Saving for a down payment is the initial financial step required when purchasing a home, reports TPG Management experts. It involves setting aside a lump sum, usually expressed as a percentage of the home’s purchase price, to be paid upfront. Typically, a down payment ranges from 3% to 20%, with 20% being the standard amount needed to avoid private mortgage insurance (PMI). Effectively accumulating these funds requires strategic planning and disciplined saving habits. Without a clear plan, the process can feel overwhelming, but a structured approach can help maintain focus and motivation.

The amount needed for a down payment varies depending on the loan type and the price of the home. For example, conventional loans generally require between 3% and 20% down, while government-backed loans like FHA and VA have different minimum requirements. The timeline and method for saving depend on individual income, expenses, and financial goals, making it essential to create a tailored approach to reach the target amount efficiently. Understanding one’s personal financial landscape allows for adjustments as circumstances change, making the saving process more adaptable and realistic.

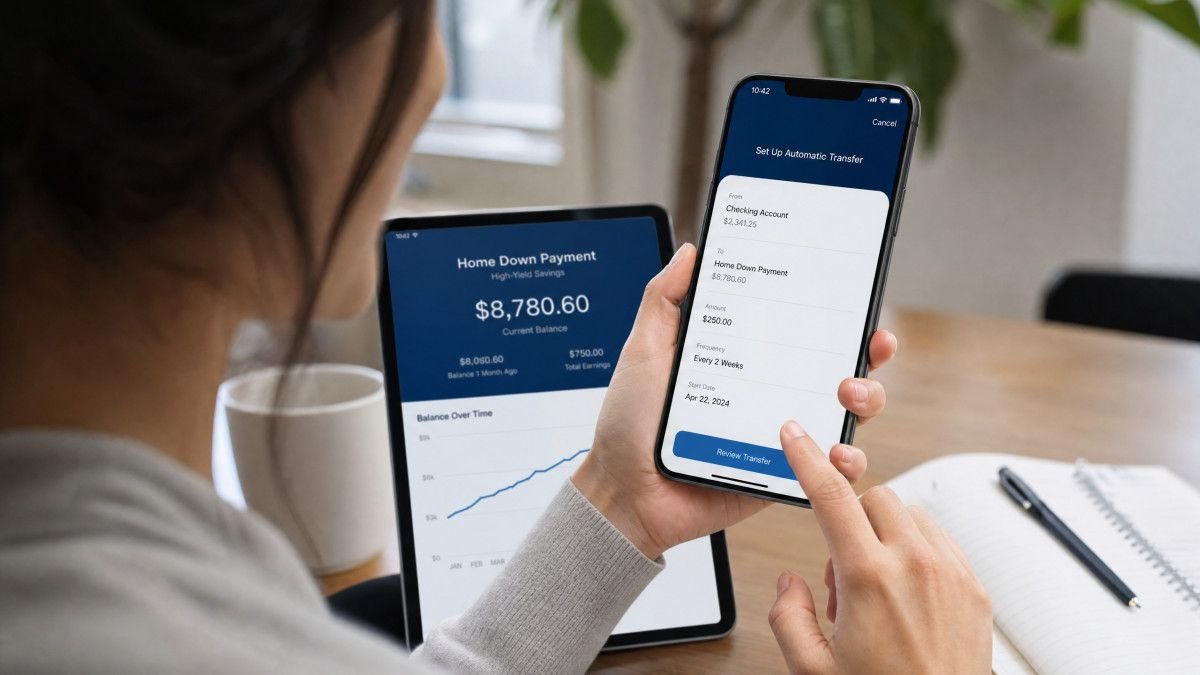

Adopting a combination of savings strategies can make the process more manageable. Automating transfers to a high-yield savings account, auditing budgets to reduce discretionary spending, and exploring down payment assistance programs are proven methods. These approaches help ensure consistent progress toward the down payment goal, improve loan qualification prospects, and reduce the financial burden of homeownership. Establishing milestones and regularly reviewing progress can also enhance motivation and offer opportunities to refine saving tactics as needed.

Understanding Down Payment Requirements

Down payment requirements depend largely on the type of mortgage loan chosen and the borrower’s financial circumstances. Conventional loans typically require between 3% and 20% down. For those able to put 20% down, private mortgage insurance (PMI) can be avoided, reducing monthly payments. FHA loans require a minimum down payment of 3.5% for borrowers with credit scores above 580 and 10% for those with lower scores. VA and USDA loans often offer no down payment options for eligible buyers.

