Private mortgage insurance (PMI) is an additional cost required by lenders on conventional home loans when the borrower’s down payment is less than 20% of the purchase price, points out TRI Property Pros. It serves to protect the lender from potential losses if the borrower defaults on the loan. While PMI allows buyers to finance homes with smaller down payments, it is a significant recurring expense that can substantially increase the total cost of homeownership.

Typically, PMI costs range from 0.5% to 1.5% of the original loan amount annually, paid in monthly installments. For example, on a $300,000 loan, this translates to $1,500 to $4,500 per year or roughly $125 to $375 per month. These payments continue until the borrower accumulates at least 20% equity in the property, at which point the borrower can request cancellation of PMI under federal rules.

Understanding the true cost of PMI involves not only the monthly premiums but also the timing and conditions of cancellation, available alternatives, and the potential opportunity cost of tying up more capital in a larger down payment. Evaluating these factors is essential to making informed decisions when financing a home purchase.

In addition to the direct financial implications, PMI can influence a borrower’s long-term wealth accumulation and cash flow management. The recurring monthly expense may limit the ability to save or invest elsewhere, potentially affecting overall financial goals. Moreover, the structure of PMI payments and their cancellation can vary, so being aware of these nuances helps in forecasting homeownership costs more accurately. Considering PMI as one part of the broader mortgage strategy ensures buyers remain prepared for the full financial commitment involved in purchasing a home with a smaller down payment.

Many prospective homebuyers face the challenge of balancing immediate affordability with long-term financial impact. PMI provides a pathway to homeownership without the need for a substantial upfront investment, but its cost can accumulate significantly over time. Understanding how PMI fits into the overall mortgage picture, including its interaction with interest rates, loan terms, and market conditions, is key to making well-rounded decisions. Planning ahead for PMI expenses and exploring ways to mitigate or avoid them can lead to better financial outcomes and smoother homeownership experiences.

What Is PMI and Why Is It Required?

Private mortgage insurance (PMI) is insurance that protects the lender, not the borrower, against losses if the borrower defaults on a conventional mortgage. It is typically required when the borrower makes a down payment of less than 20% of the home’s purchase price. Since lower down payments represent higher risk to lenders, PMI serves as a safeguard to reduce that risk and allow borrowers to access financing that might otherwise be unavailable.

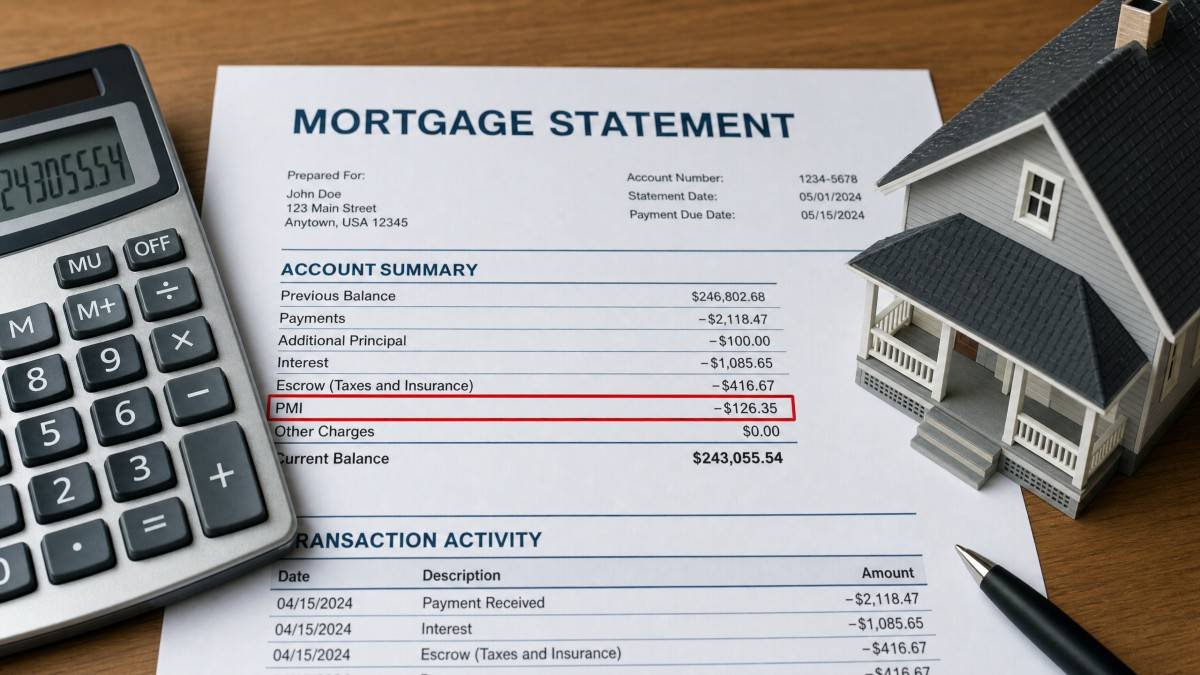

PMI premiums are paid monthly as part of the mortgage payment and are calculated as a percentage of the original loan amount. The requirement for PMI is a standard industry practice for conventional loans with lower equity and is distinct from government-backed mortgage insurance programs, such as FHA mortgage insurance premiums (MIP), which have different rules and costs.

