When navigating the complex world of real estate finance, understanding the fundamental differences between a deed of trust and a mortgage is crucial for both homebuyers and lenders, notes Helios Property Management company. While both serve as security instruments that pledge real property as collateral for a loan, their legal structures, involved parties, and particularly their foreclosure processes can vary significantly depending on state law.

Understanding Mortgages: The Two-Party Agreement

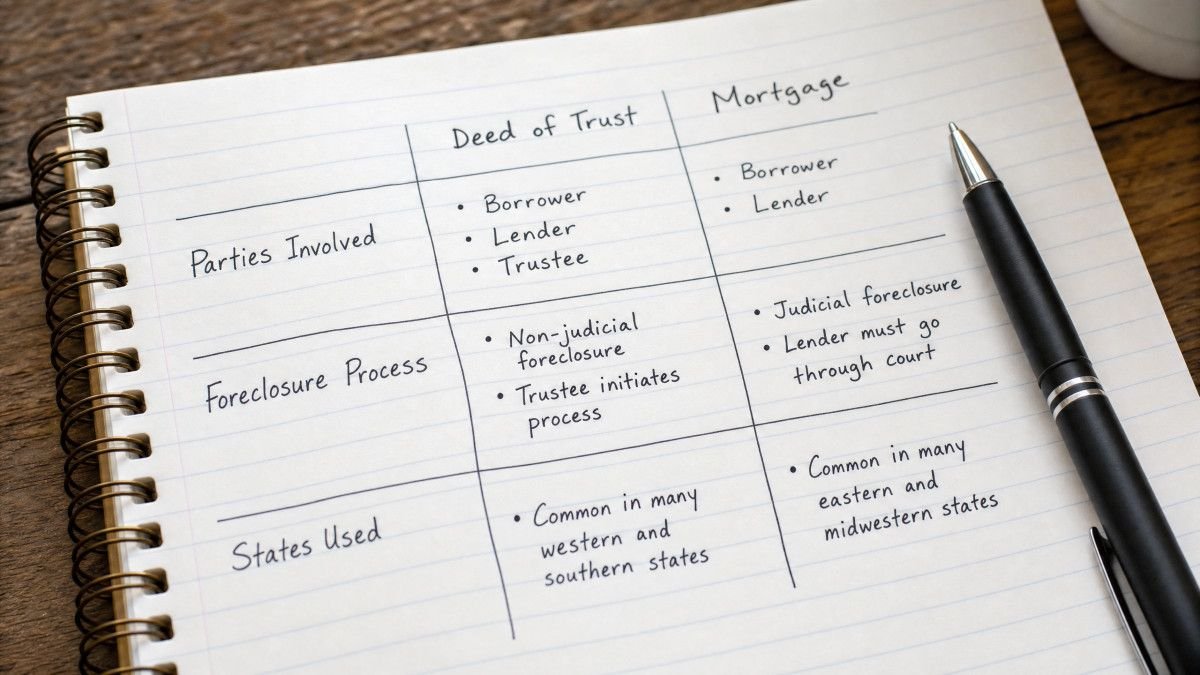

A mortgage is a legal agreement where a borrower pledges real estate as security for a loan, typically involving two parties: the borrower (mortgagor) and the lender (mortgagee), and usually necessitates a judicial foreclosure process in the event of default.

In essence, a mortgage is a contract that creates a lien on the property, giving the lender a claim against the property if the borrower fails to meet their repayment obligations. The borrower retains legal title to the property throughout the loan term, meaning they are the legal owner from the outset. This direct relationship between two parties—the individual or entity borrowing money and the financial institution providing it—is a hallmark of the mortgage system. For instance, if you secure a $300,000 loan to purchase a home, the mortgage document legally ties that property to your repayment promise. Should you, for some unforeseen reason, become unable to make your monthly payments, the lender’s primary recourse is to initiate a foreclosure proceeding.

