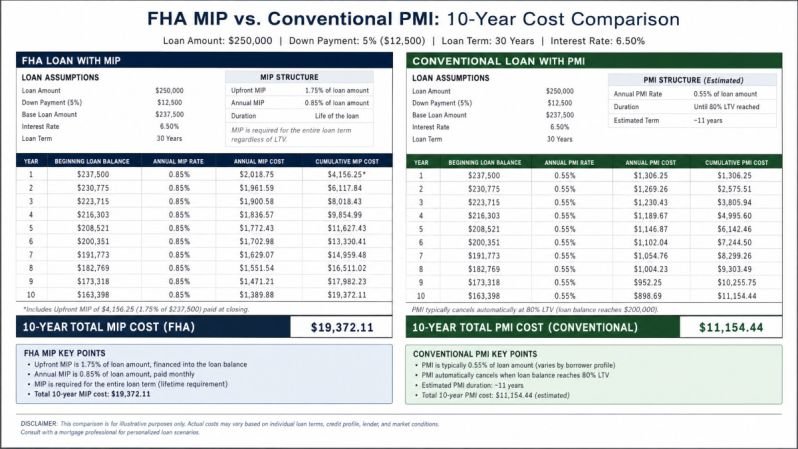

Borrowers with a FICO score of 580 or higher can qualify for as little as a 3.5% down payment, while scores between 500 and 579 typically require 10%. FHA loans also allow debt-to-income ratios up to 43%, and sometimes higher with compensating factors. However, FHA loans require an upfront mortgage insurance premium of 1.75% of the loan amount plus an annual mortgage insurance premium ranging from 0.15% to 0.75%, which often lasts for the loan’s life unless the down payment is 10% or more.

Another important aspect of FHA loans is the allowance for alternative credit documentation, which helps borrowers without a traditional credit history qualify. This can include records of timely rent, utility, phone, and insurance payments, making FHA loans accessible to those who may not have established credit through conventional means. Additionally, FHA loan limits vary by county, reflecting local housing market costs, with 2026 limits ranging from $541,287 in low-cost areas to $1,249,125 in high-cost regions for single-family homes. These limits ensure FHA loans remain targeted toward moderate-income borrowers without exceeding typical housing values in the area.

FHA loans also cover a range of property types beyond single-family homes, including multi-family properties up to four units, provided the borrower occupies one unit. Eligible properties include HUD-approved condominiums and manufactured homes meeting FHA standards. The requirement that the property be the borrower’s primary residence ensures the program supports owner-occupants rather than investors, aligning with the FHA’s mission to promote stable homeownership.

Conventional Loans: Key Facts and Requirements

Conventional loans are not government-insured but follow guidelines from entities like Fannie Mae and Freddie Mac. Typically, a minimum credit score of 620 is required, though higher scores yield better interest rates and lower mortgage insurance costs. Down payments can be as low as 3%, but 20% is recommended to avoid private mortgage insurance (PMI).

PMI on conventional loans, which ranges from 0.3% to 1.15% annually, is cancelable once a borrower attains 20% equity in the home. Conventional loans generally prefer debt-to-income ratios of 45% or less but may allow up to 50% in some cases. Loan limits are set by the FHFA; in 2025, the conforming loan limit was $806,500 for most areas. Conventional loans also offer more flexibility in property types and occupancy, including investment properties and second homes.

Conventional loans often appeal to borrowers with stronger credit profiles and larger down payment capabilities, as they can access more competitive interest rates and more favorable terms. These loans accommodate a broader spectrum of property uses, including primary residences, second homes, and investment properties, providing flexibility not available with FHA loans. Additionally, conventional loans allow for a variety of property types, including single-family homes, multi-unit properties up to four units, condominiums, and planned unit developments, depending on lender criteria.

While conventional loans require private mortgage insurance if the down payment is less than 20%, this insurance can be removed once the borrower reaches 20% equity, often reducing monthly payments significantly. This feature can make conventional loans more cost-effective over time for borrowers who plan to build equity quickly or refinance. Moreover, conventional loans typically enforce stricter underwriting standards, including more rigorous credit score requirements and documentation, which can result in faster loan processing for qualified borrowers.

Comparison of FHA vs. Conventional Loans

This table summarizes critical distinctions between FHA and conventional loans to clarify their differences in credit requirements, mortgage insurance, and loan limits.

| Feature | FHA Loan | Conventional Loan |

|---|---|---|

| Government Backing | Yes (insured by FHA) | No (private lenders, GSE guidelines) |

| Minimum Credit Score | 500 (with 10% down) / 580 (with 3.5% down) | 620 |

| Minimum Down Payment | 3.5% | 3% |

| Mortgage Insurance | Upfront MIP 1.75% + Annual MIP 0.15%-0.75% | PMI 0.3%-1.15% annually if <20% down |

| MIP/PMI Duration | Annual MIP for life (or 11 years if ≥10% down) | PMI cancellable at 20% equity |

| Debt-to-Income Ratio Flexibility | Up to 43%, sometimes higher with compensating factors | Typically 45% or lower, up to 50% in some cases |

| Loan Limits | Set by HUD, varies by county (e.g., $541,287 – $1,249,125 in 2026 for 1-unit) | Set by FHFA, conforming limits (e.g., $806,500 in 2025 for 1-unit) |

| Property Types | Primary residence only; 1-4 units, HUD-approved condos, manufactured homes | Primary, secondary, investment properties; 1-4 units |

| Occupancy | Primary residence required | Primary, secondary, investment |

Common Misconceptions About FHA and Conventional Loans

Several myths about FHA and conventional loans can mislead prospective borrowers. One common misconception is that FHA loans are only for first-time buyers; however, any qualified borrower can obtain an FHA loan regardless of prior homeownership. Another myth suggests FHA loans are only for low-income buyers, but there are no income limits associated with FHA programs.

