Property taxes significantly influence the total amount homeowners pay each month for their mortgage. These taxes are often included in the monthly mortgage payment through an escrow account, which collects funds to pay local tax authorities on the homeowner’s behalf, notes 480 Realty & Property Management company. Because property tax rates and assessed values fluctuate, the monthly mortgage payment can change accordingly, affecting household budgeting and financial planning.

Calculating property taxes involves multiplying the assessed value of a property by the local tax rate or millage rate. For example, a home assessed at $400,000 with a 2% tax rate results in $8,000 in annual taxes. This annual amount is typically divided by 12 and added to the monthly mortgage payment. Understanding how these calculations work and how property taxes integrate into mortgage payments helps homeowners anticipate changes and avoid surprises.

Many lenders require escrow accounts to manage property tax payments, ensuring taxes are paid on time and protecting both the homeowner and lender from penalties or liens. Laws and regulations, including those from the Consumer Financial Protection Bureau and HUD, govern escrow management. Additionally, tax deductions like the SALT deduction affect the overall financial impact of property taxes on homeowners’ federal income taxes.

How Property Taxes Are Calculated

Property taxes are calculated by multiplying the assessed value of a property by the local tax rate or millage rate. The assessed value is often a fraction of the market value, determined by local tax assessors, and may be adjusted annually. For instance, if a home has an assessed value of $300,000 and the tax rate is 1.5%, the annual property tax would be $4,500. Alternatively, using mills, if the millage rate is 15 mills, the calculation would be $300,000 multiplied by 15 mills divided by 1,000, also equaling $4,500.

It is important to distinguish between market value and assessed value since many jurisdictions tax only a portion of the market value. Additionally, property tax exemptions, such as homestead exemptions, can lower the taxable amount. Variations in local tax rates and assessed values cause property tax bills to fluctuate from year to year, which impacts the monthly mortgage payment when taxes are included through escrow.

Impact of Property Taxes on Mortgage Payments

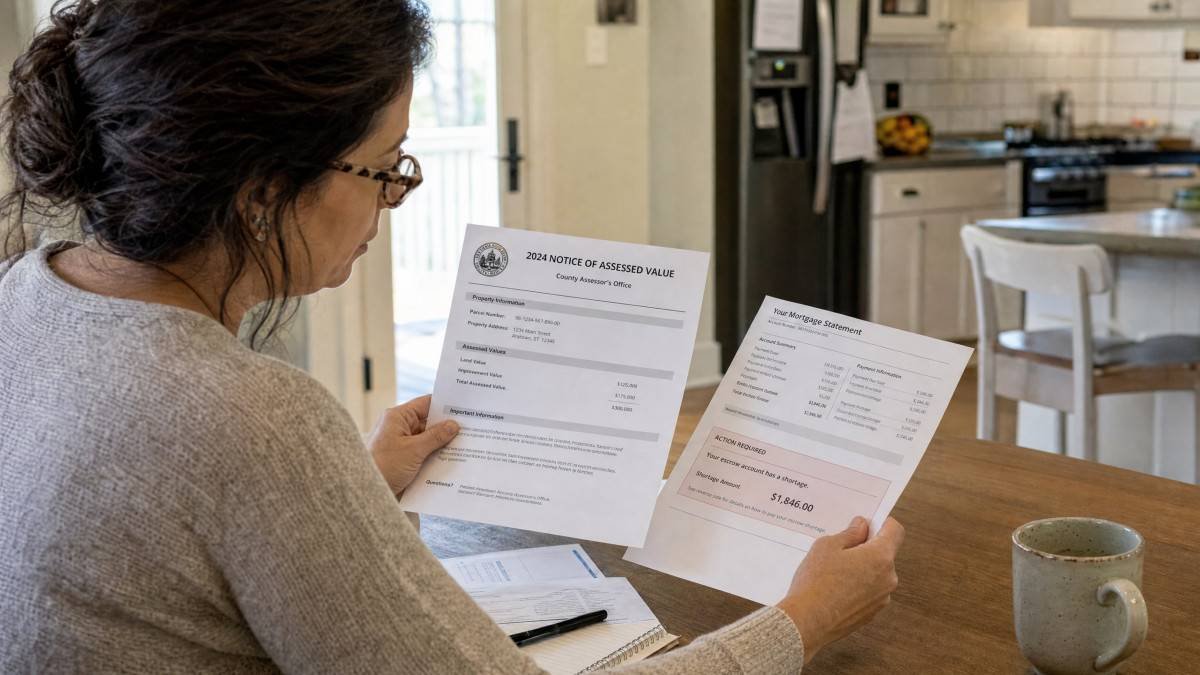

Most homeowners with mortgages pay property taxes through escrow accounts managed by their lenders. A portion of the monthly mortgage payment is allocated to this escrow account, which accumulates funds to pay property taxes when they become due. This system spreads out the tax burden over 12 months, avoiding large lump-sum payments. The total monthly payment commonly includes principal, interest, taxes, and insurance, known as PITI.

Escrow accounts protect lenders by ensuring property taxes are paid promptly, preventing tax liens that could threaten mortgage security. Lenders, especially those with FHA-insured loans, often require escrow accounts. Each year, servicers perform an escrow analysis to adjust monthly contributions based on changes in tax bills or insurance premiums. Significant increases in property taxes can raise monthly mortgage payments, sometimes with as little as 30 days’ notice, affecting household cash flow.

Comparison of Property Tax Payment Methods: Escrow vs. Direct Payment

Homeowners either pay property taxes through an escrow account managed by their lender or directly to the tax authority. Each method has distinct advantages and risks. Escrow accounts offer convenience and reduce the risk of late payments but limit homeowner control over funds. Direct payments provide more control but require careful budgeting and timely payment to avoid penalties.

