Obtaining the best mortgage rate involves understanding various factors that influence loan pricing and taking proactive steps to optimize your profile before applying, notes TrueDoor PM Temecula solutions. Mortgage interest rates fluctuate depending on lender policies, market conditions, borrower creditworthiness, and loan characteristics. Even a small difference in rates can translate into thousands of dollars in savings over the life of a loan. Recognizing the nuances behind these elements plays a crucial role in making informed borrowing decisions.

Before applying for a mortgage, it is essential to prepare your financial health comprehensively. This preparation goes beyond just knowing your credit score; it includes managing existing debts, saving for a substantial down payment, and understanding different loan products that suit your unique situation. Taking time to educate yourself about these components can lead to better negotiation power with lenders and improved loan terms.

Additionally, timing and market awareness can influence the mortgage rate you receive. Interest rates are affected by broader economic indicators, including inflation trends, Federal Reserve policies, and bond market movements. Being aware of these patterns allows you to lock in rates at favorable times. Combining strategic financial preparation with market insight equips homebuyers to secure mortgage rates that align with their long-term financial goals.

Factors Influencing Mortgage Rates

Mortgage rates are determined by a combination of borrower-specific factors and broader market conditions. The borrower’s credit score is one of the most critical determinants, with higher scores typically qualifying for lower rates. A credit score of 760 or above is generally considered excellent and can significantly reduce the interest rate offered. Loan-to-value ratio (LTV), which reflects the size of the down payment relative to the home’s value, also plays a substantial role, with larger down payments leading to better rates.

Other considerations include the loan type, such as conventional, FHA, or VA loans, and the loan term, where shorter terms usually feature lower rates. The property’s intended use—primary residence, secondary home, or investment property—affects pricing as well. Additionally, the borrower’s debt-to-income ratio (DTI) impacts the lender’s risk assessment. Market conditions, particularly the 10-year Treasury yield, influence overall interest rate trends, affecting all mortgage pricing.

Economic factors such as inflation expectations and the state of the housing market also contribute to mortgage rate fluctuations. When inflation is rising, lenders often increase rates to maintain returns above inflation. Similarly, strong housing demand can push rates higher as lenders adjust pricing to balance risk and demand. Conversely, during economic downturns or periods of market uncertainty, mortgage rates tend to decrease as lenders seek to stimulate borrowing.

Geographical differences can influence mortgage rates as well. Certain regions may have varying rates due to local economic conditions, property values, and lender competition. Borrowers should be aware that rates offered in metropolitan areas may differ from those in rural locations, reflecting localized risk profiles and market dynamics.

Steps to Secure the Best Mortgage Rate

Improving your credit score is the first step toward obtaining a favorable mortgage rate. Borrowers should aim to raise their credit score to at least 760 by paying bills on time, reducing outstanding debt, and correcting errors on credit reports. A higher credit score reduces perceived risk for lenders and results in lower interest charges. Saving a larger down payment, ideally 20 percent or more, can eliminate private mortgage insurance and improve loan pricing.

Lowering your debt-to-income ratio by paying off debts before applying helps lenders view you as a lower-risk borrower. Shopping multiple lenders by obtaining at least three to five Loan Estimates on the same day allows for accurate comparisons based on identical market conditions. Comparing the APR rather than just the nominal interest rate provides a clearer picture of overall loan cost. Considering mortgage points to buy down your rate and choosing the correct loan type for your situation further optimize your rate.

In addition, maintaining stable employment and income history enhances your borrowing profile. Lenders favor applicants with consistent income sources, as this reduces the risk of default. Preparing all necessary documentation, such as tax returns and pay stubs, also streamlines the application process and can encourage lenders to offer better terms.

Timing your mortgage application around favorable market conditions can also improve your chances of securing a lower rate. Monitoring economic indicators and consulting with financial advisors can provide insights into when rates may be at their lowest. Being ready to lock in a rate quickly once you find a competitive offer can prevent potential increases during the approval process.

Mortgage Points, Rate Locks, and Loan Comparison

Mortgage points enable borrowers to pay upfront fees to reduce their interest rate. One point equals one percent of the loan amount and typically lowers the rate by approximately 0.25 percent. Calculating the break-even point—where the upfront cost equals the monthly savings—is essential to determine if paying points is financially beneficial. Borrowers who plan to stay in their homes beyond this point can save money over the long term.