The Judicial Foreclosure Process

Foreclosure under a mortgage typically involves a judicial process, meaning the lender must file a lawsuit in court to obtain a judgment allowing them to sell the property to satisfy the debt. This court-supervised process can be lengthy and costly, often taking several months, or even years, depending on the state and the specifics of the case. The court oversees every step, from verifying the validity of the lien to approving the sale of the property. This judicial oversight provides a layer of protection for the borrower, offering opportunities to raise defenses or negotiate alternatives to foreclosure. For example, a borrower might argue that the lender did not follow proper notification procedures, potentially delaying or even halting the foreclosure. This can be a source of frustration for lenders, who face significant legal fees and extended timelines before they can recover their investment. However, it also means that borrowers in mortgage states often have more time to address their financial difficulties or seek legal counsel.

Mortgage Assignment and MERS

Mortgages are frequently bought and sold between financial institutions, a process known as assignment. When a mortgage is assigned, the new lender acquires the rights to receive payments and enforce the lien. These assignments are typically recorded in county land records to provide public notice of the change in ownership. However, the Mortgage Electronic Registration System, Inc. (MERS) was created to streamline this process. MERS acts as a nominee for the loan owner, tracking assignments electronically and often eliminating the need for physical recordation of each transfer. This system, while efficient, has sometimes led to legal challenges in foreclosure proceedings, as borrowers or courts question the standing of the foreclosing party if the chain of assignment through MERS is unclear. It’s a complex system, and sometimes, even seasoned legal professionals find themselves untangling the intricacies of who truly holds the note and the mortgage.

Understanding Deeds of Trust: The Three-Party Arrangement

A deed of trust is a security instrument involving three parties—the borrower (trustor), the lender (beneficiary), and a neutral third party (trustee)—where the trustee holds legal title to the property until the loan is repaid, often facilitating a nonjudicial foreclosure process.

Unlike a mortgage, a deed of trust introduces a third, independent party: the trustee. This trustee, often a title company, escrow company, or bank, holds the bare legal title to the property until the borrower (trustor) fully repays the loan to the lender (beneficiary). The borrower, however, retains equitable title and the right to use and occupy the property. This means that while the trustee technically holds the title, the borrower is still the homeowner in all practical aspects, responsible for maintenance, taxes, and enjoying the property. This three-party structure is a key differentiator from the two-party mortgage system.

The Nonjudicial Foreclosure Process

One of the most significant implications of a deed of trust is the typically nonjudicial nature of its foreclosure process. If a borrower defaults on their loan, the deed of trust usually contains a power of sale clause, which grants the trustee the authority to sell the property at a public auction without requiring court intervention. This process is generally much faster and less expensive for lenders compared to judicial foreclosures. For example, in states where deeds of trust are prevalent, a lender might initiate foreclosure proceedings within a few months of a borrower missing payments, whereas a judicial foreclosure could drag on for a year or more. This expedited process can be a significant advantage for lenders, but it also means borrowers have less time to react and fewer legal avenues to challenge the foreclosure in court. The trustee’s role is to ensure the process adheres to state-specific legal requirements, which can still be complex, but without the direct oversight of a judge.

Deed of Trust Assignment

Similar to mortgages, deeds of trust can also be assigned to new lenders. These assignments are typically recorded in county land records, ensuring a clear chain of ownership for the debt and the security instrument. MERS also plays a role in tracking assignments of deeds of trust, aiming to simplify the transfer process and reduce recording fees. However, as with mortgages, the involvement of MERS can sometimes lead to complications or questions regarding proper documentation and the standing of the foreclosing party, particularly if the assignment records are not meticulously maintained. It’s a system designed for efficiency, but its complexity can sometimes create unexpected hurdles.

Key Differences and State Variations

The primary distinctions between a deed of trust and a mortgage lie in the number of parties involved, the holder of legal title during the loan term, and the typical foreclosure process, with state laws dictating which instrument is predominantly used.

