For many homeowners, the mortgage is not only the largest component of their monthly expenses but also a significant factor in their long-term financial health. Reducing the mortgage interest rate can lead to lowered monthly payments and substantial savings over the duration of the loan, sometimes amounting to tens of thousands of dollars. This makes understanding and pursuing ways to reduce mortgage interest rates a priority for those looking to optimize their finances and build equity more efficiently, explains Abacus Avenue Team.

There are multiple strategies available to homeowners seeking to lower their mortgage interest rates, each with distinct eligibility requirements, benefits, and considerations. Conventional refinancing remains a popular choice, allowing borrowers to replace their existing loan with one that carries a lower rate or modified terms. Meanwhile, government-backed refinance programs provide streamlined options for veterans, FHA loan holders, and other eligible borrowers, often with reduced documentation and fees. These programs are designed to ease access to lower rates while safeguarding borrowers’ interests.

In addition to refinancing, loan modifications and alternative methods such as mortgage rate buydowns and mortgage recasting offer homeowners additional ways to reduce their effective interest rates or monthly payments. Each approach involves different processes and impacts, making it crucial for borrowers to carefully assess their credit profiles, current loan terms, equity positions, and financial goals. Gaining a comprehensive understanding of these options empowers homeowners to make informed decisions that maximize savings and improve their mortgage situations.

Refinancing Your Mortgage

Refinancing your mortgage involves replacing your current loan with a new one, often to obtain a lower interest rate, reduce monthly payments, or adjust the loan term. Conventional refinancing requires credit approval and may involve closing costs typically ranging from 2% to 6% of the loan amount. For example, reducing your interest rate by one percentage point on a $300,000 mortgage could save approximately $333 per month, translating to over $4,000 annually in savings.

Government-backed refinance programs offer streamlined options with less stringent underwriting. The VA IRRRL targets veterans with existing VA loans, allowing them to refinance with reduced documentation and potentially lower rates. The FHA Streamline Refinance similarly helps FHA mortgage holders reduce rates with limited requirements. These programs may waive appraisals and credit checks under certain conditions, accelerating the process and lowering upfront costs.

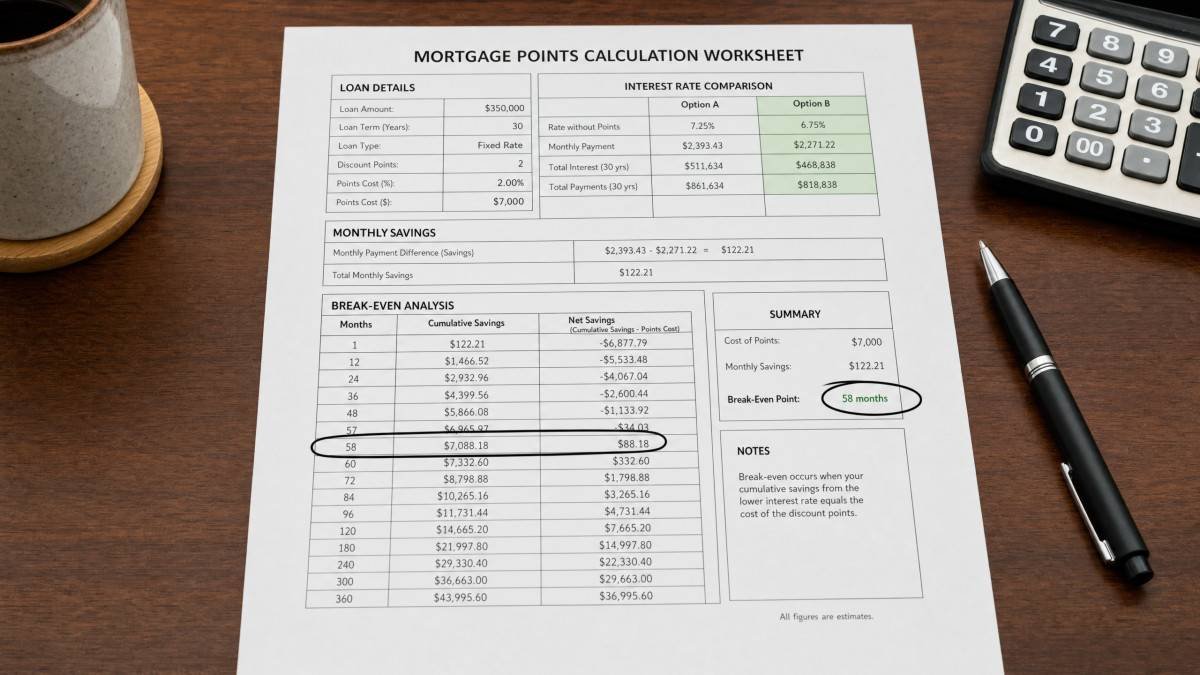

When considering refinancing, it is important to calculate the break-even point, which is the time it takes for the monthly savings to cover the closing costs associated with the new loan. Typically, if you plan to stay in your home beyond this period, refinancing becomes a financially sound decision. Additionally, borrowers should be aware that shortening the loan term through refinancing can increase monthly payments but reduce total interest paid, while extending the term can lower monthly payments but increase long-term interest expenses.

