A purchase money mortgage is a specific type of home loan directly tied to the acquisition of real estate, distinguishing itself from other financing methods. It’s essentially a loan provided to a buyer by either the seller of the property or a third-party lender, specifically for the purpose of funding that particular purchase. This arrangement is crucial in real estate transactions, especially when traditional bank financing might be challenging or less flexible, shares Heritage Property Management team.

Understanding the Core Concept of a Purchase Money Mortgage

A purchase money mortgage is a loan specifically granted for the acquisition of real property, often providing a direct financing avenue from the seller to the buyer. This means the funds are used exclusively to buy the property, and the property itself serves as collateral for that specific debt. Unlike a refinance or a home equity loan, which are secured by existing property, a purchase money mortgage is created simultaneously with the property’s transfer of ownership. This simultaneous creation gives it a unique legal standing, particularly concerning lien priority, which can be a significant advantage for the lender.

For instance, if a buyer secures a $300,000 loan from the seller to purchase a home, that $300,000 loan is the purchase money mortgage. The property immediately becomes collateral for this specific debt. This arrangement is distinct from a scenario where a buyer takes out a personal loan and then uses those funds to buy a house; in that case, the personal loan isn’t directly tied to the property’s purchase in the same way, and thus wouldn’t typically be classified as a purchase money mortgage. The direct link between the loan and the property acquisition is the defining characteristic, influencing its legal treatment and protections.

Seller Financing vs. Third-Party Lender

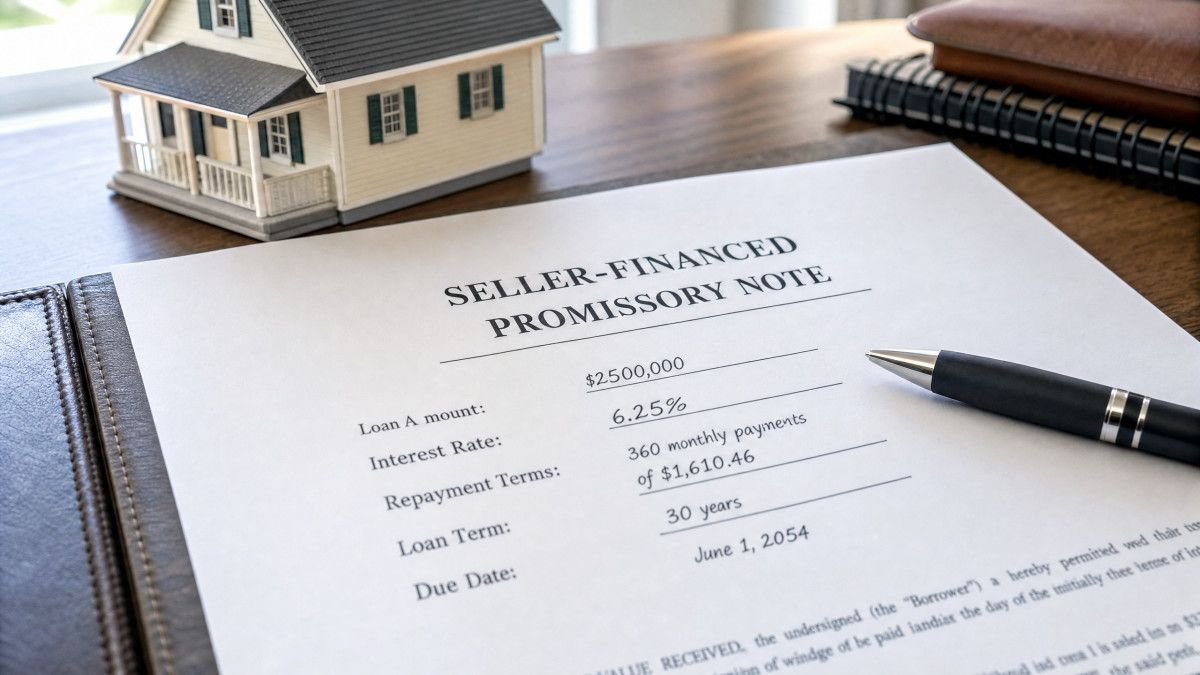

While often associated with seller financing, a purchase money mortgage can also originate from a third-party lender, though the former is more commonly highlighted. When a seller provides the financing, they essentially act as the bank, lending the buyer the money to purchase their home and receiving payments directly. This can be particularly beneficial in niche markets or for properties that might not qualify for conventional loans. For example, a seller might offer to finance a $250,000 property with a 10% down payment and a 5-year term at 6% interest, making the purchase accessible to a buyer who might struggle with traditional bank requirements.

Conversely, a third-party lender, such as a bank or credit union, can also issue a purchase money mortgage. In this more common scenario, the loan from the financial institution is still specifically for the purchase of the property, and it’s granted at the time of the sale. The key distinction from other types of mortgages is its purpose: it’s solely for the acquisition. The legal framework surrounding purchase money mortgages often grants them special priority over other liens, even those recorded earlier, because the loan is what enabled the purchase in the first place. This priority can be a complex legal point, and it’s one area where I’ve seen buyers and even some less experienced real estate professionals get tripped up, leading to unexpected complications down the line.

The Legal Standing and Priority of Purchase Money Mortgages

A purchase money mortgage typically holds a superior lien position compared to other types of mortgages or judgments against the buyer, even if those other liens were recorded earlier. This elevated status is a fundamental aspect of property law, designed to encourage property transactions by protecting the financing source. The rationale is straightforward: without the purchase money mortgage, the buyer wouldn’t have acquired the property, so the lender who provided the funds for the purchase should have the first claim on the property if the buyer defaults. This priority is often established by statute, varying slightly by jurisdiction, but the core principle remains consistent across most states.