The percentage required translates directly into the amount of money needed upfront. For instance, on a $400,000 home, a 20% down payment amounts to $80,000, while a 3% down payment for a conventional loan would be $12,000. Understanding these requirements helps buyers plan realistically and explore loan options that fit their financial capabilities and long-term objectives.

In addition to loan type and credit score, lenders may consider other factors such as employment history and savings history when determining down payment requirements. Some loans may also have specific stipulations related to borrower income or property type, which can influence the minimum necessary down payment. Being aware of these nuances allows prospective buyers to better prepare and align their saving strategies with lender expectations.

Moreover, the size of the down payment not only affects upfront costs but also influences monthly mortgage payments and overall loan affordability. A larger down payment typically results in lower monthly payments and can improve loan terms, while a smaller down payment might increase overall loan costs due to added fees or insurance requirements. Careful consideration of these trade-offs is vital when setting a down payment goal.

Strategies for Saving Effectively

One of the most reliable ways to save for a down payment is to automate the process. Setting up a fixed monthly transfer to a dedicated high-yield savings account immediately after receiving a paycheck ensures consistent contributions without relying on memory or willpower. High-yield savings accounts typically offer annual percentage yields (APY) between 4% and 5%, significantly higher than traditional savings accounts, which often yield less than 0.1%.

Alongside automation, conducting a thorough budget audit to identify and reduce discretionary spending can free up additional funds to allocate toward savings. Increasing income through side jobs, overtime hours, or bonuses can also accelerate the saving timeline. Reducing existing debt lowers the debt-to-income ratio, which improves loan qualification chances and may allow more funds to be directed toward a down payment.

Another effective strategy is to take advantage of windfalls such as tax refunds, work bonuses, or monetary gifts by directing these funds straight into the down payment savings account. This can provide substantial boosts to the overall savings balance. Setting realistic, incremental savings milestones and celebrating each achievement can help maintain motivation throughout the process.

It is also helpful to separate the down payment savings from everyday checking accounts to avoid the temptation of spending these funds. Using tools like budgeting apps or financial tracking software can give clear visibility into progress, helping to adjust saving rates or spending habits if necessary. Staying disciplined and consistent in saving efforts is key to reaching the goal in a timely manner.

Comparing Loan Types and Down Payment Requirements

Different loan types have varying down payment requirements and eligibility criteria. Conventional loans are flexible, requiring from 3% up to 20% down, but they may require PMI if less than 20%. FHA loans are popular among first-time buyers, requiring 3.5% down for eligible credit scores, with higher requirements for lower scores. VA and USDA loans stand out by offering zero down payment options, but applicants must meet military service or geographic criteria.

Choosing the appropriate loan type influences how much a buyer needs to save and affects overall affordability. Understanding these differences is essential for efficient planning and ensuring the down payment aligns with the borrower’s financial situation and loan eligibility.

Jumbo loans, which are used for loan amounts exceeding conforming loan limits, typically require higher down payments ranging from 10% to 20%. These loans generally demand stronger credit profiles and financial reserves. Prospective buyers considering luxury or high-cost properties should factor in these elevated requirements when setting their savings goals.

Additionally, some loans offer special programs or incentives designed to reduce down payment barriers, such as first-time homebuyer programs or community lending initiatives. Researching these options can help identify opportunities to minimize upfront costs and expand financing possibilities. It is advisable to consult with mortgage professionals to understand which loan type best suits individual financial situations and homeownership goals.

| Loan Type | Minimum Down Payment | PMI Requirement | Eligibility Factors |

|---|---|---|---|

| Conventional | 3% – 20% | Yes, if under 20% | Credit score, income, debt-to-income ratio |

| FHA | 3.5% (580+ score) 10% (500-579 score) |

Mortgage insurance required | Credit score, first-time buyers favored |

| VA | 0% | No PMI | Eligible veterans and active military |

| USDA | 0% | No PMI | Rural areas, income limits apply |

| Jumbo | 10% – 20% | Typically required | High loan amounts, strong credit required |

Utilizing Down Payment Assistance Programs

Down payment assistance (DPA) programs offer grants, low-interest second mortgages, or forgivable loans to eligible buyers, particularly first-time homebuyers. Many states and local governments provide such programs, often with income limits and other qualifying criteria. These resources can alleviate the upfront cost burden and make homeownership accessible to those with limited savings.