Another consideration is the impact of refinancing on your credit score. Applying for a refinance involves a hard credit inquiry, which can result in a temporary dip in your credit score. However, if managed properly and combined with timely payments on the new loan, your credit score can recover and even improve over time. It is advisable to shop for refinance rates within a focused window—usually 14 to 45 days—to minimize multiple inquiries’ impact on your credit.

Government-Backed Refinance Programs

Several government programs, including VA IRRRL, FHA Streamline Refinance, and initiatives by Fannie Mae and Freddie Mac, provide specialized refinance options to lower mortgage interest rates. The VA IRRRL allows eligible veterans to refinance existing VA loans with minimal documentation and typically no appraisal, helping reduce monthly payments or convert adjustable rates to fixed rates. Borrowers pay a one-time VA funding fee that can be rolled into the loan.

Fannie Mae’s RefiNow™ program requires a minimum 0.50% interest rate reduction and a lower monthly payment, targeting Fannie Mae-owned loans. Freddie Mac’s Refi Possible® assists low- and moderate-income borrowers, allowing high debt-to-income ratios up to 65% and waiving minimum credit score requirements. Both programs often waive appraisals to reduce costs. FHA Streamline Refinance requires the existing loan to be current and provides a net tangible benefit, with cash back limited to $500.

These government programs are designed to increase accessibility for borrowers who might not qualify for conventional refinancing due to credit challenges or income limitations. They often feature more flexible underwriting standards and reduced documentation requirements, which can speed up processing times. For example, the VA IRRRL program does not require a new credit check or income verification in most cases, making it an efficient option for veterans looking to lower their interest rates quickly.

In addition to lowering interest rates, some government programs allow borrowers to switch from adjustable-rate mortgages (ARMs) to fixed-rate loans, providing payment stability and protection against future rate increases. This can be particularly advantageous in a rising interest rate environment. However, borrowers should carefully review program-specific fees, such as VA funding fees or FHA mortgage insurance premiums, to understand the full cost implications before proceeding.

Loan Modification to Lower Interest Rate

A loan modification permanently changes one or more terms of your existing mortgage to make payments more affordable, often including interest rate reductions. Unlike refinancing, it does not replace your loan but adjusts it, typically for borrowers facing financial hardship. Eligibility generally requires demonstrating difficulty in meeting current payments and being at least one month delinquent.

Modifications can extend the loan term, reduce interest rates temporarily or permanently, or forbear a portion of principal. Government programs, such as FHA’s Standalone Loan Modification, assist borrowers in modifying loans to prevent foreclosure. The Consumer Financial Protection Bureau recommends proactively contacting mortgage servicers to explore modification options before missing payments.

Loan modifications can be a critical tool for borrowers experiencing temporary or permanent financial difficulties, such as job loss, medical emergencies, or other unforeseen circumstances. Unlike refinancing, loan modifications typically do not require a new credit application or appraisal, making them more accessible for struggling borrowers. Some modifications may also reduce principal balances in rare cases, though most focus on adjusting payment terms to improve affordability.

Servicers are required by law to evaluate borrowers for all available workout options, including loan modifications, before initiating foreclosure proceedings. Borrowers should maintain open communication with their mortgage servicers and provide requested documentation promptly to increase their chances of approval. While modifications can lower interest rates and monthly payments, they may also extend the loan term, potentially increasing total interest paid over time, so borrowers should weigh these factors carefully.

Other Strategies to Lower Mortgage Rates

Beyond refinancing and modifications, homeowners can reduce their effective mortgage interest rate through rate buydowns or mortgage recasting. A mortgage rate buydown involves paying points upfront—commonly one point equals 1% of the loan amount—to lower the interest rate by about 0.25% per point paid. Temporary buydowns, such as a 3-2-1 buydown, reduce rates gradually over the first three years.

Mortgage recasting allows borrowers to make a large principal payment, after which the lender recalculates monthly payments based on the reduced balance, maintaining the original interest rate and loan term. This lowers monthly payments without incurring new closing costs or refinancing. Recasting is especially beneficial for those receiving a lump sum, such as a bonus or inheritance, seeking to reduce monthly expenses without changing loan structure.

Rate buydowns can be especially attractive in a higher interest rate environment, where lowering the rate even slightly can lead to meaningful monthly savings. While paying points upfront increases initial costs, the long-term savings may justify this expense for homeowners planning to remain in their homes for several years. Some lenders also offer seller-paid buydowns as incentives during home purchases, which can reduce the initial interest rate without direct cost to the buyer.