According to the Cornell Law School’s Legal Information Institute, a purchase money mortgage is defined as “a mortgage that a buyer of real property gives to the seller as part of the transaction used to purchase that property.” This definition underscores the direct link between the loan and the acquisition. The priority granted to these mortgages is a significant protection for lenders, whether they are the seller or a third party. It ensures that if the property goes into foreclosure, the purchase money mortgage holder is typically the first to be paid from the proceeds, ahead of other creditors who might have claims against the buyer.

The Nuances of Lien Priority

The priority of a purchase money mortgage isn’t absolute and can be subject to specific conditions and jurisdictional rules. Generally, for a purchase money mortgage to maintain its superior priority, it must be recorded promptly after the transaction. If there’s a delay in recording, another lienholder who records their interest first might gain priority, depending on the state’s recording statutes (e.g., race, notice, or race-notice jurisdictions). This is a critical detail that can significantly impact the lender’s security. For instance, if a seller finances a $400,000 property but fails to record the mortgage for a month, and in the meantime, a contractor files a mechanic’s lien for $50,000, the priority could be contested, leading to a complex legal dispute.

Furthermore, the priority typically only applies to the portion of the loan used specifically for the purchase. If a buyer takes out a larger loan that includes funds for renovations or other purposes, the portion of the loan not used for the purchase might not enjoy the same priority status. This distinction is crucial for lenders to understand, as it affects their risk exposure. I’ve encountered situations where lenders assumed their entire loan had purchase money priority, only to discover later that a portion was subordinate to other liens, a realization that can be quite frustrating and financially damaging.

Key Benefits and Drawbacks for Buyers and Sellers

A purchase money mortgage offers distinct advantages, such as potentially easier qualification for buyers and a faster closing process, but it also carries risks like higher interest rates and the potential for foreclosure if the buyer defaults. For buyers, the primary benefit is often accessibility. If they have a less-than-stellar credit history or lack a substantial down payment, traditional lenders might reject their application. A seller, however, might be more willing to take on the risk, especially if they are eager to sell the property. This can open doors to homeownership that would otherwise be closed.

For sellers, offering a purchase money mortgage can make their property more attractive to a wider pool of buyers, potentially leading to a quicker sale and a higher purchase price. Additionally, the seller can earn interest on the loan, providing a steady stream of income over the loan term. For example, a seller who finances a $500,000 property at 7% interest over 15 years will receive significant interest payments in addition to the principal. However, this arrangement is not without its drawbacks. The seller assumes the risk of the buyer defaulting, which could necessitate a lengthy and costly foreclosure process to reclaim the property.

Weighing the Risks and Rewards

The decision to utilize a purchase money mortgage requires careful consideration of the associated risks and rewards for both parties. Buyers must be aware that seller financing often comes with higher interest rates than traditional bank loans, reflecting the increased risk taken by the seller. They might also face a balloon payment at the end of a relatively short term, such as 5 or 10 years, requiring them to refinance or pay off the remaining balance in full. If they are unable to secure refinancing at that time, they risk losing the property. This is a significant financial commitment that requires careful planning and a clear understanding of the terms.

Sellers, on the other hand, must assess the buyer’s financial stability and ability to repay the loan. They are essentially acting as a bank, and they need to perform due diligence to mitigate their risk. This might involve reviewing the buyer’s credit report, verifying their income, and requiring a substantial down payment. If the buyer defaults, the seller must navigate the foreclosure process, which can be complex and time-consuming, depending on the jurisdiction. The potential for a prolonged legal battle is a significant deterrent for some sellers, making them hesitant to offer financing despite the potential benefits.

Frequently Asked Questions About Purchase Money Mortgages

What is the main difference between a purchase money mortgage and a traditional mortgage?

The main difference is that a purchase money mortgage is created simultaneously with the property purchase and is often provided directly by the seller, whereas a traditional mortgage is typically obtained from a third-party financial institution like a bank or credit union.

Does a purchase money mortgage require a down payment?

Yes, a purchase money mortgage typically requires a down payment, although the amount can be negotiated directly between the buyer and the seller, potentially offering more flexibility than traditional bank requirements.

Can a purchase money mortgage be refinanced?

Yes, a purchase money mortgage can be refinanced, often to secure a lower interest rate or to pay off a balloon payment that may be due at the end of the loan term.

What happens if I default on a purchase money mortgage?

If you default on a purchase money mortgage, the lender (whether the seller or a third party) has the right to initiate foreclosure proceedings to take possession of the property and recover the outstanding debt.

Are interest rates higher on purchase money mortgages?

Interest rates on purchase money mortgages, particularly those offered through seller financing, are often higher than traditional bank rates to compensate the seller for the increased risk they are assuming.

The Strategic Role of Purchase Money Mortgages in Real Estate

A purchase money mortgage serves as a vital tool in real estate transactions, offering an alternative financing route that can facilitate sales when traditional methods fall short. By understanding its unique legal standing, particularly its priority over other liens, and carefully weighing the benefits against the potential risks, both buyers and sellers can leverage this mechanism to achieve their respective goals. Whether it’s a buyer securing a home despite credit challenges or a seller expediting a sale while earning interest, the purchase money mortgage remains a significant, albeit complex, component of property law and real estate finance.