Rate locks protect borrowers from rising rates during the loan processing period, usually lasting 30 to 60 days. Some lenders offer float-down options, allowing borrowers to benefit from rate decreases after locking. Choosing the appropriate loan type, such as VA or USDA loans for eligible borrowers, can provide some of the lowest mortgage rates available due to government backing or incentives.

Besides traditional mortgage points, some lenders also offer “rebate points,” which can lower closing costs by increasing the interest rate slightly. Understanding these options allows borrowers to tailor their loan structure according to their financial priorities, whether that means reducing upfront expenses or lowering monthly payments.

Evaluating loan comparison involves more than just rates and points. It is important to consider loan features such as prepayment penalties, flexibility of payment schedules, and the lender’s reputation for customer service and transparency. A well-rounded comparison ensures that the chosen mortgage aligns with both financial goals and personal comfort with the lender.

| Loan Type | Typical Interest Rate | Down Payment Requirement | Mortgage Insurance | Eligibility |

|---|---|---|---|---|

| Conventional | Varies; generally moderate | 5%–20% (20% to avoid PMI) | PMI required if down payment < 20% | Most borrowers |

| FHA | Often higher than conventional | 3.5% | Upfront and annual mortgage insurance premiums | Borrowers with lower credit scores |

| VA | Lowest among eligible borrowers | 0% | No PMI, but funding fee applies | Eligible veterans and military |

| USDA | Competitive, low rates | 0% | Mortgage insurance required | Rural homebuyers meeting income limits |

Shopping Multiple Lenders and Comparing APR

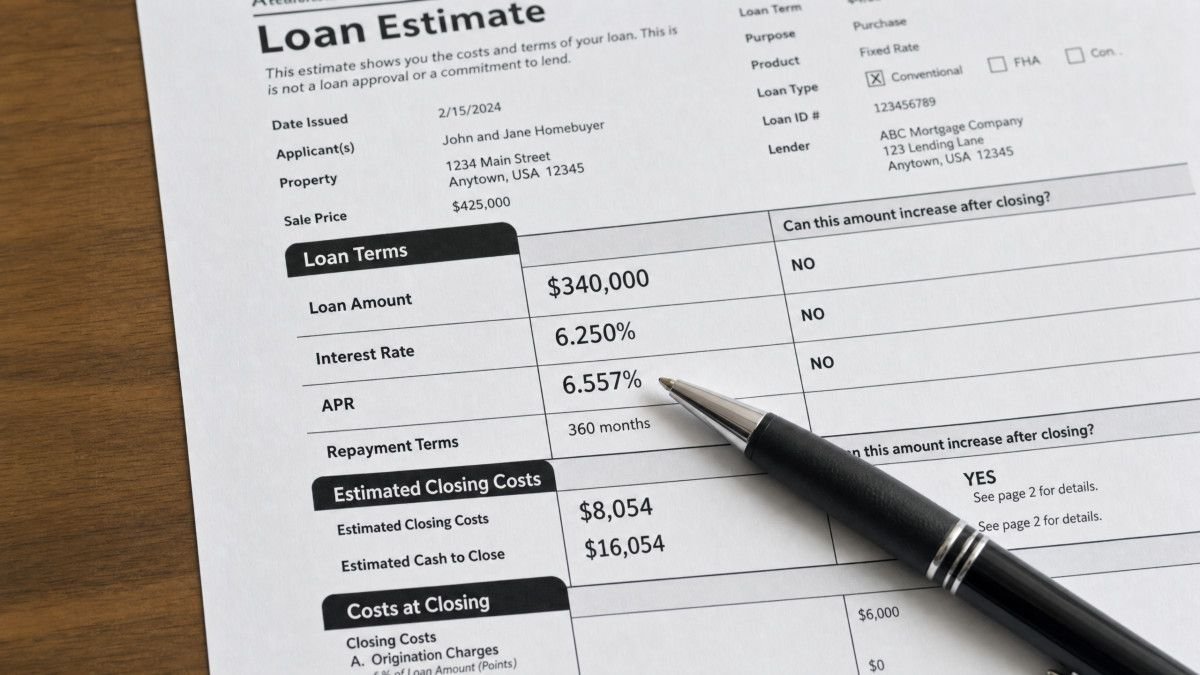

Shopping with multiple lenders is the most effective way to secure the lowest mortgage rate possible. Borrowers should request Loan Estimates from at least three to five lenders on the same day to ensure rate quotes reflect identical market conditions. This practice prevents misleading comparisons due to fluctuating interest rates over time. Loan Estimates provide detailed information on interest rates, fees, and closing costs, enabling borrowers to make informed decisions.