Mortgage recasting requires lender approval and is not offered by all loan servicers. Unlike refinancing, recasting does not reset the loan term or require full underwriting, making it a faster and lower-cost option for reducing monthly payments. However, recasting is generally only available on conventional loans and not government-backed loans, and the minimum principal payment required to trigger a recast varies by lender. Borrowers should contact their servicer to understand the specific requirements and benefits.

Comparison of Mortgage Refinance Options

The following table compares key features of various refinance options to help homeowners evaluate which approach best suits their needs.

| Feature | Conventional Refinance | VA Interest Rate Reduction Refinance Loan (IRRRL) | FHA Streamline Refinance | Fannie Mae RefiNow / Freddie Mac Refi Possible |

|---|---|---|---|---|

| Eligibility | Broad; credit-dependent | Existing VA-backed loan holder | Existing FHA-insured loan holder | Fannie Mae/Freddie Mac-owned loan; income limits apply |

| Credit Score Impact | Significant; higher scores get better rates | Less emphasis; still considered | Less emphasis; may waive new credit check | Moderate to significant |

| Down Payment | Not applicable (refinance) | Not applicable (refinance) | Not applicable (refinance) | Not applicable (refinance) |

| Equity Requirement | Typically 20% to avoid PMI | No specific equity requirement | No specific equity requirement | Can be low (e.g., 3% for HomeReady) |

| Appraisal Required? | Often required | Often waived | Often waived | Often waived (RefiNow) |

| Net Tangible Benefit Required | Not always required | Required | Required | Required (e.g., 0.50% rate reduction for RefiNow) |

| Cash-out Option | Yes; limited or full cash-out | No; limited to $500 | No; limited to $500 | Limited (e.g., $2,000 or 2% for HomeReady) |

| Mortgage Insurance | PMI if equity <20% | No PMI; VA funding fee applies | MIP (Mortgage Insurance Premium) applies | PMI if equity <20% |

Frequently Asked Questions

How much can I save by lowering my mortgage interest rate?

Savings depend on your loan balance, current rate, and new rate. For instance, reducing your interest rate by one percentage point on a $300,000 mortgage saves roughly $333 monthly, exceeding $4,000 annually. Over a 30-year loan, this can accumulate to tens of thousands in savings, making even small rate reductions financially significant. The exact savings also depend on the loan term and whether you refinance to a shorter or longer term, as shorter terms typically save more interest overall.

What is the minimum credit score required to refinance for a lower interest rate?

Generally, a credit score of 740 or higher qualifies borrowers for the most competitive rates. However, government-backed programs like FHA and VA loans accept lower scores, expanding access. Improving your credit score by even a few points can help you secure a more favorable interest rate and reduce your overall mortgage costs. Some programs waive credit checks entirely or have more flexible criteria, which can be beneficial for borrowers with less-than-perfect credit histories.

Are there any government programs to help me lower my mortgage interest rate?

Yes. The VA Interest Rate Reduction Refinance Loan (IRRRL) assists veterans with existing VA loans. The FHA Streamline Refinance helps current FHA mortgage holders reduce rates with limited documentation. Fannie Mae and Freddie Mac offer programs such as RefiNow™ and Refi Possible®, which facilitate refinancing at lower rates for eligible borrowers, often waiving appraisal requirements. These programs are designed to reduce barriers like high closing costs and documentation burdens.

What are the costs associated with refinancing my mortgage?

Closing costs typically range from 2% to 6% of the loan amount, covering appraisals, title insurance, lender fees, and administrative expenses. Some lenders offer “no-cost” refinances by incorporating fees into the loan balance or charging higher interest rates. Calculating the break-even point helps determine if refinancing savings outweigh these costs within a reasonable timeframe. Additionally, government-backed refinance programs often reduce or waive some fees, lowering upfront expenses for qualifying borrowers.

Can I lower my interest rate without refinancing?

Yes. Loan modifications permit permanent adjustments to existing loan terms, including interest rate reductions, primarily for borrowers facing financial hardship. Mortgage recasting lowers monthly payments by recalculating payments after a lump-sum principal payment without changing the interest rate or loan term. However, these options depend on lender policies and borrower eligibility. They may not be available to all borrowers but can be valuable alternatives to refinancing when circumstances prevent obtaining a new loan.

Conclusion

Lowering your mortgage interest rate can lead to substantial financial savings through various avenues such as refinancing, loan modifications, rate buydowns, or recasting. Refinancing remains the most common and often most effective method, with conventional and government-backed programs offering tailored options to suit different borrower profiles. Understanding eligibility requirements, potential savings, and associated costs is essential for making an informed decision that fits your financial goals.

Government programs like the VA IRRRL and FHA Streamline Refinance simplify the process for eligible borrowers, while Fannie Mae and Freddie Mac initiatives provide additional alternatives. Other strategies like loan modifications and mortgage recasting offer solutions for those facing hardship or seeking to reduce monthly payments without a full refinance. Evaluating these options carefully, comparing multiple lender offers, and considering your credit score and equity position will help you secure the lowest possible mortgage interest rate.