By requiring PMI, lenders can offer loans to a broader range of borrowers, including those who may not have the savings to provide a substantial down payment. This insurance mitigates potential losses for lenders by covering a portion of the unpaid loan balance in the event of foreclosure. From the borrower’s perspective, PMI opens the door to homeownership sooner but comes with added monthly costs that should be carefully weighed against the benefits of entering the housing market earlier.

Furthermore, PMI requirements reflect the balance of risk and reward in mortgage lending. Borrowers with higher down payments inherently carry lower risk, so PMI is not necessary in those cases. However, for borrowers with less upfront equity, PMI protects lenders and encourages lending activity, which can have a positive impact on overall housing market liquidity. Understanding this dynamic helps borrowers appreciate why PMI exists and how it fits into the broader lending ecosystem.

How PMI Costs Are Calculated

PMI typically costs between 0.5% and 1.5% of the original loan amount annually. The exact rate depends on factors such as the borrower’s credit score, loan-to-value ratio (LTV), and the loan type. For example, on a $300,000 loan, an annual PMI cost rate of 1% results in $3,000 per year or $250 per month. Lower credit scores and higher LTV ratios generally produce higher PMI rates within the standard range.

The monthly PMI premium is added to the mortgage payment and continues until the borrower reaches the required equity level to cancel PMI. Over the course of several years, especially with smaller down payments, total PMI payments can accumulate to thousands of dollars, making it a substantial hidden cost that buyers should factor into their budgets and loan comparisons.

Additional variables can influence PMI rates, including the borrower’s debt-to-income ratio, loan term length, and the insurer’s underwriting guidelines. For instance, borrowers with excellent credit profiles and modest LTV ratios may qualify for lower PMI rates, reducing the overall cost. Conversely, riskier borrower profiles often lead to higher premiums.

Some lenders may offer different PMI premium structures, including single-premium options where the cost is paid upfront rather than monthly, or split-premium arrangements combining upfront and monthly payments. These variations affect both the lender’s risk exposure and the borrower’s cash flow, so understanding the calculation and structure of PMI costs is critical for evaluating mortgage offers comprehensively.

PMI Cancellation Rules and Timelines

The Homeowners Protection Act of 1998 establishes rules governing the cancellation of PMI on conventional loans. Borrowers can request PMI cancellation once their loan-to-value ratio reaches 80% based on the original purchase price or appraised value at loan initiation. Lenders are required to automatically cancel PMI when the LTV reaches 78%, assuming payments are current.

Additionally, lenders must cancel PMI at the midpoint of the loan term, even if the LTV has not reached 78%, provided the borrower is current on payments. Borrowers seeking earlier cancellation can request an appraisal to demonstrate that the property’s value has increased sufficiently to reduce the LTV below 80%. Understanding these rules helps homeowners plan when to expect relief from PMI payments.

It is important for borrowers to actively monitor their home equity and communicate with their lenders regarding PMI cancellation. While automatic cancellation at 78% LTV is mandated, many borrowers may benefit from proactively requesting an appraisal once they believe they have reached 20% equity, especially if property values have appreciated. Timely cancellation can result in significant savings by eliminating unnecessary PMI payments.

In some cases, paying down the principal aggressively or refinancing can accelerate the removal of PMI. However, refinancing to remove PMI should be evaluated carefully considering closing costs, current interest rates, and the borrower’s financial situation. Additionally, certain loans may have specific requirements or restrictions on PMI removal, so consulting the loan agreement and lender policies is advisable to avoid surprises.

Alternatives to PMI and Comparison of Options

Several alternatives to paying PMI exist for borrowers who want to avoid monthly PMI premiums. The most straightforward is making a 20% down payment, which eliminates the need for PMI entirely. Other options include piggyback loans, where a second mortgage covers part of the down payment to keep the first mortgage at 80% LTV; lender-paid PMI, where the lender covers PMI in exchange for a higher interest rate; and government-backed loans such as VA or USDA loans that do not require PMI but may have other fees or eligibility criteria.

Each alternative has distinct cost implications, upfront requirements, and eligibility considerations. Comparing these options based on total cost over time, cash flow impact, and borrower qualifications is essential to choosing the most financially advantageous approach.

Piggyback loans, often structured as an 80/10/10 arrangement, can be beneficial for those with limited cash on hand but may result in higher overall interest expenses due to the second mortgage’s typically higher rates. Lender-paid PMI can simplify monthly payments but often leads to increased interest costs over the life of the loan, which may outweigh the savings. Government-backed loans provide attractive alternatives but are only available to qualifying borrowers and may include other fees or restrictions.