Employers may also offer down payment assistance as part of benefits packages. Combining DPA with personal savings and gift funds from family members can significantly reduce the amount a buyer needs to save independently. Understanding program requirements and application processes is important to maximize these opportunities and incorporate them into a comprehensive saving strategy.

Some DPA programs are designed to be combined with specific loan types, such as FHA or conventional loans, which can broaden eligibility and ease qualification. It is advisable to research local programs thoroughly, as availability and terms can vary widely by region. Early engagement with housing counselors or nonprofit organizations can provide valuable guidance and help identify all assistance options.

Beyond financial aid, certain programs may offer education and counseling services to prepare buyers for the responsibilities of homeownership. These resources enhance borrower readiness and increase the likelihood of successful loan repayment and long-term stability. Taking advantage of such holistic support can lead to better outcomes for first-time and repeat homebuyers alike.

Calculating Timeline and Setting a Saving Goal

Establishing a clear goal and timeline for saving a down payment provides motivation and structure. Dividing the target amount by the monthly savings contribution derives the number of months needed to reach the goal. For example, saving $40,000 at $1,000 per month requires 40 months, or about 3.3 years. Adjusting monthly savings or the target down payment can shorten or lengthen this timeline.

Including closing costs in the budget is essential, as they typically add 2% to 5% of the purchase price in upfront expenses. Allocating funds for these costs prevents surprises during home purchase. Tracking progress regularly helps identify if savings are on pace or if adjustments are needed. This disciplined approach supports meeting financial objectives within a realistic timeframe.

Setting intermediary milestones along the way can help maintain motivation and allow for reassessment of goals. For instance, marking progress every quarter or year provides an opportunity to celebrate achievements and make any necessary course corrections. Flexibility is important as unexpected expenses or changes in income may require revising the savings plan.

It is also prudent to factor in inflation and potential changes in home prices when calculating the timeline. Market fluctuations can affect the required down payment amount, so regularly reviewing real estate trends can help anticipate adjustments in savings targets. Remaining adaptable while maintaining steady contributions ensures ongoing progress toward homeownership.

Frequently Asked Questions

What is the minimum down payment required for different loan types?

The minimum down payment varies by loan type. Conventional loans usually require at least 3%, FHA loans require 3.5% for borrowers with credit scores above 580, and VA and USDA loans may require no down payment for eligible applicants. Jumbo loans typically require 10% or more. It is important to consider that some programs targeting first-time buyers might offer reduced down payment options as well.

When is private mortgage insurance (PMI) required?

PMI is generally required for conventional loans when the down payment is less than 20% of the home’s purchase price. It protects the lender in case of default and increases monthly mortgage costs until sufficient equity is built. Once the borrower reaches 20% equity in the home, PMI can often be removed, lowering monthly payments.

What is the best type of account to save for a down payment?

A high-yield savings account (HYSA) is often the best option for down payment savings because it offers better interest rates than traditional savings accounts, typically between 4% and 5% APY. This helps the savings grow faster while keeping funds accessible. Additionally, HYSAs are usually federally insured, providing safety for the deposited funds.

Can gift funds be used for a down payment?

Yes, most loan programs, including FHA and conventional loans, allow the use of gift funds from family members. A gift letter documenting that the funds are non-repayable is usually required by lenders to verify the source. Some lenders may have specific guidelines on who can provide gift funds and the documentation needed.

Are down payment assistance programs widely available?

Down payment assistance programs are offered in most states and many local jurisdictions, primarily targeting first-time buyers. These programs can provide grants or low-interest loans to help cover the down payment and sometimes closing costs, subject to income and eligibility criteria. Availability and terms vary, so researching local options is essential for maximizing benefits.

Conclusion

Saving for a down payment effectively requires a combination of informed planning, disciplined saving habits, and knowledge of available resources. Understanding the specific down payment requirements tied to different loan types helps set realistic goals. Using automation and high-yield savings accounts ensures steady growth of funds while minimizing reliance on willpower. Conducting budget audits and exploring additional income streams can accelerate the timeline. This multifaceted approach empowers buyers to build savings steadily despite financial challenges.

Additionally, exploring down payment assistance programs and gift funds can substantially reduce the amount needed from personal savings. Calculating a clear timeline and factoring in closing costs ensures preparedness when purchasing a home. By employing these strategies consistently, prospective buyers can navigate the financial demands of homeownership more confidently and efficiently. Careful preparation and ongoing commitment are key to turning the dream of owning a home into reality.