The table below compares key features of both payment methods to clarify their differences and financial implications for homeowners.

| Feature | Payment via Escrow Account | Direct Payment to Tax Authority |

|---|---|---|

| Convenience | High; lender manages payments, reducing homeowner burden. | Lower; homeowner must track due dates and make payments. |

| Budgeting | Easier; monthly contributions spread cost evenly. | Requires saving for large, infrequent payments. |

| Risk of Late Payment | Low; lender ensures timely payments, minimizing penalties. | Higher; homeowner must avoid late payments to prevent liens. |

| Control over Funds | Lower; funds held by lender without substantial interest earnings. | Higher; homeowner retains funds until payment due date. |

| Lender Requirement | Often required, especially for FHA loans or high loan-to-value ratios. | Permitted by some lenders, often with financial qualifications. |

| Annual Adjustments | Monthly payments adjusted annually based on escrow analysis. | Homeowner pays adjusted tax bills directly. |

Laws, Regulations, and Government Programs Affecting Property Taxes

The Consumer Financial Protection Bureau (CFPB) regulates mortgage servicers’ handling of escrow accounts, requiring timely payments to avoid penalties and tax liens. The CFPB advises homeowners to contact servicers immediately if taxes are unpaid and to provide a formal notice of error. HUD mandates escrow accounts for FHA-insured mortgages to ensure taxes and insurance are paid promptly, protecting both homeowners and lenders.

Freddie Mac guidelines require servicers to collect sufficient escrow funds and conduct annual analyses to adjust payments for property taxes and insurance. These guidelines also define procedures for managing escrow surpluses and shortages. The Internal Revenue Service permits homeowners to deduct property taxes on federal returns through the SALT deduction, capped at $10,000 per household under the Tax Cuts and Jobs Act of 2017. This cap is scheduled to increase by 1% annually starting in 2026, reaching $40,000 by 2029 for taxpayers earning under $500,000.

Common Misconceptions About Property Taxes and Mortgage Payments

One common misconception is that property taxes are fixed. In reality, property taxes often change annually due to reassessments, tax rate adjustments, or expiration of exemptions. Homeowners should expect fluctuations and plan accordingly. Another misunderstanding is that property taxes are always included in the mortgage payment. While many lenders require escrow accounts, some allow direct payment, which necessitates disciplined budgeting to avoid late fees.

Some believe escrow accounts earn significant interest; however, any interest earned is generally minimal and often offset by administrative fees, depending on state laws. Lastly, increases in property taxes are often attributed solely to rising home values, but other factors such as increased local government spending or changes in tax policy can also cause tax increases even if property values remain stable.

Frequently Asked Questions

What happens if my mortgage servicer fails to pay my property taxes from my escrow account?

If your mortgage servicer does not pay your property taxes on time, you should immediately contact them and provide a formal notice of error. You should also notify your local tax authority to avoid penalties or a tax lien on your property. The Consumer Financial Protection Bureau recommends consulting a HUD-approved housing counselor or attorney if the issue remains unresolved. Prompt action is critical to prevent fines or legal complications.

Can I choose to pay my property taxes directly instead of through an escrow account?

Some lenders allow homeowners to pay property taxes directly, but this depends on lender policy and loan type. Direct payment requires the homeowner to budget for large, infrequent tax bills, which are typically due annually or semi-annually. Choosing direct payment increases the risk of late payments and penalties if funds are not set aside properly. Many FHA loans and high loan-to-value mortgages require escrow accounts, limiting this option.

How often do property tax assessments change and affect my mortgage payment?

Property tax assessments can change annually or on a periodic basis depending on local government schedules. Changes in assessed value or tax rates alter the annual property tax bill. Mortgage servicers perform an escrow analysis annually and adjust the monthly escrow payment accordingly. This adjustment changes the total monthly mortgage payment to reflect updated tax obligations, which homeowners should anticipate during budgeting.

Are there exemptions that reduce my property tax burden?

Many jurisdictions offer exemptions that lower taxable property values, including homestead exemptions for primary residences, and exemptions for seniors, veterans, and disabled individuals. These exemptions reduce the annual property tax bill and thus the monthly mortgage payment if taxes are escrowed. Eligibility and application requirements vary by location, so homeowners should research local programs to maximize savings.

What is the SALT deduction and how does it relate to property taxes?

The State and Local Tax (SALT) deduction allows taxpayers who itemize to deduct property taxes and other state and local taxes on federal income tax returns. The Tax Cuts and Jobs Act of 2017 capped this deduction at $10,000 per household. This limit reduces the federal tax benefit of high property tax payments, particularly in high-tax states. The cap is set to increase annually by 1% starting in 2026, reaching $40,000 by 2029 for incomes under $500,000.

Conclusion

Property taxes are a critical factor influencing monthly mortgage payments through escrow accounts that help homeowners manage large annual tax bills by spreading payments monthly. Understanding the calculation of property taxes, their variability, and how they integrate into mortgage payments allows homeowners to better plan their finances and anticipate changes. Escrow accounts offer convenience and reduce the risk of late payments, although they limit control over funds.

Laws and regulations from entities such as the CFPB, HUD, and Freddie Mac ensure proper management of escrow accounts and timely payment of property taxes. Additionally, tax benefits like the SALT deduction provide some relief but come with limitations. Homeowners should remain informed about local exemptions and reassessments to avoid surprises and ensure their mortgage payment accurately reflects their tax obligations.