Evaluating these alternatives requires a thorough analysis of both upfront and long-term costs, as well as consideration of personal financial situations and goals. Consulting with mortgage professionals and running detailed cost comparisons help borrowers make decisions aligned with their financial priorities and homeownership plans.

| Option | Description | Typical Costs | Pros | Cons |

|---|---|---|---|---|

| Standard PMI | Monthly premiums on conventional loans with less than 20% down. | 0.5%–1.5% of loan annually, paid monthly. | Allows low down payment; cancelable at 80% LTV. | Ongoing monthly cost until cancellation; adds to monthly payment. |

| 20% Down Payment | No PMI required with at least 20% down. | Higher upfront cash needed; no PMI payments. | No PMI cost or payments; lower loan amount. | Requires substantial upfront cash; may delay purchase. |

| Piggyback Loan (80/10/10) | Second mortgage covers part of down payment to avoid PMI. | Two loan payments; usually higher rates on second loan. | Avoids PMI; lower first mortgage LTV. | More complex financing; higher overall interest costs. |

| Lender-Paid PMI (LPMI) | Lender pays PMI; borrower accepts higher interest rate. | Higher interest rate over loan life; no monthly PMI line item. | No monthly PMI payments; simpler payment structure. | Higher total interest costs; PMI not cancelable separately. |

| VA or USDA Loans | Government-backed loans with no PMI but other fees. | Funding or guarantee fees apply; no monthly PMI. | No PMI required; favorable terms for eligible borrowers. | Eligibility limited; may have upfront fees. |

Calculating the True Cost of PMI

The true cost of PMI extends beyond the monthly premiums to include opportunity costs and cancellation timing. Borrowers must consider the total PMI payments made until cancellation, which can range from several thousand to over ten thousand dollars depending on the loan amount, down payment, and property appreciation. For example, a borrower with a 5% down payment on a $300,000 loan might pay $5,000 to $15,000 in PMI before reaching 20% equity.

Additionally, the opportunity cost of using funds for a larger down payment instead of investing elsewhere should be factored. While avoiding PMI requires more upfront cash, investing that capital might yield returns that offset or exceed the PMI expense. Analyzing these trade-offs helps determine whether paying PMI or increasing the down payment is more financially beneficial over the long term.

Calculating the true cost also involves considering how property value fluctuations affect the timeline for PMI cancellation. Appreciation can accelerate equity buildup, reducing PMI duration and total payments, while depreciation may extend PMI obligations. Borrowers should account for local market trends and home price volatility when estimating PMI costs.

Moreover, tax implications related to PMI payments can influence the net cost. Although PMI premiums were tax deductible for many taxpayers in recent years, changes in tax law affect this benefit. Borrowers should consult tax professionals to understand potential deductions or credits, which can partially offset PMI expenses and affect overall affordability.

Frequently Asked Questions About Private Mortgage Insurance (PMI)

How much does PMI typically cost?

PMI usually costs between 0.5% and 1.5% of the original loan amount annually. This is paid monthly and varies based on credit score, loan-to-value ratio, and loan specifics. For example, on a $300,000 loan, PMI could cost between $125 and $375 per month. Factors such as the borrower’s financial profile and the insurer’s pricing models can cause rates to fluctuate within this range.

When can PMI be canceled?

Borrowers can request PMI cancellation once their loan-to-value ratio reaches 80% of the original purchase price. Lenders must automatically cancel it at 78% LTV if payments are current. PMI must also be canceled at the loan’s midpoint term under federal law. To initiate cancellation, borrowers often need to submit a written request and may have to pay for an appraisal to confirm property value and equity.

What is the difference between FHA MIP and PMI?

FHA mortgage insurance premium (MIP) is similar to PMI but more difficult to cancel. For FHA loans with less than 10% down originated after June 2013, MIP typically lasts for the life of the loan, whereas PMI can be canceled once sufficient equity is reached. Additionally, FHA MIP includes both upfront and annual premiums, which generally make FHA loans more expensive over time compared to conventional loans with PMI.

How can I avoid paying PMI?

PMI can be avoided by making a 20% down payment, using a piggyback loan arrangement, choosing lender-paid PMI which increases the interest rate instead of monthly payments, or qualifying for a VA or USDA loan, which do not require PMI. Each option carries its own financial trade-offs and eligibility requirements, so borrowers should evaluate which approach aligns best with their financial situation and homebuying goals.

What is lender-paid PMI (LPMI)?

Lender-paid PMI means the lender covers PMI premiums in exchange for charging a higher interest rate on the loan. This removes the monthly PMI payment but increases the overall interest costs over the loan term, and PMI cannot be canceled separately. While this option simplifies monthly payments, borrowers should carefully compare the long-term cost impact against traditional PMI arrangements before choosing LPMI.

Conclusion

Private mortgage insurance is a necessary and often costly component of financing a home with less than 20% down on a conventional loan. The monthly PMI premiums can add significant expense over several years until cancellation is possible. Understanding the rates, cancellation rules, and the total financial impact is essential for borrowers considering lower down payment options.

Exploring alternatives such as larger down payments, piggyback loans, lender-paid PMI, or government-backed loans can help reduce or eliminate PMI costs. A thorough analysis that includes both direct PMI premiums and the opportunity cost of down payment funds enables homebuyers to make more informed and financially prudent mortgage choices.