Comparing the Annual Percentage Rate (APR) rather than just the nominal interest rate gives a more comprehensive measure of the loan’s true cost. The APR includes interest plus lender fees and certain closing costs, reflecting the total yearly cost of the loan. Evaluating APR helps borrowers avoid loans with deceptively low rates but high fees, ultimately improving their ability to select the most cost-effective mortgage option.

In addition to APR, understanding the total cost of homeownership involves evaluating other loan features such as escrow requirements, potential rate adjustments on adjustable-rate mortgages, and any lender-specific incentives or discounts. A thorough review of all loan terms alongside APR comparisons ensures the selection of a mortgage that best fits the borrower’s financial situation.

Building relationships with local lenders or mortgage brokers can also provide access to specialized loan products or discounts that may not be widely advertised. These personalized options can sometimes result in better rates or more flexible terms, which can be beneficial when combined with the broader shopping strategy.

FAQ About Getting the Best Mortgage Rate

How many lenders should I shop to get the best mortgage rate?

It is recommended to obtain Loan Estimates from at least three to five different lenders. This range provides a broad sample of available rates and fees, allowing for a better comparison. Shopping multiple lenders on the same day ensures that rate quotes are based on current market conditions, preventing outdated or inconsistent offers from skewing your decision. By comparing several offers, you increase your chances of finding competitive terms tailored to your profile.

How does my credit score impact the mortgage rate I can get?

Your credit score is one of the most important factors lenders use to set your mortgage rate. Scores above 760 typically qualify for the best rates because they indicate lower risk. Lower scores often lead to higher rates and increased costs. Improving your credit before applying can save thousands in interest over the life of the loan. Lenders also consider credit history details such as payment timeliness, credit utilization, and length of credit history when determining your rate.

What is the difference between the interest rate and APR?

The interest rate is the nominal cost of borrowing expressed as a percentage, while the APR includes the interest rate plus lender fees and certain closing costs spread over the loan term. APR provides a more comprehensive view of the loan’s total cost, making it a better metric for comparing offers from different lenders. While the interest rate affects your monthly payment, the APR reflects the overall expense you will pay during the loan’s life.

What are mortgage points and are they worth paying for?

Mortgage points are upfront fees paid to lower your interest rate; one point equals one percent of the loan amount and usually reduces the rate by about 0.25 percent. Whether points are worth it depends on how long you plan to stay in the home. Paying points can save money if you remain in the property past the break-even point when monthly savings exceed the initial cost. Evaluating your expected time in the home alongside your financial situation is crucial before deciding to purchase points.

What is a rate lock and how long does it last?

A rate lock is an agreement with your lender to secure a specific mortgage interest rate for a set period, typically 30 to 60 days. This protects you from rising rates during the loan closing process. Some lenders offer float-down options that allow you to take advantage of lower rates if market rates drop after the lock. It’s important to understand the terms and fees associated with rate locks, as extended locks or float-downs may involve additional costs.

Conclusion

Securing the best mortgage rate requires a clear understanding of how lender criteria, borrower financial profiles, and market conditions intersect to determine pricing. Improving credit scores, increasing down payments, lowering debt levels, and choosing the right loan type contribute significantly to obtaining favorable rates. Collecting multiple Loan Estimates simultaneously allows borrowers to compare offers accurately and select the most cost-effective option. These steps form the foundation for a successful home financing experience.

Evaluating the full cost of loans through the APR metric, considering mortgage points, and making strategic decisions about locking rates further enhance savings potential. By applying these strategies and maintaining informed decision-making throughout the mortgage application process, borrowers can minimize interest expenses and ensure more affordable home financing. Careful planning and thorough research empower homebuyers to navigate the mortgage landscape with confidence and secure terms aligned with their financial goals.