It is also falsely believed that FHA loans have tougher appraisal requirements than conventional loans. Both loan types require appraisals that ensure the property is safe and sound. Additionally, many believe a 20% down payment is mandatory for conventional loans; in reality, some conventional programs allow down payments as low as 3%. Lastly, mortgage insurance on FHA loans does not always last forever—it can end after 11 years if the down payment is at least 10% or by refinancing into a conventional loan once 20% equity is reached.

Another frequent misunderstanding involves the upfront mortgage insurance premium on FHA loans. Some borrowers assume it is an extra out-of-pocket cost, but it is commonly financed into the loan amount, increasing the loan balance rather than requiring immediate payment. Additionally, some believe conventional loans are universally better due to the ability to cancel PMI; however, for borrowers with lower credit scores or limited savings, FHA loans may provide more affordable monthly payments despite the mortgage insurance premiums lasting longer.

There is also confusion regarding occupancy requirements. FHA loans strictly require the borrower to occupy the property as their primary residence, limiting their use for investment or second homes, whereas conventional loans allow financing for secondary residences and investment properties. This distinction is critical for borrowers considering purchasing homes for purposes other than primary occupancy.

Frequently Asked Questions

What is the primary difference between an FHA loan and a conventional loan?

The primary difference is that FHA loans are insured by the Federal Housing Administration, which enables lenders to offer lenient terms like lower credit score and down payment requirements. Conventional loans are not government-backed and follow stricter guidelines set by private lenders and government-sponsored enterprises such as Fannie Mae and Freddie Mac. Conventional loans require higher credit scores but offer cancellable private mortgage insurance once 20% equity is reached.

Can I get an FHA loan if I’m not a first-time homebuyer?

Yes, FHA loans are available to any borrower who meets the eligibility criteria, regardless of whether they have owned a home before. The key requirement is that the property purchased must be the borrower’s primary residence. FHA loans are popular among first-time buyers but are not restricted to them.

How much down payment do I need for each loan type?

For FHA loans, the down payment can be as low as 3.5% if the borrower’s FICO score is 580 or higher. For scores between 500 and 579, a 10% down payment is usually required. Conventional loans can require down payments as low as 3%, especially with programs like Fannie Mae’s HomeReady®, but a 20% down payment is typically recommended to avoid private mortgage insurance.

What are the mortgage insurance implications for FHA vs. conventional loans?

FHA loans require an upfront mortgage insurance premium of 1.75% of the loan amount, typically financed into the mortgage, plus an annual mortgage insurance premium ranging from 0.15% to 0.75%. This annual premium generally lasts for the life of the loan if the down payment is less than 10%. Conventional loans require private mortgage insurance if the down payment is under 20%, but this PMI can be canceled once the borrower attains 20% equity.

Which loan type is better for someone with a lower credit score?

FHA loans are typically better suited for borrowers with lower credit scores because they accept FICO scores as low as 500 with a 10% down payment or 580 with a 3.5% down payment. Conventional loans generally require a minimum FICO score of 620, making FHA loans more accessible to those with credit challenges.

Can I use an FHA loan for investment properties or second homes?

No, FHA loans require that the property be the borrower’s primary residence. They can be used for single-family homes, multi-unit properties up to four units (if the borrower occupies one unit), HUD-approved condominiums, and manufactured homes. Investment properties and second homes are not eligible for FHA financing. Conventional loans, however, do allow financing for investment properties and second homes, offering more flexibility in property usage.

How do debt-to-income ratios affect FHA and conventional loan approvals?

FHA loans typically allow for higher debt-to-income (DTI) ratios, often up to 43%, and sometimes even exceeding 50% if the borrower has compensating factors like strong credit or significant cash reserves. Conventional loans generally prefer DTIs of 45% or lower, but some lenders may allow up to 50%. Higher DTI ratios can make FHA loans more accessible for borrowers with existing debts.

Conclusion

FHA loans and conventional loans each cater to different borrower profiles and financial situations. FHA loans provide more lenient credit score requirements and lower down payment options, making them accessible to a wider range of borrowers, particularly those with limited savings or credit challenges. However, they require upfront and ongoing mortgage insurance premiums, which can increase the overall cost of the loan, especially if the down payment is less than 10%.

Conventional loans offer more flexibility in property use and the potential to cancel mortgage insurance once sufficient equity is built. They typically require higher credit scores and larger down payments but may result in lower long-term costs for well-qualified borrowers. Evaluating credit standing, savings for a down payment, and intended property use will help borrowers select the mortgage option that best aligns with their financial goals and homeownership plans.