The choice between a deed of trust and a mortgage is not typically up to the borrower; rather, it is determined by state law. Some states are “mortgage states,” while others are “deed of trust states.” A few states permit the use of both. For example, California, Texas, and Virginia are generally considered deed of trust states, while New York, Florida, and Pennsylvania are typically mortgage states. This geographical distinction is crucial because it directly impacts the foreclosure process and the rights of both borrowers and lenders. According to a report by the Mortgage Bankers Association, nonjudicial foreclosures, common in deed of trust states, generally have a shorter timeline, averaging around 120-180 days from default to sale, compared to judicial foreclosures, which can often exceed 300 days.

Title Holding

One of the most fundamental differences lies in who holds the legal title to the property during the repayment period. With a mortgage, the borrower retains legal title, and the lender holds a lien against the property. This means the borrower is the legal owner from day one. In contrast, with a deed of trust, the legal title is transferred to a neutral third-party trustee, who holds it until the loan is fully satisfied. The borrower holds equitable title, which grants them the right to use and enjoy the property, but not the legal ownership until the debt is cleared. This distinction can feel subtle, but it has profound implications, particularly if the loan goes into default. It can be a bit confusing to grasp that you’re living in a home you’re paying for, but technically, a third party holds the legal reins.

Foreclosure Process Implications

The differing foreclosure processes are perhaps the most significant practical distinction. Judicial foreclosures, typical of mortgages, offer borrowers more protection due to court oversight. This can include the right to present defenses, negotiate modifications, or even redeem the property by paying off the debt before the sale. However, this also means a longer, more expensive process for lenders. Nonjudicial foreclosures, characteristic of deeds of trust, are generally faster and less costly for lenders, as they bypass the court system. While borrowers still receive notice and have certain rights, the opportunities to challenge the foreclosure are often more limited and time-sensitive. This efficiency for lenders can translate into less flexibility for borrowers facing financial hardship, making the initial choice of security instrument a critical, albeit often unchosen, factor in homeownership.

Frequently Asked Questions

Q: What is the primary difference between a deed of trust and a mortgage?

A: The primary difference lies in the number of parties involved and the foreclosure process. A mortgage involves two parties (borrower and lender) and typically requires judicial foreclosure, while a deed of trust involves three parties (borrower, lender, and trustee) and often allows for nonjudicial foreclosure.

Q: Who holds the title to the property with a deed of trust?

A: With a deed of trust, a neutral third-party trustee holds the legal title to the property until the borrower fully repays the loan. The borrower retains equitable title, allowing them to use and occupy the property.

Q: Are deeds of trust used in all states?

A: No, deeds of trust are not used in all states. Some states primarily use mortgages, while others predominantly use deeds of trust. A few states permit both, with the choice often made by the lender.

Q: What is a power of sale clause, and how does it relate to deeds of trust?

A: A power of sale clause, typically found in a deed of trust, grants the trustee the authority to sell the property at a public auction without court intervention if the borrower defaults. This facilitates a faster, nonjudicial foreclosure process.

Q: Does a deed of trust offer more protection to the borrower than a mortgage?

A: Generally, a mortgage, with its judicial foreclosure process, offers more protection to the borrower due to court oversight and opportunities to present defenses. Deeds of trust, with nonjudicial foreclosure, tend to favor lenders with a quicker process.

Conclusion

Understanding the fundamental distinctions between a deed of trust and a mortgage is paramount for anyone involved in real estate transactions, from first-time homebuyers to seasoned investors. While both instruments serve the critical function of securing a loan with real property, their differing structures—two parties versus three—and the resulting foreclosure processes—judicial versus nonjudicial—have significant implications for the rights and responsibilities of borrowers and lenders alike. The choice between these instruments is largely dictated by state law, influencing the speed and legal complexities of recourse in the event of default. Navigating these nuances can feel daunting, but grasping the core differences empowers individuals to better comprehend their financial commitments and the legal landscape of their homeownership journey. Ultimately, knowing whether your security instrument is a mortgage or a deed of trust is not just a legal technicality; it’s a foundational piece of knowledge for any property owner.